Key Stats for Dell Stock

- 52-Week Range: ~$112 to ~$285

- Current Price: $242.93

- Street Mean Target: ~$255

- TIKR Target Price (Mid): ~$278

- TIKR Annualized IRR (Mid): ~3% per year

- FY2026 Revenue: $113.5B (up 19% YoY)

- FY2026 Non-GAAP EPS: $10.30 (up 27% YoY)

- FY2026 AI Server Orders: $64.1B

- AI Backlog Entering FY2027: $43B

- FY2027 Revenue Guidance: ~$140B

Value your favorite stocks like DELL with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

Why Dell’s Best Year Ever Is Also Its Most Complicated

Dell (DELL) spent most of its history being defined by PCs and commoditized hardware. The last two years changed that framing entirely. Dell closed more than $64 billion in AI-optimized server orders in fiscal 2026, shipped more than $25 billion throughout the year, and entered fiscal 2027 with a record backlog of $43 billion. CEO Jeff Clarke called it a defining year. By the revenue numbers alone, it was.

Full-year revenue reached $113.5 billion, up 19%, with non-GAAP EPS of $10.30, up 27%, and more than $11 billion in annual cash flow. Dell returned $7.5 billion to shareholders, raised its annual dividend 20%, and approved a $10 billion increase in its buyback authorization.

All of that is genuinely strong. The complication is what it means for the business’s long-term margin structure, and the gross profit chart is where that story lives.

See historical and forward estimates for DELL stock (It’s free!) >>>

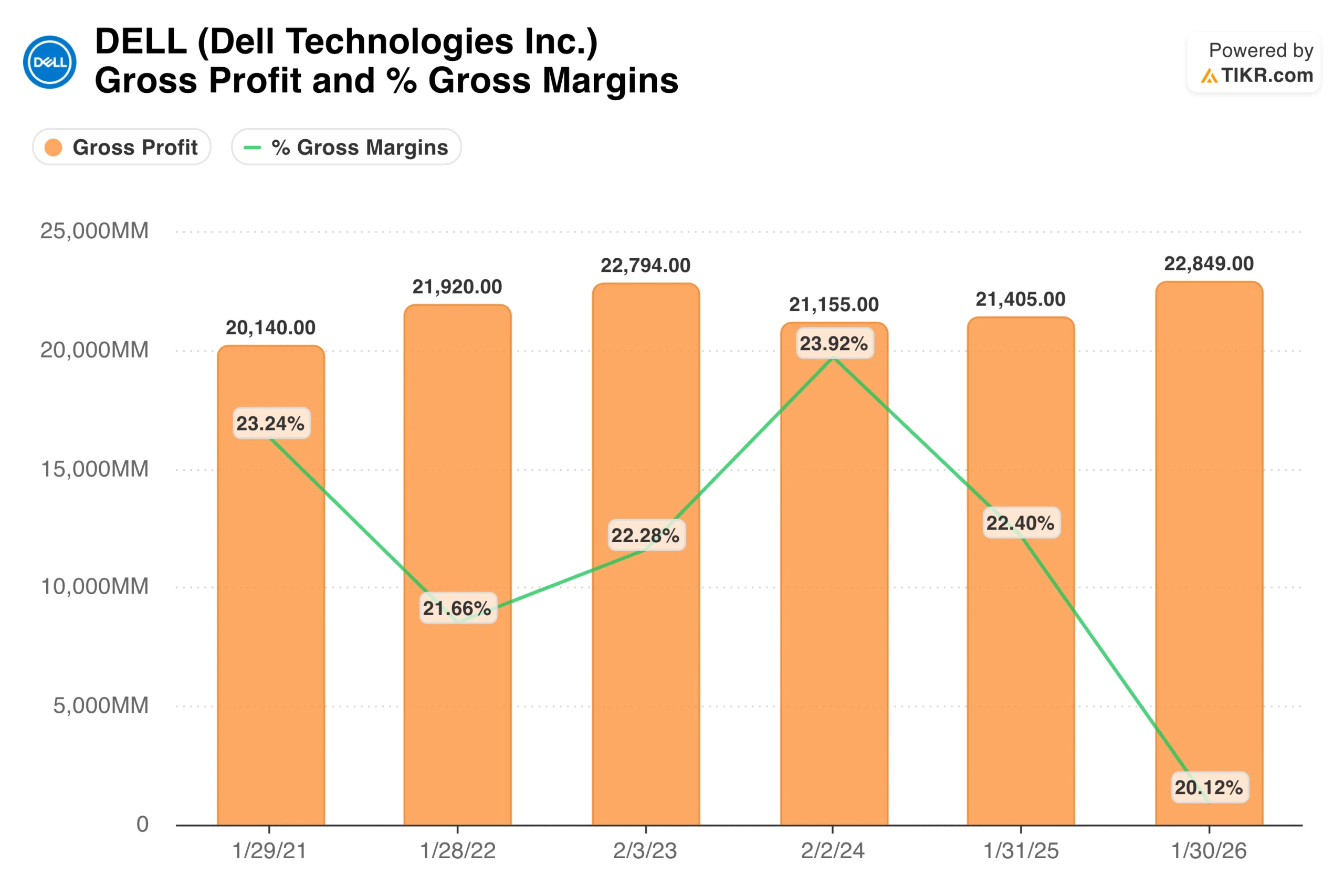

What the Gross Margin Chart Is Actually Saying

Gross profit dollars have been relatively stable over the past five years, ranging from $20.1 billion to $22.8 billion. The FY2026 number at $22.85 billion is a record on an absolute basis. But gross margin percentage dropped to 20.1% in FY2026, the lowest in this series.

That decline tells you something specific: AI servers are enormous revenue but thin-margin hardware. Q4 gross margin rate was 20.5%, reflecting the mix shift toward AI servers. The more AI server revenue Dell generates, the more total revenue grows, and the more gross profit dollars come in, but also the more the margin percentage compresses.

This is not a flaw in the business, it is a structural characteristic of selling high-volume, low-margin hardware to hyperscalers.

The bull case says services, software, and storage attach to those server sales over time, which are higher-margin revenue streams that gradually improve the mix. The bear case says AI servers remain the dominant revenue driver and margins stay structurally compressed.

Management guided that AI server profitability is tracking toward a mid-single-digit operating margin, which is the number to watch as the backlog converts.

What the Net Income Recovery Looks Like

Net income tells a cleaner story. It fell to $2.44 billion in FY2023 after the VMware spin-off removed that contribution from Dell’s results, then recovered to $3.39 billion in FY2024, $4.59 billion in FY2025, and a record $5.94 billion in FY2026. The trajectory is consistently upward, and the most recent year was the strongest in the company’s post-spin history.

The gap between gross profit and net income is where Dell’s operating discipline shows up. Even as gross margins compressed, operating leverage through scale and cost control allowed net income to grow substantially.

Operating expenses fell as a percentage of revenue to 9.9% in Q4, and operating income grew 32% to $3.5 billion. That combination of disciplined spending and surging top-line demand is what turns low gross margins into record net income.

See what analysts think about DELL stock right now (Free with TIKR) >>>

What the TIKR Model Implies at the Current Price

The mid-case target is around $278 over about 4.7 years, implying roughly 14% total return at around 3% annually. The model uses revenue growth of around 6% per year, net income margins of around 6%, and EPS growth of around 7%. The low case, at around $236, is actually below the current stock price. The high case reaches around $360 at roughly 5% annually.

This is worth being direct about. Dell had one of the best years in its history, growing revenue by 19% and EPS by 27%, and entering FY2027 with unprecedented AI server demand. The TIKR model is saying the stock has priced in most of it.

The 3-year return of 411% that preceded this moment is exactly what a stock looks like when the market correctly anticipated a transformation and rewarded it in advance.

What Could Drive the Returns Higher or Lower

The bull case requires two things to happen. First, the $43 billion AI backlog converts to revenue without significant order cancellations or margin deterioration. Management guided FY2027 revenue to around $140 billion, with AI-optimized server revenue projected to roughly double to around $50 billion.

Second, the services and storage attach rates improve over time, gradually lifting the blended margin above the current 20% level. If both happen, the high case at around $360 becomes the relevant scenario.

The risks are also specific. Hewlett Packard Enterprise warned that memory shortages will persist through 2027, a critical component for Dell’s high-density AI server configurations. Supply constraints could slow backlog conversion.

Gross margins could remain compressed if the mix shift toward AI servers deepens rather than balances out. And at around 24 times trailing earnings, the stock does not offer much cushion for execution misses

Is DELL Worth Buying at $243?

Dell is a genuinely transformed business. The AI server backlog, record cash generation, buybacks, and the dividend increase all reflect a company executing extremely well amid one of the most powerful secular spending cycles in enterprise technology.

The honest read from the TIKR model is that the stock is close to fair value at the current price. A mid-case return of around 3% annually is not a reason to sell a quality business, but it is a reason to be clear-eyed about what you are buying.

For investors who already own Dell, the model says hold. For investors deciding whether to initiate at $243, the upside requires the high case to materialize, and the low case is essentially flat.

See analysts’ growth forecasts and price targets for DELL stock (It’s free!) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!