Key Stats for Keurig Dr Pepper Stock

- 52-Week Range: $25 to $36

- Current Price: $29

- Street Mean Target: $33

- Street High Target: $42

- Analyst Consensus: 6 Buys / 4 Outperforms / 7 Holds

- TIKR Model Target (Dec. 2030): $40

KDP Stock Beats Q1 Estimates as Beverages Run Hot and the Real Story Sits in the Split

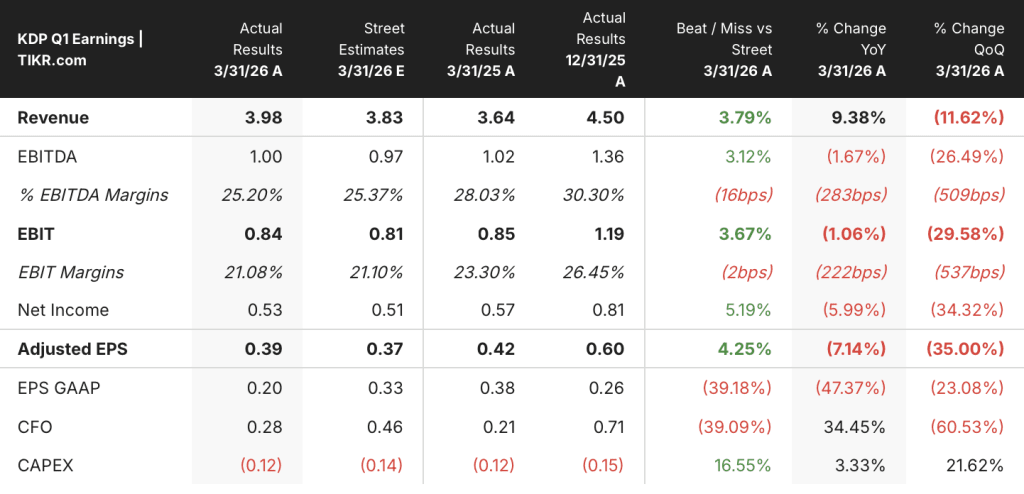

Keurig Dr Pepper (KDP) beat Wall Street estimates on both revenue and earnings in Q1 2026, posting net sales of $3.98 billion against a consensus of $3.84 billion, and adjusted EPS of $0.39 against an estimate of $0.37.

The company is not one business right now. It is two businesses in a transition period.

U.S. Refreshment Beverages, the segment carrying Dr Pepper, Snapple, Ghost, and Electrolit, grew net sales 11.9% in the quarter, with operating income rising 9.8%.

The U.S. Coffee segment declined 2.3% on a net sales basis, pressured by trade inventory adjustments that pulled pod shipments down 7% below actual point-of-sale trends, combined with peak green coffee cost inflation flowing through an 18-month hedging cycle.

CFO Anthony DiSilvestro put the two-speed dynamic plainly on the Q1 2026 earnings call: “We expect Q1 to represent the most significant year-over-year gross margin decline for our legacy KDP business, with trends improving as inflation and tariff impacts ease, particularly in the back half.”

The JDE Peet’s acquisition closed on April 1, 2026, completing a roughly $18 billion deal that brings the Dutch coffee giant into KDP’s fold alongside the planned spin into two pure-play public companies: Beverage Co. and Global Coffee Co.

Keurig Dr Pepper’s stock has shed around 24% of its value since announcing the deal in August 2025.

CEO Tim Cofer confirmed that the company still targets operational readiness to separate by end of 2026, with the official split likely occurring in early 2027, subject to market conditions.

The company reaffirmed full-year 2026 guidance for net sales of $25.9 to $26.4 billion, with constant currency adjusted EPS growth in the low double-digit range.

Is KDP Stock Undervalued? What Wall Street Sees After the Q1 Beat

The consensus on Keurig Dr Pepper stock is cautiously constructive. Of the 17 analysts covering KDP as of May 22, 2026, 6 rate it a Buy, 4 Outperform, and 7 Hold, with no Sell ratings. The Street mean target sits at around $33, implying roughly 14% upside from the current price of around $29.

The Street high of $42 points to a scenario where the separation unlocks full pure-play re-ratings for both businesses, with investors willing to assign beverage-peer multiples to a standalone refreshment business running at double-digit growth.

The core driver investors are tracking is EPS recovery. Q1 normalized EPS of $0.39 fell 7.1% year over year, hurt by the lapping of a one-time gain and peak coffee cost headwinds. But the estimates table shows the trajectory turning sharply: consensus sees normalized EPS of $0.54 in Q2 2026, $0.63 in Q3, and $0.72 in Q4, a profile consistent with management’s guidance for high single-digit EPS growth in Q2 and further acceleration in the back half.

KDP’s revenue growth carries the same shape. Q1 actuals of $3.98 billion will expand significantly in Q2 through Q4 as the JDE Peet’s contribution flows in for a full three quarters, with consensus revenue estimates of around $7 billion for Q2 and Q3.

The tension sits in the EBITDA margin line. Q1 EBITDA margins compressed to 25.2% from the prior year, weighed down by green coffee cost inflation and elevated SG&A. Consensus sees margins recovering toward 25% to 26% by year-end, but the coffee cost pass-through lag means any lingering commodity pressure could delay that recovery into 2027.

The Street’s median target of around $33 implies that KDP stock is undervalued at around $29 once the transitory coffee headwinds normalize, a view that requires holding through a messy integration year with limited earnings clarity until the separation is finalized.

Is KDP Stock Worth $40? TIKR’s Base Case and the Separation Assumption Behind It

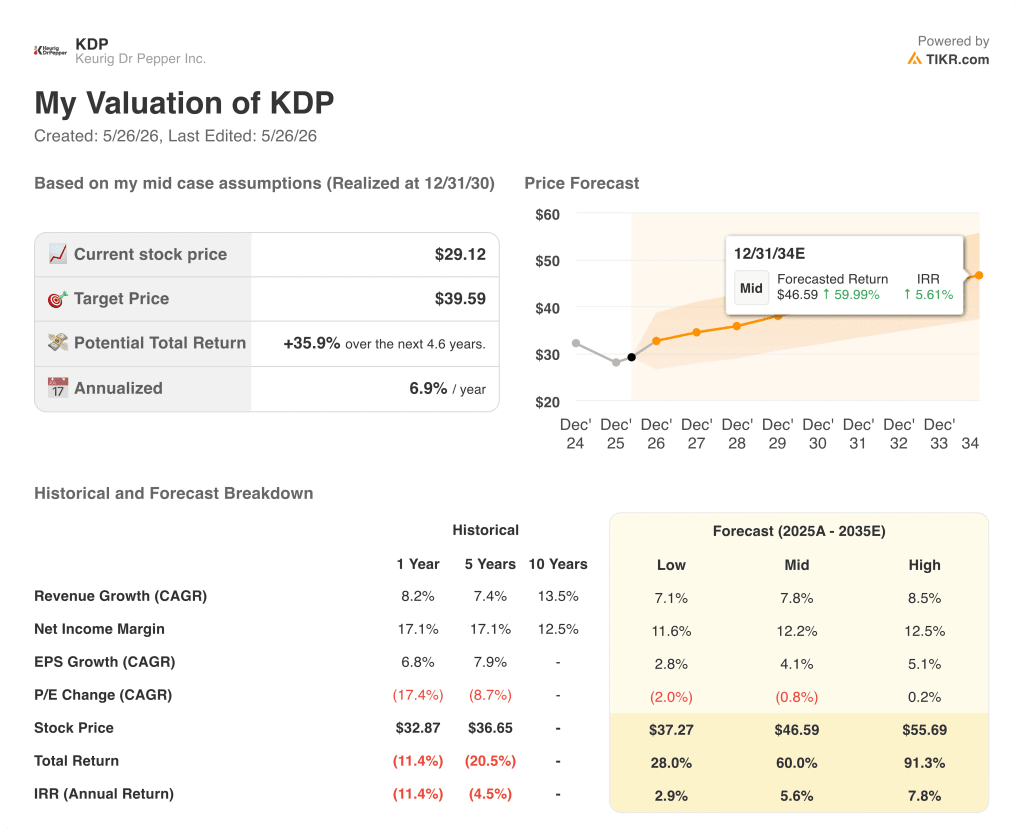

TIKR’s base case values Keurig Dr Pepper stock at around $40 by December 2030, implying a total return of around 36% from the current price of around $29, or roughly 7% annualized over the next 4 and a half years.

The mid-case model assumes revenue growing at around 8% annually, net income margins of around 12%, and EPS growing at around 4% per year, with the P/E multiple contracting modestly over time. Extending that model to a 2035 horizon, the mid case reaches a stock price of around $47, a total return of around 60%, and an IRR of around 6%.

If the separation executes cleanly and the beverage business sustains its double-digit growth profile, the high case prices KDP stock at around $56 by 2035, implying a total return of around 91% and an IRR of around 8%.

If coffee integration stalls, leverage reduction lags, or the separation slips past 2027, TIKR’s low case produces a stock price of around $37 by 2035, a total return of around 28% and an IRR of around 3%.

At around $29, Keurig Dr Pepper stock is undervalued relative to the mid-case assumptions in TIKR’s model, but realizing that value depends on one condition: the separation delivering two credibly independent companies with distinct capital allocation frameworks. The TIKR data makes the upside case clear. So does the variable that could delay it.

Is Keurig Dr Pepper stock a buy right now?

The Street mean target of around $33 implies roughly 14% upside from the current price of around $29, with 10 of 17 analysts rating KDP a Buy or Outperform.

TIKR’s base case adds a longer-duration view, pricing KDP at around $40 by December 2030.

The key condition is successful execution of the Beverage Co. and Global Coffee Co. separation, targeted for early 2027.

What do analysts say about KDP stock?

As of May 22, 2026, 6 analysts rate KDP a Buy, 4 Outperform, and 7 Hold.

The Street mean target is around $33. The Street high target is $42, anchored to scenarios where the separation unlocks full pure-play re-ratings for both businesses. No analysts currently have Sell ratings on KDP.

What happened to Keurig Dr Pepper stock in Q1 2026?

Keurig Dr Pepper stock rose sharply after Q1 2026 results posted net sales of $3.98 billion, beating consensus estimates of $3.84 billion, and adjusted EPS of $0.39 against a $0.37 estimate. U.S.

Refreshment Beverages drove the beat with 11.9% net sales growth, while the U.S. Coffee segment declined 2.3%, weighed by trade inventory adjustments and peak green coffee cost inflation.

Should You Invest in Keurig Dr Pepper Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Keurig Dr Pepper stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Keurig Dr Pepper stock alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze KDP stock on TIKR for Free →