Key Stats for TJX Companies Stock

- Current Price: $157 (May 21, 2026)

- Q1 FY2027 Revenue: $14.32B, up 9% YoY

- Q1 FY2027 Diluted EPS: $1.19, up 29% YoY

- Full-Year Revenue Guidance (FY2027): $63.2B to $63.7B, up 5% to 6%

- Full-Year EPS Guidance (FY2027): $5.08 to $5.15, up 7% to 9%

- TIKR Model Price Target: $211.09

- Implied Upside: ~34%

TJX Stock Beats Q1 Estimates Across Every Division but Fuel Hedges Funded Half the Beat

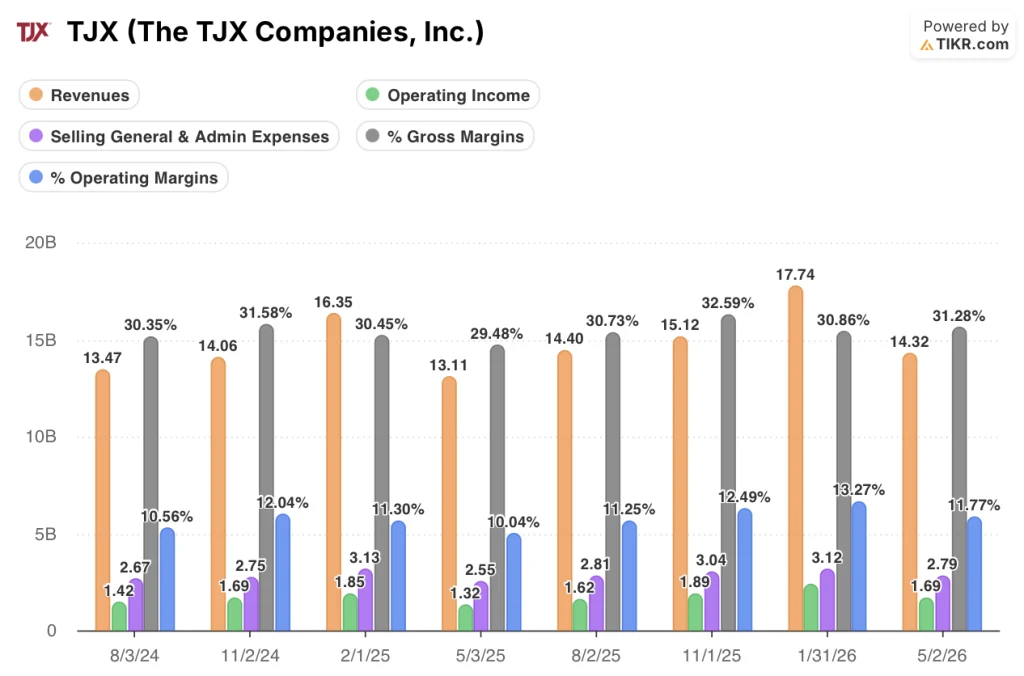

The TJX Companies (TJX) reported Q1 FY2027 revenue of $14.32B, up 9% year over year, beating Street estimates of $14.0B, following its Q1 2027 earnings release.

Diluted EPS came in at $1.19, up 29% from $0.92 in the prior-year period and $0.17 above the Street estimate of $1.02.

Pretax profit margin reached 12%, up 170 basis points, while gross margin expanded to 31.3%, up 180 basis points, driven by merchandise margin improvement, favorable inventory hedges, and fuel hedge gains.

Every division posted comp sales growth: Marmaxx grew 6% with segment profit margin up 100 basis points to 14.7%, HomeGoods surged 9% with segment profit margin up 270 basis points to 12.9%, TJX Canada grew 7%, and TJX International rose 4%.

John Klinger, CFO and Executive Vice President, stated on the Q1 FY2027 earnings call that “we beat our guidance in the first quarter by $0.20, and we’re flowing $0.13 to the year,” with the $0.07 differential reflecting fuel costs now embedded in the full-year plan at current diesel prices.

Management raised full-year comp sales guidance to 3% to 4%, full-year revenue guidance to $63.2B to $63.7B, and full-year EPS guidance to $5.08 to $5.15.

TJX returned $1.1B to shareholders through buybacks and dividends in Q1, and raised its FY2027 share repurchase guidance to $2.75B to $3.0B.

TJX Stock Revenue Up 9% and Every Margin Line Expanding, Until Fuel Costs Hit the Back Half

TJX has now posted positive revenue growth in seven consecutive quarters visible in the income statement, accelerating from 5.6% in the August 2024 quarter to 9.2% in the most recent Q1 FY2027 period ended May 2, 2026.

Gross margins bottomed at 29.5% in the May 2025 quarter, then recovered to 30.7%, 32.6%, 30.9%, and now 31.3%, a trajectory that reflects TJX’s improving merchandise margin and the structural benefit of its off-price buying model.

Operating income reached $1.69B in Q1 FY2027, up 28% from $1.32B in the year-ago quarter, supported by operating margin expanding to 11.8% from 10.0%.

The quarterly operating margin trajectory tells the fuller story: 10.6% in August 2024, 12.0% in November 2024, 11.3% in February 2025, then 10.0% before recovering through 11.2%, 12.5%, 13.3%, and back to 11.8% in the most recent quarter, showing a seasonal compression pattern with a clear upward floor.

SG&A came in at $2.79B, representing 19.5% of revenue, unfavorable by 10 basis points versus the prior year, with management attributing the modest deleverage to incremental store wage and payroll costs.

The gross margin expansion of 180 basis points in Q1 FY2027 is the largest single-quarter expansion visible across the eight quarters in the income statement, but management has already signaled that fuel hedge gains (a first-quarter tailwind) will not repeat at the same level in the back half of the year.

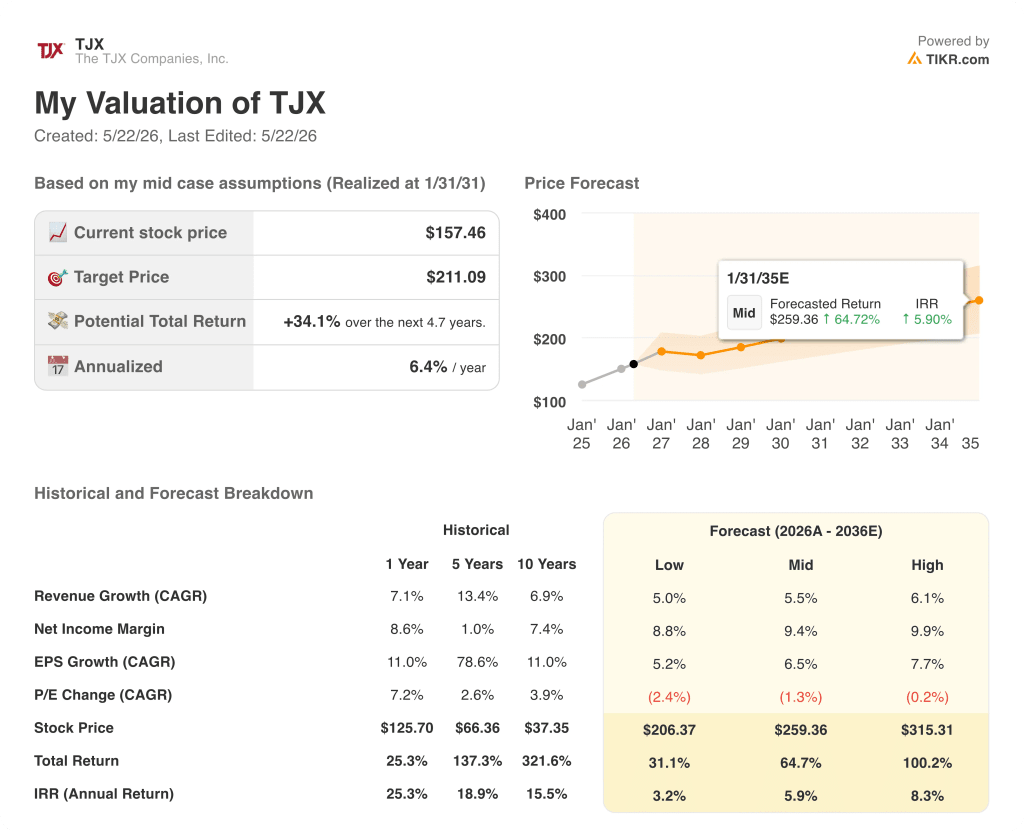

TIKR’s $211 Target on TJX Stock Requires Margin Assumptions That Fuel Costs Are Already Pressuring

TIKR’s valuation model prices TJX stock at $211 by January 2031, implying a 34% total return from the current price of $15, or 6.4% annualized over around 5 years.

The mid-case assumes revenue CAGR of 5.5% and net income margins expanding to 9.4%, figures that are directionally supported by the Q1 beat but contingent on TJX holding merchandise margin gains through a higher fuel cost environment in the back half of FY2027.

The model embeds a P/E compression assumption of negative 1.3% annually, meaning TJX stock reaches $211 despite the market assigning a slightly lower earnings multiple over time, which places the full return burden on earnings growth rather than multiple expansion.

TJX stock delivers a $206 price and 3.2% IRR in TIKR’s low case, a scenario consistent with revenue growth closer to the 5% CAGR floor and net income margins of 8.8%, which would reflect fuel costs compressing second-half profitability without a meaningful offset.

The mid case at $260 and 5.9% IRR by January 2035 assumes the 5.5% revenue CAGR and 9.4% margin hold through the forecast period, a realistic path if the HomeGoods margin recovery at 12.9% continues and Spain expansion adds incremental volume without materially diluting consolidated margins.

The high case at $315 and 8.3% IRR requires 6.1% revenue CAGR and 10% net income margins, conditions that would demand either diesel prices falling from current levels or TJX accelerating store count expansion into Spain, Mexico, and potential JV geographies management referenced on the call.

The Q1 FY2027 earnings report tightens the investment debate to a single variable: whether TJX can sustain the merchandise margin gains that drove the Q1 beat through a back half defined by elevated fuel costs management has explicitly embedded into guidance.

What happened to TJX stock after Q1 FY2027 earnings?

The TJX Companies reported Q1 FY2027 revenue of $14.32B, up 9% year over year, and diluted EPS of $1.19, up 29%, both well above Street estimates.

Every division posted positive comp sales growth, led by a 9% comp at HomeGoods. Management raised full-year EPS guidance to $5.08 to $5.15 and increased the annual share buyback program to $2.75B to $3.0B. TJX stock closed at $157 on May 21, the day after the report.

Is TJX stock undervalued right now?

TIKR’s valuation model prices TJX stock at $211 by January 2031, implying approximately 34% upside from the current price of $157.

The mid-case assumes 5.5% revenue CAGR and net income margins of 9.4%, which are achievable if merchandise margin gains persist beyond the Q1 fuel hedge tailwind.

The key variable is whether TJX sustains gross margin above 31% through the second half of FY2027, when fuel hedge benefits will not repeat at Q1 levels.

Should You Invest in The TJX Companies, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up The TJX Companies, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track The TJX Companies, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze TJX stock on TIKR for Free →