Key Stats for CRH Stock

- 52-Week Range: $87 to $132

- Current Price: $101

- Street Mean Target: $143

- Street High Target: $165

- Analyst Consensus: 16 Buys / 5 Outperforms / 2 Holds / 0 Underperforms

- TIKR Model Target (Dec. 2030): $179

CRH Beats Q1 Revenue Estimates as Infrastructure Demand and Acquisitions Compound a Strong Start to 2026

CRH plc (CRH), the world’s leading building materials and infrastructure solutions group, delivered a 9% revenue increase to $7.4 billion in Q1 2026, driven by record early-season project activity across its roads, aggregates, and water infrastructure platforms, following its April 30 earnings release.

The Americas Materials Solutions segment was the standout, posting revenue 21% ahead of the prior year, with aggregate volumes up 14% and cement volumes up 10%.

CRH stock has been building on a secular tailwind that most investors underestimate: roughly 50% of the infrastructure investment earmarked through the Infrastructure Investment and Jobs Act has yet to be deployed.

CEO Jim Mintern framed the opportunity with precision on the Q1 2026 earnings call: “2026 is expected to be a record year for investment in transportation infrastructure, which bodes well for our business given our unmatched scale and market-leading position.”

The company’s connected portfolio strategy is generating measurable results at the EBITDA line, with Q1 adjusted EBITDA reaching $586 million, up 18% year over year, alongside 70 basis points of margin expansion.

CRH has also been aggressively recycling capital, announcing $1.9 billion in divestitures of noncore businesses while committing around $900 million to nine value-accretive acquisitions in the year to date, including a $700 million agreement to acquire Axius Water, a leading U.S. water quality and nutrient removal provider.

The buyback program has returned approximately $400 million to shareholders so far in 2026, with a fresh $300 million tranche launched April 30, extending a program that has now returned $10 billion since 2018.

Wall Street Lifts CRH Targets to $143 as EBITDA Growth and Infrastructure Tailwinds Strengthen the Bull Case

The central investment debate around CRH stock is not whether the business is growing — it clearly is. The debate is whether the current multiple reflects the durability and scale of that growth, or whether the market is discounting it too heavily against macro noise.

CRH’s EBITDA picture is consistent and directional: $2.46 billion in Q2 2025, $2.70 billion in Q3 2025, then consensus estimates of $2.62 billion in Q2 2026 and $2.93 billion in Q3 2026, with Q3 margins projected to reach 25.0%.

The seasonality in EPS and EBIT requires a direct explanation for any investor reading the Q1 figures in isolation.

CRH is a construction materials business whose revenue and earnings are heavily weighted to Q2 and Q3, the active building season in the Northern Hemisphere. Q1 is structurally the weakest quarter: the reported EBIT for Q1 2026 was $(0.04) billion and EPS Normalized came in at $(0.21).

These are not signs of fundamental deterioration. They reflect a business that generates the bulk of its annual EBITDA between April and October, a pattern the full-year guidance of $5.60 to $6.05 in diluted EPS already prices in.

The Street has internalized this dynamic. With 16 Buys, 5 Outperforms, and only 2 Holds in the current coverage table, the analyst community is aligned on the bull thesis. The mean price target of around $143 implies roughly 41% upside from the current price of $101, and the street high sits at $165.

The next catalyst to watch is the Q2 2026 earnings report, expected in July, which will represent the first full quarter of peak construction season and the first material test of whether the $8.1 to $8.5 billion EBITDA guidance range holds as weather normalization arrives.

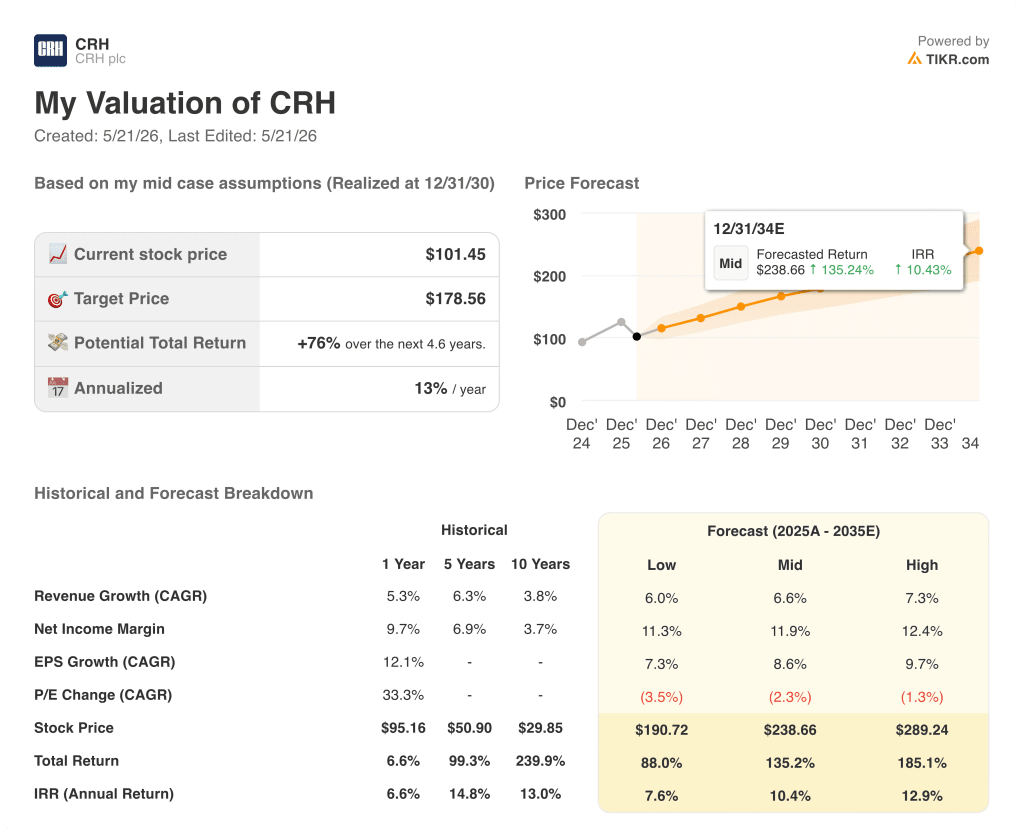

CRH’s TIKR Valuation Points to $179 as Infrastructure Compounding and Water Expansion Justify a Re-Rating

TIKR’s base case values CRH at around $179 per share by December 2030, built on mid-case assumptions of around 7% revenue CAGR and an 12% net income margin, grounded in the company’s decade-long track record of 15% compound annual EBITDA growth and its expanding water infrastructure platform.

The central tension in CRH stock is straightforward: the business is a proven compounder with a decade of data behind it, but the current price reflects macro skepticism that the construction cycle has peaked.

The bull case rests on a simple fact: roughly 50% of IIJA highway funds have yet to hit the street, the $700 million Axius Water deal opens a new growth lane in the fast-expanding water quality market, and Q1 mix-adjusted aggregate pricing already came in 5% ahead, giving management the commercial footing to defend margins through the full season.

The risk is that Congress opts for a continuing resolution instead of a new highway funding bill, energy costs spike faster than mid-year price increases can offset, and the subdued residential market keeps the Outdoor Living segment in a holding pattern longer than expected.

TIKR’s model prices the range at around $191 on the low end and around $289 on the high end by 2034, with IRRs of roughly 8% and 13% respectively, meaning even the cautious scenario still implies meaningful upside from the current price of $101.

Is CRH stock undervalued right now?

TIKR’s base case values CRH at around $179 per share by December 2030, implying roughly 76% upside from its current price of $101. With 16 analysts issuing Buy ratings and a mean Street target near $143, consensus supports the undervaluation view.

The key variable is sustained EBITDA margin expansion toward 25% through the peak construction season.

What do analysts say about CRH stock?

The current coverage table shows 16 Buys, 5 Outperforms, and 2 Holds, with a mean price target around $143 and a Street high of $165.

That implies roughly 41% upside at consensus and 63% at the high target. The near-unanimous bullish positioning reflects CRH’s IIJA tailwind, its 18% Q1 EBITDA growth, and the company’s track record of 15% compound annual EBITDA growth over the past decade.

Should You Invest in CRH plc?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up CRH plc stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track CRH plc alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze CRH stock on TIKR for Free →