Key Stats for American Tower Stock

- 52-Week Range: $165 to $234

- Current Price: $183

- Street Mean Target: $216

- Analyst Consensus: 14 Buys / 5 Outperforms / 6 Holds

- TIKR Model Target (Dec. 2030): $

American Tower Beats Q1 Estimates and Raises Full-Year Guidance as DISH Overhang Clears

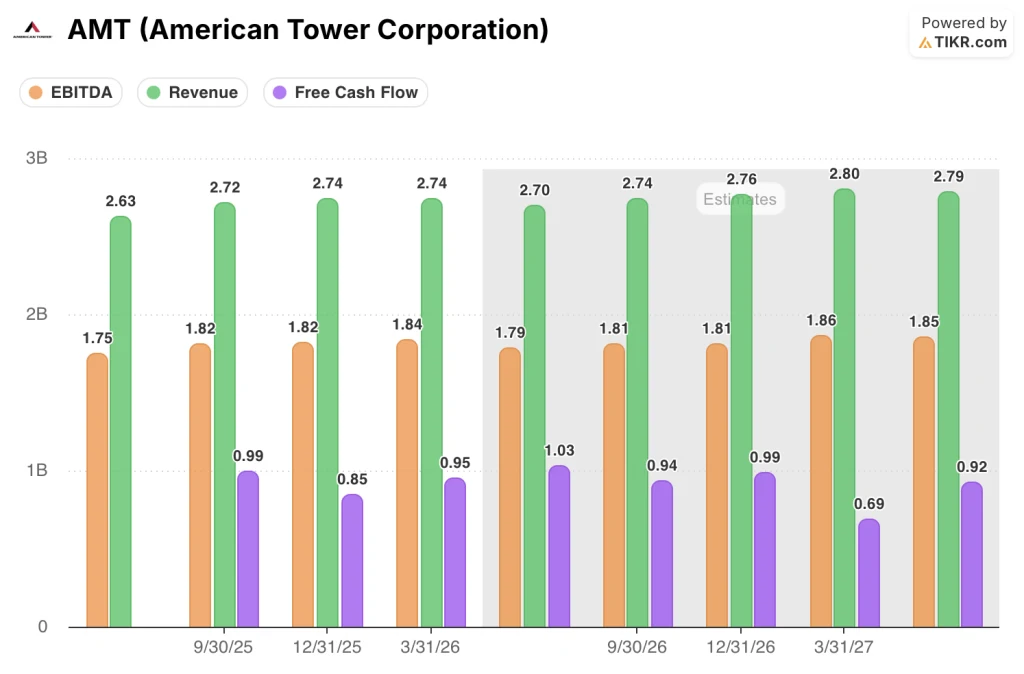

American Tower Corporation (AMT), the world’s largest independent wireless tower and data center landlord, raised its full-year 2026 outlook following Q1 results that beat on both revenue and earnings, with Q1 revenue coming in at $2.74 billion against a consensus estimate of $2.66 billion and EPS of $1.84 against an estimate of $1.60.

The beat was not a one-quarter anomaly.

Property segment revenue, representing the core site-leasing business, grew 7.3% year over year to $2.67 billion, driven by 5G densification demand, accelerating cloud adoption, and what CEO Steve Vondran described on the Q1 2026 earnings call as “rapidly expanding AI-driven workloads.”

The company now guides for full-year total property revenue between $10.59 billion and $10.74 billion, up from a prior range of $10.44 billion to $10.59 billion, with adjusted EBITDA of $7.23 billion at the midpoint.

Beneath the headline, the more consequential development is the removal of DISH from forward guidance entirely.

DISH Network, the satellite television and wireless carrier, had signed a long-term lease agreement with American Tower in 2021 to use tower space as it built out a 5G network across the U.S. — but DISH defaulted on that agreement, stopped making payments, and ultimately sold its spectrum to AT&T (T) , collapsing the build plan entirely.

DISH-related churn had been the single loudest noise in AMT’s story for over a year: an event-driven headwind that stripped around $200 million in annual U.S. revenue from the run rate and compressed reported AFFO per share growth to roughly 2% for 2026.

With DISH now derisked out of guidance, any recovery in the DISH litigation or spectrum redeployment by AT&T becomes pure upside to numbers the Street is already standing behind.

Bernstein’s upgrade to Outperform in May, citing the structural case for towers alongside CoreSite’s AI-driven momentum, was the clearest signal yet that the analyst community is beginning to reprice the stock for the post-DISH baseline.

CoreSite, AMT’s data center subsidiary, delivered approximately 17% property revenue growth in Q1 when excluding noncash straight-line revenue, driven by sustained enterprise demand for hybrid cloud deployments and an accelerating pipeline of AI-related inferencing workloads.

Vondran called the interconnection activity an “inflection point” and stated on the earnings call that “the CoreSite platform drives resilient leasing demand while capturing a high-margin interconnection revenue stream.”

AMT also repurchased around $184 million of stock during Q1 and an additional $19 million through April 21, bringing cumulative buybacks since Q4 2025 to over $565 million.

The capital allocation signal matters: management is putting money behind the thesis that AMT stock is cheap at these levels.

Wall Street Sees 17% Upside to the Mean and No Sells on the Board

The analyst community has reached a clear directional conclusion on American Tower stock: 14 Buys, 5 Outperforms, and 6 Holds with no Underperforms and no Sells among 25 active analysts.

The Street mean target of around $216 implies roughly 17% upside from the current price of around $184, while the high target of $260 reflects what the most constructive analysts see if CoreSite’s AI pipeline converts faster than consensus and U.S. tower organic growth reaccelerates to mid-single digits in 2027.

The thesis the majority is standing behind is a re-rating on transformation: DISH churn rolls off, the underlying mid-single-digit organic tenant billings growth becomes visible again, and CoreSite compounds at double digits on top of a stable tower base.

AMT’s Q2 2026 EBITDA is estimated at around $1.79 billion, roughly flat year over year, before DISH-adjusted growth accelerates later in the year as the churn base period is lapped.

Q2 2026 revenue is also estimated at around $2.70 billion, reflecting the 2.7% year-over-year growth rate in the TIKR actuals and estimates table, a controlled deceleration from Q1 before the DISH noise fully exits the year-over-year comparison.

Meanwhile, Q2 2026 FCF is estimated at around $1.03 billion, implying a roughly 38% FCF margin for the period per the TIKR actuals and estimates table.

At around $184, American Tower stock is undervalued relative to the Street consensus and to the intrinsic picture the TIKR model builds from the company’s own growth assumptions.

The key variable to watch: how quickly AI inferencing workloads scale into CoreSite facilities, because that single factor separates the $216 mean from the $260 high target faster than any tower metric will.

Is American Tower Stock Undervalued in 2026? TIKR’s $315 Mid-Case and the Private Market Discount

TIKR’s base case values American Tower at around $315 by December 2030, implying roughly 71% total return from the current price of around $184, or approximately 12% annualized over the next 4 and a half years.

If revenue grows at roughly 5% annually with net income margins near 32% and modest P/E expansion, the TIKR mid-case stock price reaches around $427 by 2035, representing a roughly 133% total return and an IRR of approximately 10%.

If growth underperforms and P/E contracts slightly, the low case produces a stock price of around $357 and an IRR of roughly 8%, still a positive return from today’s price over the full period.

If AI workloads accelerate CoreSite revenue beyond the base case and mobile data traffic doubles on schedule, the high case reaches a stock price of around $497 and an IRR of approximately 12%.

The tension in the TIKR model is not operational: AMT’s 10-year historical revenue CAGR is 8.4%, and the mid-case assumes only roughly 5%.

The tension is the public market discount.

CFO Rod Smith named it directly at the JPMorgan conference in May, noting that private buyers value tower assets at materially higher multiples than public markets because they take a long-term view and see past event-driven noise like the DISH churn.

AMT’s current price-to-NAV of 0.78x, against a NAV estimate of around $235 per share in the TIKR Street Estimate table, is precisely that discount: a stock the private market would buy at a premium, trading in the public market at a discount to its own appraised value.

The DISH churn is now derisked. The CoreSite inflection is visible in the Q1 results. The buyback is running. American Tower stock is undervalued, and the data the TIKR model is built on has been available to institutional investors for months.

Is American Tower Stock a Buy Right Now?

The Street consensus is Buy, with 14 Buys and 5 Outperforms among 25 analysts and no Sells on the board.

The mean target of around $216 implies roughly 17% upside from the current price of around $184. TIKR’s mid-case model extends that view further, targeting around $315 by December 2030, or roughly 71% total return.

The key condition: DISH churn exits the year-over-year comparison cleanly and CoreSite’s AI inferencing pipeline continues to convert at Q1’s pace.

What Is the Price Target for AMT Stock?

The Street mean target for AMT stock is around $216, with the high at $260 and the low at $195, based on 22 active price estimates in the TIKR data table.

TIKR’s mid-case valuation model targets around $315 by December 2030 based on roughly 5% revenue CAGR, roughly 32% net income margins, and modest multiple expansion.

The gap between the Street one-year target and the TIKR five-year model reflects the duration premium embedded in tower infrastructure assets.

Should You Invest in American Tower Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up American Tower Corporation stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track American Tower Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze AMT stock on TIKR for Free →