Key Stats for Amazon Stock

- Current Price: $266.32

- Street Target: ~$313

- Target Price (Mid): ~$668

- Potential Total Return: ~151%

- Annualized IRR: ~22% / year

- Earnings Reaction: +0.77% (Q1 2026, reported April 29, 2026)

- Max Drawdown: 21.74% (2/13/26)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

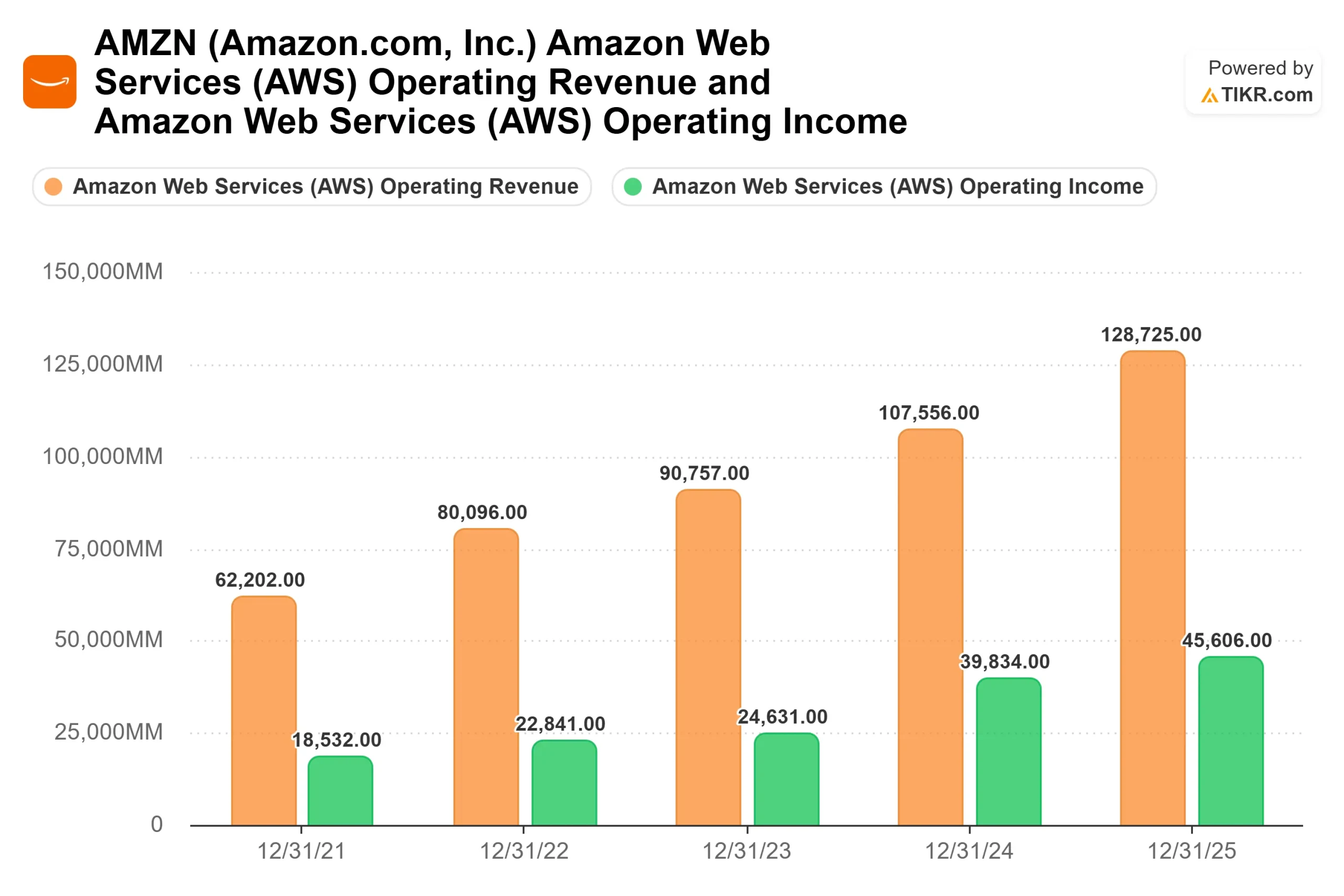

Amazon.com (AMZN) reported what may be its best quarter ever on April 29, 2026, and the stock gained 0.77%. Revenue of $181.5 billion cleared the $177.2 billion consensus. Adjusted EPS of $2.78 nearly doubled the $1.64 Wall Street model, per TIKR’s Beats & Misses data. AWS grew 28% year-over-year, its fastest rate in 15 quarters, at a 37.7% operating margin. Operating income of $23.9 billion produced a 13.1% company-wide margin that CFO Brian Olsavsky called the highest Amazon has ever recorded on the Q1 2026 earnings call.

The market barely reacted because of what the cash flow statement showed. Q1 capital expenditures hit $43.2 billion, up from $24.3 billion in Q1 2025 per TIKR data, sending quarterly free cash flow to -$17.2 billion. Amazon has committed to roughly $200 billion in 2026 spending, the majority directed at AI data centers and custom silicon. For investors pricing stocks on near-term cash generation, the stock looks broken.

But Amazon’s own history argues otherwise. CEO Andy Jassy was direct on the call: “We’ve been through this cycle with the first big AWS growth wave and we like the results. We expect to feel similarly about this next wave with much larger potential downstream revenue and free cash flow.” The last time CapEx crushed Amazon’s cash flow this decisively, the company was building the infrastructure that became a $150 billion annualized revenue business. The TIKR model sees roughly $668 by December 31, 2030. The gap between that and today’s $266.32 is the question the market has not yet answered.

Why the Market Is Scared of the Right Thing

The fear is legitimate. TIKR’s forward estimates project free cash flow remaining negative through 2026 before recovering. The NTM Market Cap / Free Cash Flow multiple sits at -546x per TIKR data. But the spending is not consumption. Jassy explained on the call that data centers carry 30-plus-year useful lives and chips carry five to six years. The CapEx deployed today creates assets that generate revenue for years after construction ends.

The demand behind those assets is already contracted. The AWS backlog stood at $364 billion at Q1-end, excluding a recently announced Anthropic deal, Jassy said, which was worth over $100 billion. Amazon holds over $225 billion in Trainium revenue commitments from AI labs, including Anthropic and OpenAI, per Jassy on the call. This is pre-sold capacity against spending that investors are treating as speculative.

See historical and forward estimates for Amazon stock (It’s free!) >>>

Three Engines Accelerating at Once

AWS and AI is the primary lever. Amazon’s AI revenue run rate inside AWS has crossed $15 billion, growing triple digits year-over-year. Bedrock, Amazon’s managed model platform giving developers access to Anthropic, OpenAI, Meta, and Amazon’s own Nova models, processed more tokens in Q1 than all prior years combined, with customer spend up 170% quarter-over-quarter, per Jassy on the call.

Advertising generated $17.2 billion in Q1 2026, up 22% year-over-year per the earnings call. It is high-margin revenue that requires minimal incremental CapEx and cross-subsidizes the infrastructure buildout from within.

Retail and fulfillment are becoming more efficient as they scale. North America’s operating income hit $8.3 billion at a 7.9% margin. Unit growth of 15%, the highest since the COVID era, per CFO Brian Olsavsky, outpaced outbound shipping cost growth of 12%, meaning the network is getting cheaper to operate as volume rises.

What the Spending Buys

The CapEx is funding four bets with distinct return profiles. The largest is AWS AI infrastructure, where capacity is already pre-sold. Trainium2, Amazon’s AI chip offering around 30% better price performance than comparable GPUs per Jassy, is largely sold out. Trainium3 is shipping and nearly fully subscribed. Trainium4, still 18 months from availability, is already heavily reserved.

The second is Amazon Leo, the company’s low Earth orbit satellite internet service targeting commercial launch in Q3 2026. Enterprise customers are already signed, including Delta Airlines (which committed at least half its fleet from 2028), JetBlue, AT&T, Vodafone, and NASA, per Jassy on the call. In April 2026, Amazon announced it would acquire Globalstar to add direct-to-device satellite capabilities and entered a partnership with Apple to power satellite connectivity for iPhones and Apple Watches. Jassy on the call: “The business has a chance to be a very large many-billion-dollar revenue business.”

The third is retail delivery speed, pulling Prime members toward baskets that are three times larger. The fourth is Amazon’s custom chip business, which has crossed a $20 billion annualized revenue run rate growing at triple-digit percentages year-over-year, per Jassy on the call.

See how Amazon performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $266.32

- Target Price (Mid): ~$668

- Potential Total Return: ~151%

- Annualized IRR: ~22% / year

See analysts’ growth forecasts and price targets for Amazon stock (It’s free!) >>>

The TIKR mid case assumes a revenue compound annual growth rate of around 12% through 12/31/30. The two primary revenue drivers are AWS accelerating as enterprise AI moves from pilot to production, and advertising compounding as Amazon deepens its commerce media position. The margin driver is the free cash flow recovery: TIKR’s forward estimates project FCF turning from negative in 2026 to around $176 billion by 2030 as CapEx growth decelerates and installed capacity monetizes.

The upside path: AWS backlog converts faster than modeled, Trainium gains meaningful external chip-sale revenue, and Amazon Leo adds a revenue leg before 2030. The risk: AI demand softens before installed capacity is monetized, FCF stays compressed longer than estimated, and ongoing FTC antitrust litigation produces structural changes to the marketplace.

The Street consensus sits at around $313 per TIKR data, implying roughly 17% upside. The TIKR mid case at around $668 looks through the CapEx trough to the monetization wave on the other side.

Conclusion

The signal that confirms or breaks this thesis is not AWS revenue; that story is already in the price. Watch the quarter when Amazon’s CapEx growth rate starts decelerating relative to revenue growth. TIKR’s forward estimates place that inflection in 2027, when free cash flow is projected to turn materially positive. If it arrives on schedule, the overhang that held the stock to a 0.77% gain on its best quarter ever begins to lift.

The TIKR mid case says the stock will more than double from here by December 31, 2030. The market is pricing the fear. The model is pricing the recovery.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Amazon?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Amazon, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Amazon alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!