Key Stats for Booking Holdings Stock

- Current Price: $159.68

- Target Price (Mid): ~$322

- Street Target: ~$224

- Potential Total Return: ~102%

- Annualized IRR: ~16% / year

- Earnings Reaction: +0.35% (4/28/26)

- Max Drawdown: -33.75% (5/15/26)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Booking Holdings (BKNG) has had a punishing 2026. The stock hit a max drawdown of -33.75% on May 15, falling from a 52-week high of $233.58 to as low as $150.14, as the Middle East conflict forced management to cut full-year guidance. The market is treating that guidance cut as evidence of structural damage.

CEO Glenn Fogel, speaking at the J.P. Morgan 54th Annual Global Technology, Media and Communications Conference on May 20, made a forceful case that the market has the diagnosis wrong.

The Guidance Cut That Spooked Investors

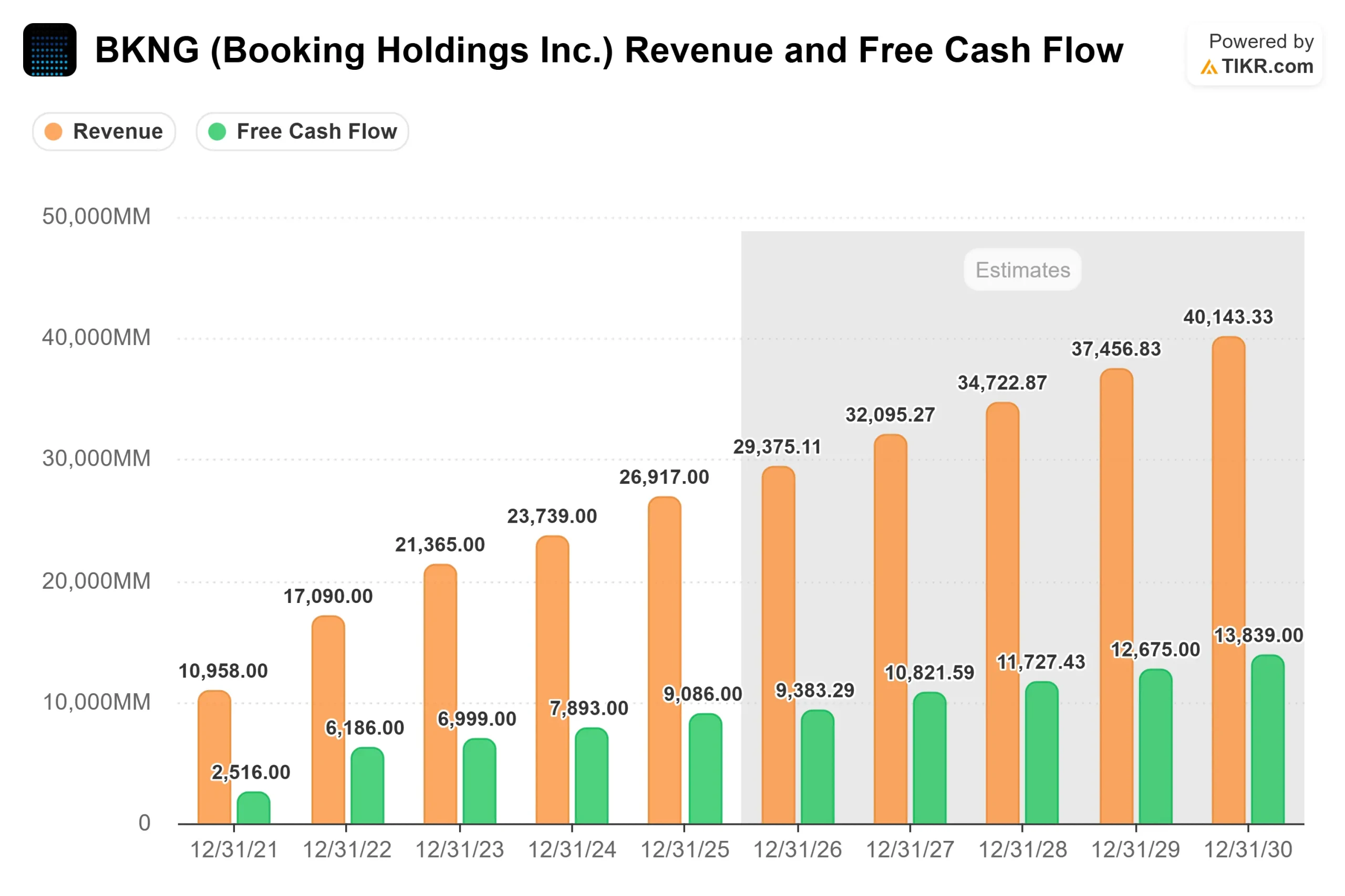

On April 28, Booking reported Q1 2026 revenue of $5.53 billion, up 16% year over year, and beat on every key metric. Adjusted EPS came in at $1.14 versus the $1.08 consensus, and adjusted EBITDA of $1.29 billion beat estimates by 3.47%, per TIKR’s Beats & Misses data. Then the guidance landed.

Management cut full-year revenue growth guidance from low double digits to high single digits, with Q2 room night growth guided to just 2% to 4%. The stock’s 1-day reaction on April 28 was a muted +0.35%, but selling continued. On May 11, shares fell another 5.57% after the company revised its outlook further and issued €1.9 billion in new senior notes. JPMorgan cut its price target to $208 from $224 while keeping an Overweight rating.

The conflict’s actual impact on the underlying business, though, is more contained than the stock move implies. CFO Ewout Steenbergen disclosed on the Q1 call that the Middle East situation reduced room night growth by approximately 2 percentage points. Without it, room nights would have grown approximately 8%, above the high end of guidance. The business itself is not breaking down.

See historical and forward estimates for Booking Holdings stock (It’s free!) >>>

Three Things Fogel Said That Investors Need to Hear

Fogel did not come to JPMorgan to manage guidance expectations. He came to build the long-term case, and three parts of that conversation stand out.

Travel’s structural tailwind is intact. Fogel pointed to roughly 4 billion people globally who still cannot afford to travel, calling them a multi-decade demand driver. He also noted that approximately one-third of global travel bookings are still made outside digital channels, meaning the secular shift to online is far from complete. “Long term, travel has always in the past, and I absolutely believe always in the future, will be a growth industry,” he said. “It has exceeded global GDP by 1% to 2% for a very, very long time.”

AI is a competitive advantage, not a threat. One of the biggest fears driving BKNG’s 2026 selloff was that AI tools like ChatGPT would disintermediate OTAs (online travel agencies) by letting travelers book directly through large language models. Fogel’s position is the opposite. Booking’s data advantage, 1.3 billion room nights booked over the last 12 months, creates AI and machine learning models that improve with scale. “Because we are the biggest, because we have the most data, what is the most important thing in AI is having data that you can then train models off of. It’s a flywheel that just keeps on spinning faster,” he said. He also confirmed that 65% of Booking.com visitors now arrive directly, a figure he wants to grow further. Personalization through the Genius loyalty program creates pricing advantages no third-party platform can replicate, because the underlying data stays proprietary.

Investment continues through the downturn. Fogel explicitly said he would not pull back on product investment because of short-term volatility. He pointed to 2020, when Booking still generated close to $900 million in EBITDA during travel’s worst year on record, in his own characterization, because performance marketing spend scales with demand automatically. That structural flexibility means the company can maintain investment in AI and Connected Trip regardless of what Q2 looks like.

Connected Trip: The Growth Story Still Being Written

Connected Trip is Booking’s push to evolve from an accommodation platform into a full travel ecosystem spanning flights, cars, restaurants, and in-destination activities. Connected transactions grew at a high-teens rate in Q1 and now represent a low double-digit percentage of Booking.com’s total transactions, per Fogel’s JPMorgan remarks. Flight ticket volumes grew 28% year over year last quarter, and Fogel said that, excluding Ctrip.com’s domestic Chinese volumes, Booking may now rank as the largest third-party flight seller globally.

The white space ahead is substantial. Fogel described the OpenTable integration as barely started: Booking knows a guest is staying at a hotel in Mayfair, OpenTable knows their dining preferences, yet no personalized restaurant recommendation flows between the two today. When that connection is built, it creates monetization across verticals that do not yet exist in the numbers. “We are so far from where we’re going to be,” he said.

Is BKNG Undervalued at $159?

The analyst community has not abandoned the stock. TIKR’s Street Targets data shows 24 Buys, 6 Outperforms, and 7 Holds among the 37 analysts covering BKNG, with zero Underperforms or Sells. The consensus price target is $224.41, implying about 40% upside from today. The most bullish target on the Street is $298.

On valuation, the picture is similarly compelling when you look past the guidance cut. BKNG trades at 11.38xNTM EV/EBITDA below Airbnb’s 13.95x and below the peer group mean of 13.53x on TIKR’s Competitors page, despite carrying 87% gross margins and significantly wider geographic diversification. On a free cash flow basis, BKNG’s NTM MC/FCF of 11.72x sits well below the peer mean of 19.76x, per TIKR data, meaning investors are getting a substantial cash flow yield while waiting for conditions to normalize.

The bear case is real. Q2 guidance of 2% to 4% room night growth is a sharp deceleration, and the full-year recovery Booking is modeling depends on conflict resolution management, which itself cannot be guaranteed. European regulatory pressure adds further uncertainty: Italy’s AGCM launched a formal investigation into Booking.com’s Preferred Partner program in April 2026, examining whether hotel commission levels influence search rankings. Booking is cooperating.

What makes BKNG different from a typical guidance-cut story is the quality underneath the noise: an LTM ROIC of 93.6%, 87% gross margins, and a share count reduced by over 40% since 2014. Earnings surprise data on TIKR shows Booking has beaten adjusted EPS estimates in four of the last five reported quarters.

See how Booking Holdings performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $159.68

- Target Price (Mid): ~$322

- Potential Total Return: ~102%

- Annualized IRR: ~16% / year

See analysts’ growth forecasts and price targets for Booking Holdings stock (It’s free!) >>>

The TIKR mid-case model, with a forecast endpoint of December 31, 2030, projects approximately $322 per share, around 102% total return from today, and an annualized IRR of approximately 16% per year.

Two revenue CAGR drivers underpin the model: geographic expansion in underpenetrated markets, particularly the U.S. and Asia, and Connected Trip adoption across flights, cars, and in-destination services. The mid case assumes around 8% revenue CAGR through 2030 and net income margins expanding toward approximately 31% from today’s 26.9%, as rising direct traffic reduces performance marketing spend per booking.

The high case reaches approximately $681 by 2030 under around 9% revenue growth and approximately 32% net income margins, implying roughly 327% total return. The low case, at around 7% revenue growth and approximately 29% margins, still projects approximately $400. The model uses a declining P/E CAGR of approximately -4%, meaning returns are driven by earnings growth rather than multiple expansion, a conservative assumption.

The primary risk is a Middle East conflict extending through H2 2026, which would force another guidance revision. Secondary risk is European regulatory action that limits Booking.com’s ability to run closed-user-group pricing through Genius and preferred partner programs.

Conclusion

The next inflection point is Q2 2026 earnings, expected in late July. Room night growth at or above the 4% top end of guidance, with any signal from management that H2 cancellations are stabilizing, would directly undercut the bear case. Growth at or below the 2% floor, or a further guidance revision, will likely push the stock toward its 52-week low of $150.14.

A business with 87% gross margins, an LTM ROIC of 93.6%, and 30 Buy and Outperform ratings does not stay at 11x forward EBITDA indefinitely. Late July will tell investors whether the recovery is on schedule.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Booking Holdings?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Booking Holdings, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Booking Holdings alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Booking Holdings on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!