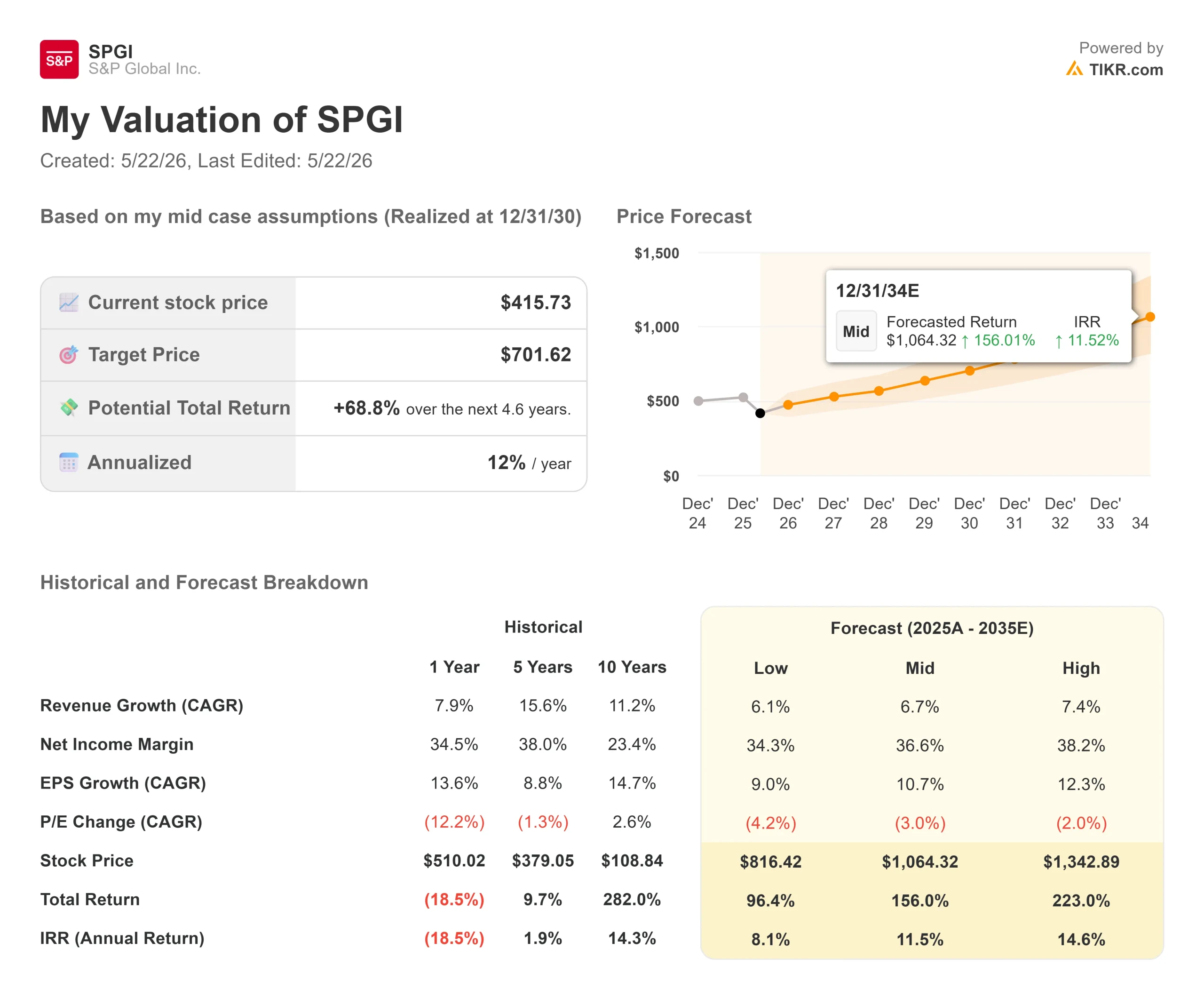

Key Stats for S&P Global Stock

- Current Price: $415.73

- Street Target: $533.76

- Target Price (Mid): ~$702

- Potential Total Return: ~69%

- Annualized IRR: ~12% / year

- Earnings Reaction: (0.06%) on April 28, 2026

- Max Drawdown: 30.73% on February 11, 2026

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

S&P Global Inc. (SPGI) has spent most of 2026 in the penalty box. A guidance miss in February sent the stock to a max drawdown of 30.73% from its 52-week high of $579.05, and every piece of good news since then has largely been sold. The stock sits at $415.73 today while 18 analysts rate it Buy, 5 rate it Outperform, and just 1 rates it Hold, with a mean Street target of $533.76.

On May 20, CEO Martina Cheung addressed shareholders at S&P Global’s Annual Meeting and made the bull case directly. The market has been unable to settle one question since February: is SPGI’s competitive position actually eroding, or did the guidance miss trigger a repricing that overshoots the fundamentals? The Annual Meeting transcript and this week’s Mobility debt pricing make that question a lot easier to answer.

What Cheung Said at the Annual Meeting

Cheung reported that 2025 revenue grew 8% year over year, adjusted operating margin expanded 140 basis points, and adjusted diluted EPS grew 14%. The company returned 113% of adjusted free cash flow to shareholders through dividends and buybacks.

The more consequential part of her remarks was on growth strategy. Cheung named three medium-term priorities: advancing market leadership, expanding into high-growth adjacencies, and amplifying enterprise capabilities through AI. On private markets specifically, she said: “We completed the acquisition of With Intelligence, expanding our private markets data and workflow capabilities,” and pointed to enhancements to the iLEVEL platform (S&P Global’s private markets data management tool), new private equity benchmarks, and partnerships with Cambridge Associates and Mercer for private credit ratings. These are concrete product steps in an asset class that generates durable demand for exactly what SPGI sells: proprietary benchmarks, credit ratings, and workflow tools.

See historical and forward estimates for S&P Global stock (It’s free!) >>>

The AI Argument Bears Are Overstating

The bear case rests on AI disruption, specifically that large language models erode demand for Market Intelligence products, particularly Capital IQ Pro (S&P Global’s flagship data and analytics platform for investment professionals). The risk is real.

But Cheung addressed it head-on at the Annual Meeting. She described 2025 as “the first full year for our Enterprise Data Organization,” built to deliver “AI-ready data” to customers so they can deploy AI workflows on SPGI’s proprietary data infrastructure rather than routing around it with public models. She also said the Chief Client Office elevated engagement to include customers’ “heads of technology, AI and data science,” enabling co-development through Kensho Labs (S&P Global’s AI and machine learning research unit).

That is not a company surprised by AI. The financial profile it is defending is formidable: a 70.5% LTM gross margin and a ratings franchise that a language model cannot replicate.

The Spin-Off Is Almost Done

The most concrete development this week isn’t the Annual Meeting. It’s the debt pricing.

On May 19, Mobility Global Inc. priced a $2 billion private offering of senior notes ahead of the planned separation: $650 million at 5.050% due 2029, $650 million at 5.450% due 2031, and $700 million at 6.050% due 2036. The offering closes May 29. Mobility Global also secured a $500 million revolving credit facility. A company doesn’t price $2 billion in debt unless the separation is close.

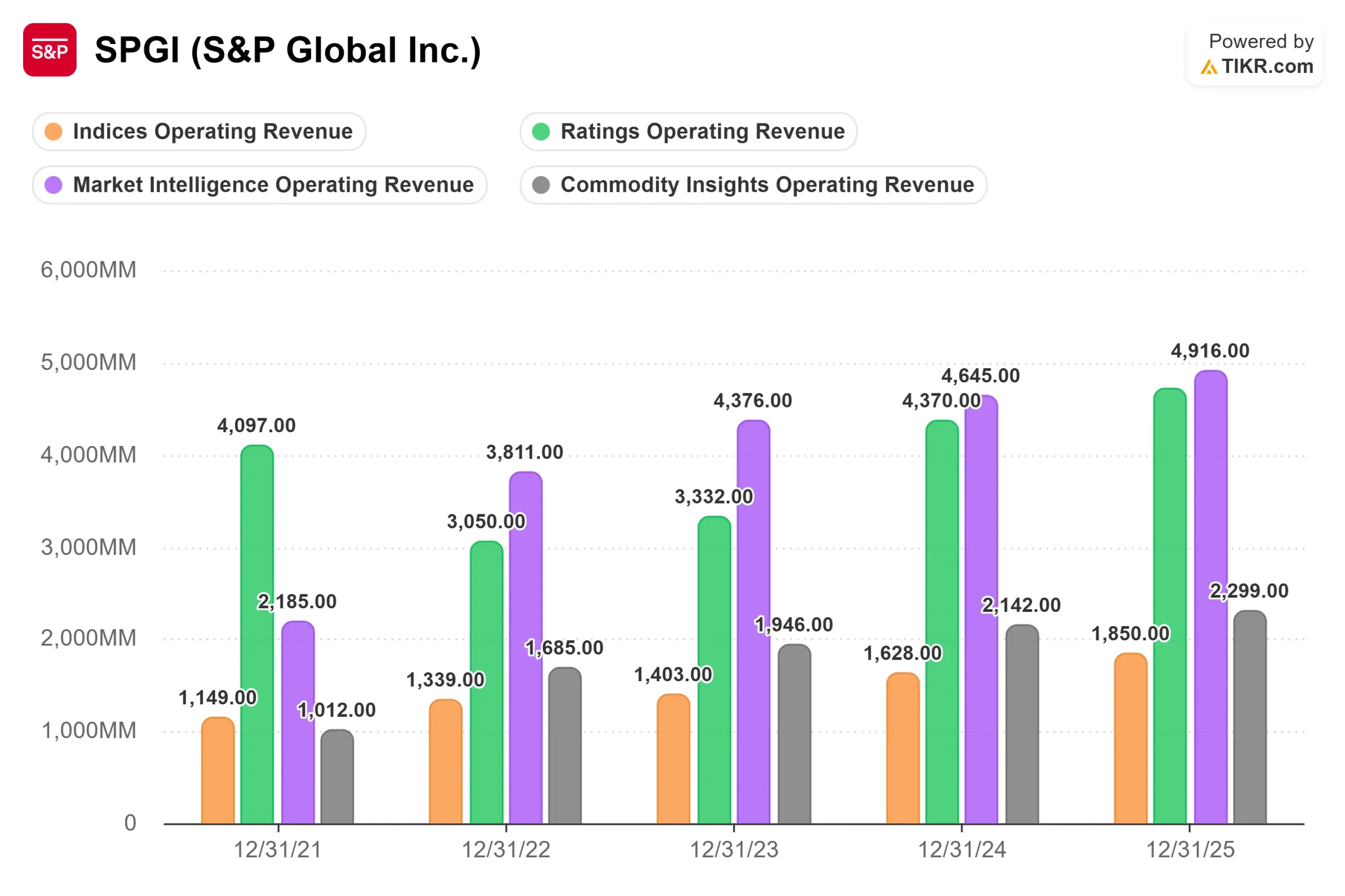

For SPGI shareholders, the spin delivers two things. First, it leaves a leaner four-segment core business: Ratings ($4.72 billion in 2025 revenue, around 64% operating margin), Indices ($1.85 billion), Market Intelligence (around $4.9 billion), and Commodity Insights (around $2.3 billion). Second, SPGI shareholders receive one Mobility Global share for every SPGI share held, tax-free.

Is S&P Global Undervalued Today?

SPGI trades at 16.15x NTM EV/EBITDA, well below the above-23x range it held in mid-2025. For context, Moody’s Corporation (MCO) trades at 19.02x with a mean analyst target of $536, and CME Group (CME) trades at 21.44x. SPGI’s discount implies the market is pricing in permanent impairment. The fundamentals don’t support that.

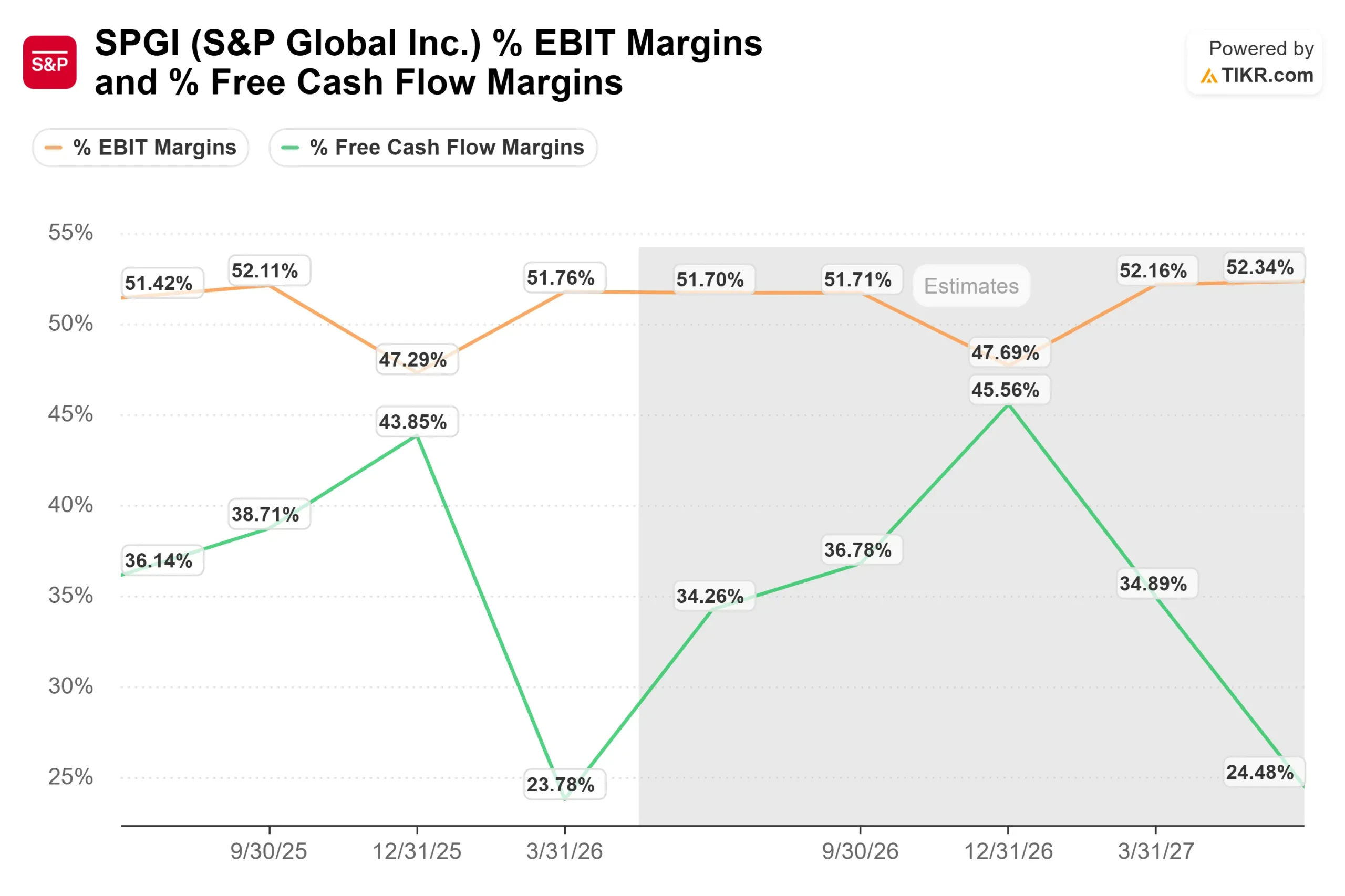

TIKR consensus estimates show revenue growing to around $16.5 billion in 2026, with EBITDA margins in the 51-52% range and normalized EPS reaching around $20 in 2026 and around $22 in 2027. That’s a compound annual growth rate of around 11% over two years, from a company that just delivered 14% adjusted EPS growth in 2025.

Two risks are worth acknowledging. The February guidance miss was real and told investors something about near-term execution. And AI disruption to Market Intelligence remains an overhang until SPGI demonstrates in revenue terms that its strategy is converting to growth, not just defending against churn.

See how S&P Global performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $415.73

- Target Price (Mid): ~$702

- Potential Total Return: ~69%

- Annualized IRR: ~12% / year

See analysts’ growth forecasts and price targets for S&P Global stock (It’s free!) >>>

The TIKR mid-case model uses a revenue CAGR of around 7% through 12/31/30. The two growth drivers are Market Intelligence subscription expansion and Indices fee growth as passive AUM (assets under management, the capital tracking benchmarks like the S&P 500) continues to grow. The margin driver is operating leverage, with net income margin expanding from the model’s 34.5% baseline to around 37% by 2030 as higher-margin segments scale.

That puts the mid-case target at approximately $702, a roughly 69% total return and an annualized IRR of around 12%. The primary downside risk is a sustained drop in debt issuance activity, which would directly compress Ratings revenue, the highest-margin segment in the portfolio.

Conclusion

The thesis resolves on two events. First, the Mobility spin-off closing is now imminent with the May 29 debt close. A clean separation removes the overhang and forces the market to re-rate the retained portfolio. Second, Q2 2026 earnings are expected in late July. If adjusted EPS holds above the Q1 level and Ratings revenue stays firm, the February guidance miss starts to look like a one-time reset, not a structural warning. If ratings disappoint, the bear case gets renewed. Either way, the data settles the argument within 90 days.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in S&P Global?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up S&P Global, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track S&P Global alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze S&P Global on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!