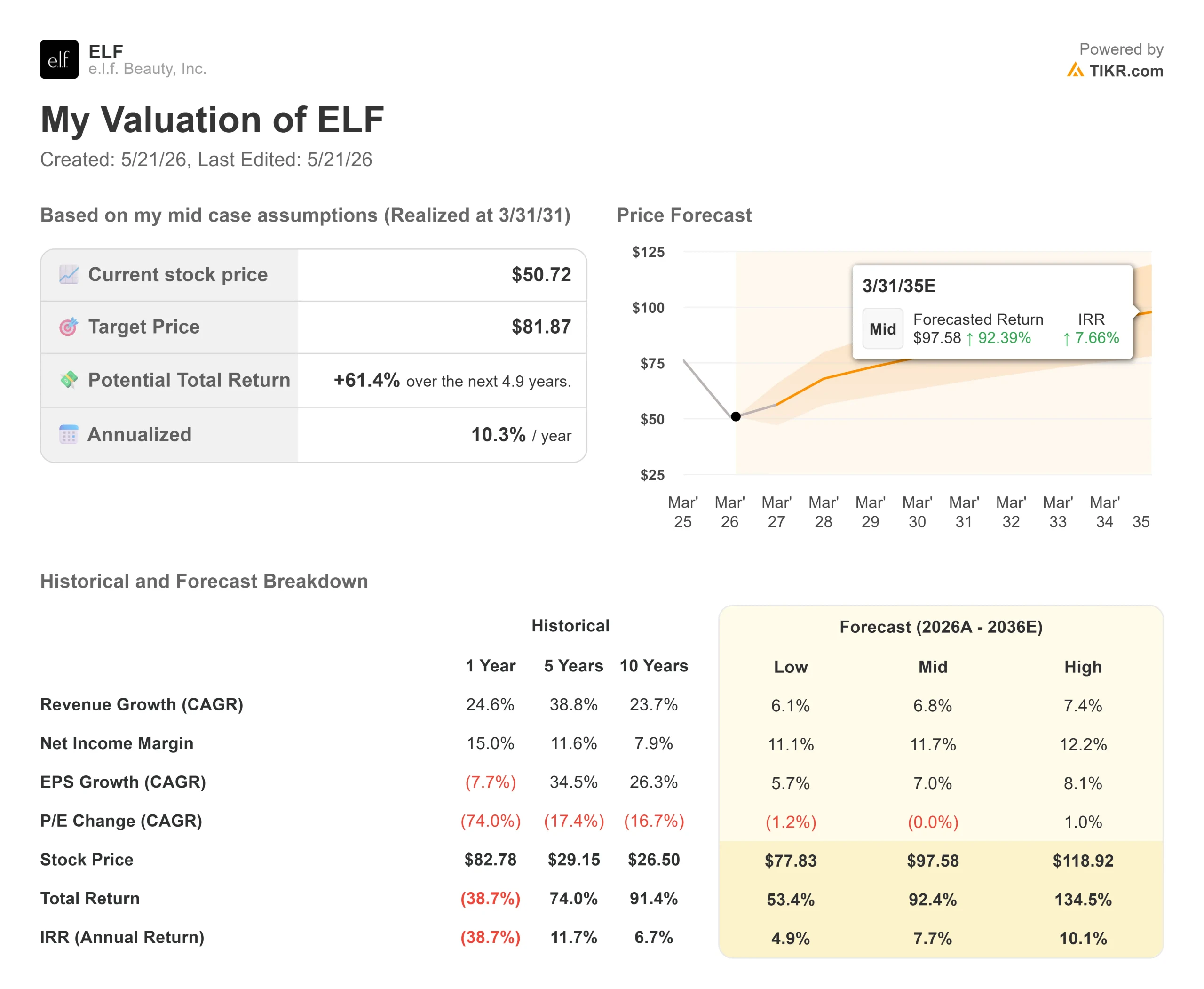

Key Stats for e.l.f. Beauty Stock

- Current Price: $50.72

- Target Price (Mid): ~$82

- Street Target: ~$88

- Potential Total Return: ~61%

- Annualized IRR: ~10% / year

- Q4 Earnings Reaction: +7.39% after-hours, May 20, 2026

- Max Drawdown: -65.42% (5/20/26)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

e.l.f. Beauty (ELF) just delivered its 29th consecutive quarter of net sales growth, beating Q4 estimates on both the top and bottom lines. The stock rose roughly 7% in after-hours trading on Wednesday. The most important number in the release, though, was not the revenue beat. It was the fiscal 2027 EPS midpoint of $3.30, against a Street consensus of $3.61. That gap is what investors are working through.

ELF has shed 65.42% from its 52-week high of $150.99, closing at $50.72 on May 20, near its 52-week low of $50.13. Wednesday’s results confirmed the story has split into two. Rhode, the prestige skincare brand founded by Hailey Bieber and acquired by e.l.f. in August 2025, is growing at a pace most beauty companies would envy. The core e.l.f. cosmetics brand is not keeping up.

That divergence is the central question for anyone considering ELF at current prices. The TIKR valuation model puts the mid-case target at ~$82 by March 2031, implying about 61% upside. Getting there requires one thing: management reviving the core brand’s unit velocity while Rhode expands globally.

What Q4 Actually Showed

Q4 net sales grew 35% year-over-year to $449.29 million, beating the Street estimate of $423.03 million. Adjusted EPS came in at $0.32, ahead of the $0.29 consensus. Gross margin expanded approximately 140 basis points to 73%, driven by the August 2025 price increase, even as average tariff rates of around 55% weighed on results throughout the year.

Rhode was the engine. CFO Mandy Fields confirmed the acquisition contributed $113 million, or approximately 34 percentage points, to Q4 net sales growth. On a pro forma basis for all of fiscal 2026, Rhode delivered approximately $390 million in net sales, growing over 80% year-over-year. It reached the number one beauty brand ranking at Sephora North America while still sitting in less than 20% of Sephora’s global store count.

The GAAP results were noisier. e.l.f. posted a net loss of $49.4 million in Q4, driven largely by a $57.6 million fair-value adjustment on the Rhode acquisition earnout, reflecting that Rhode outperformed the thresholds set in the merger agreement. Adjusted net income was $19.4 million, or $0.32 per diluted share.

Organic net sales, excluding Rhode, grew approximately 1% year-over-year in Q4, within the guidance range management provided in February. That is the e.l.f. brand’s current reality: steady, but far from what built the stock’s premium.

See historical and forward estimates for e.l.f. Beauty stock (It’s free!) >>>

The Core Brand Problem and What Management Is Doing About It

CEO Tarang Amin was direct on the call. e.l.f. brand global consumption “moderated from high single digits in fiscal ’26 to low single digits in the last 12 weeks.” Spring 2026 innovation launched slower than expected, and without the innovation halo, core item velocity softened. Unit volume was down approximately 5 points in Q4.

The root cause is the $1 price increase e.l.f. took across all SKUs in August 2025, in response to tariffs and inflation. It worked for dollar sales but hurt units. Amin told CNBC that consumers have been “suffering with higher costs” and that the company is already testing reversals.

The Halo Glow skin tint was cut from $18 to $14, producing a 38% unit lift on Amazon and a 36% lift across all retailers, including a triple-digit sales lift on TikTok Shop. More pricing actions are coming in the next few weeks. None of this is in the fiscal 2027 guidance yet. Neither is the $58.5 million in IEEPA tariff refunds (tariffs paid under a now-challenged executive order) the company is pursuing. Fields confirmed that any refunds would flow through the P&L, with management planning to reinvest them into value and unit growth.

Fall 2026 innovation ships within the month, and additional unplanned innovation is being fast-tracked for the holiday period. Three leadership appointments sharpen the brand focus: Kory Marchisotto as President of e.l.f. Brands, Oshiya Savur as Chief Marketing Officer for e.l.f. Brands, and Ekta Chopra in a newly created Chief Technology and AI Officer role.

The FY27 guidance is built on e.l.f. consumption staying near the low-single-digit rates seen in the last 12 weeks, with no credit for price reductions, incremental innovation, or tariff refunds. That is a conservative baseline.

Rhode and the International Opportunity

Rhode delivered over $500 million in global retail sales in fiscal 2026 on an annualized basis. It is Sephora North America’s top brand while occupying roughly one bay of shelf space where competitors hold two or three. The primary operational constraint, per Amin, has been keeping stores replenished, not generating demand.

This September, Rhode expands into Sephora Europe across 19 countries. Earlier in fiscal 2026, Rhode’s MECCA launch in Australia and New Zealand set the record for MECCA’s biggest launch in history. Even modest success in Europe would shift the organic revenue trajectory in the second half of fiscal 2027.

The broader portfolio is more diversified than a year ago. Non-e.l.f. brand sales have grown from 0% to about 30% of global consumption over three years. Skincare has risen from 9% to 23% of global consumption. Manufacturing outside China has expanded from 1% to over 45%, directly reducing tariff exposure. International net sales represent only about 20% of e.l.f.’s total today, compared to over 70% for legacy beauty peers.

Naturium delivered nearly $250 million in global retail sales in fiscal 2026, double its pre-acquisition levels, and was the fastest-growing brand among the top 50 skincare brands in Q4. e.l.f. SKIN reached approximately $200 million in global retail sales and has climbed from the 25th to the 11th-ranked mass skincare brand over five years.

See how e.l.f. Beauty performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $50.72

- Target Price (Mid): ~$82

- Potential Total Return: ~61%

- Annualized IRR: ~10% / year

See analysts’ growth forecasts and price targets for e.l.f. Beauty stock (It’s free!) >>>

The TIKR mid-case model values ELF at approximately $82 per share by March 2031, using a revenue compound annual growth rate (CAGR) of approximately 7% and a net income margin of approximately 12%.

The two revenue CAGR drivers are Rhode’s global retail expansion, the September Sephora Europe launch across 19 countries, and continued North America shelf space gains and Naturium’s accelerating brand investment, which has already proven out at Boots U.K. and in Walmart. The margin driver is SG&A leverage, with management guiding fiscal 2027 adjusted EBITDA margins of approximately 21%, up about 20 basis points year-over-year.

The upside case reaches approximately $119 per share, requiring faster Rhode international adoption, a unit recovery on the core brand from the pricing actions, and the $58.5 million tariff refund flowing through the P&L. The downside case sits near $78, reflecting continued e.l.f. brand softness and the $15 to $20 million in potential oil-related cost headwinds management flagged for fiscal 2027.

At a current NTM EV/EBITDA of 10.63x, ELF trades near multi-year low valuation multiples, down from 21.78x as recently as September 2025. The Street carries a mean target of $88.33, with 10 Buys, 1 Outperform, 6 Holds, and 1 No Opinion, implying approximately 74% upside to the Street mean from current levels.

Conclusion

The thesis comes down to one number in August: Q2 fiscal 2027 organic net sales.

Q1 will look ugly by design, management guided organic net sales down high single digits, lapping last year’s pre-SAP shipping surge. What matters is Q2, where management guided organic growth in the “mid-teens range” as Rhode enters the organic base and the comparison normalizes. If the pricing actions and fast-tracked innovation also show unit recovery by then, the FY27 EPS guide of $3.27 to $3.32 becomes a floor, not a ceiling.

Watch for Q2 organic net sales at or above mid-teens, with unit trends improving sequentially, in the August earnings release. At $50.72, ELF is pricing in very little credit for Rhode’s European expansion, the tariff refund, or any unit recovery on the core brand.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in e.l.f. Beauty?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up e.l.f. Beauty, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track e.l.f. Beauty alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze e.l.f. Beauty on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!