Key Stats for ResMed Stock

- 52-Week Range: $199 to $294

- Current Price: $208

- Street Mean Target: $271

- Street High Target: $340

- Analyst Consensus: 8 Buys / 3 Outperforms / 7 Holds / 1 Sell

- TIKR Model Target (June 2030): $311

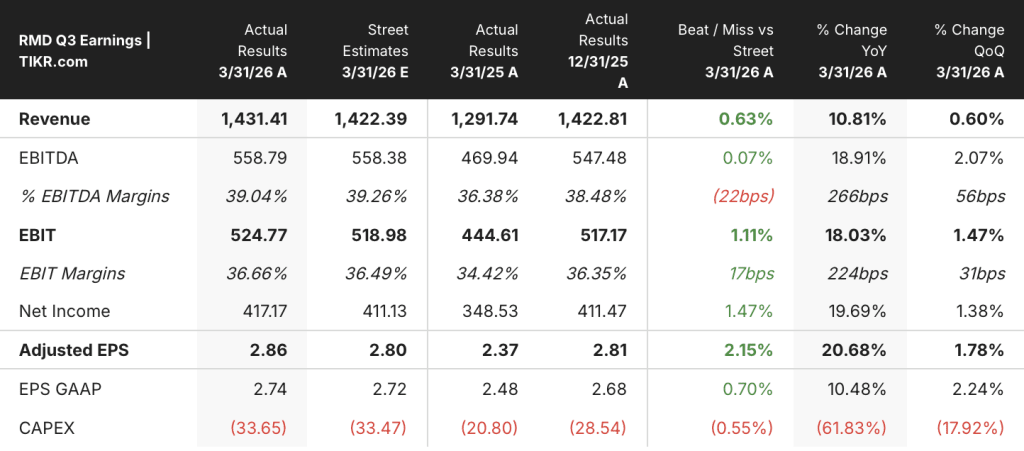

ResMed Beats Q3 Estimates as GLP-1 Data Flips the Script on Threat Narrative

ResMed Inc. (RMD), the global leader in CPAP and sleep apnea therapy, reported fiscal Q3 2026 results on April 30 with revenue of $1.43 billion — up 11% year-over-year and ahead of the $1.42 billion street estimate.

Adjusted EPS came in at $2.86, beating the consensus of $2.80 and rising 21% from the year-ago period.

The beat was broad-based: device sales grew 6% globally on a constant-currency basis, while masks and accessories grew 12%, with the Americas mask segment posting double-digit growth even after stripping out the contribution from the VirtuOx acquisition.

The operating leverage story held. Gross margin expanded 290 basis points year-over-year to 62.8%, driven by component cost improvements, manufacturing efficiencies, and freight optimization — with management guiding full-year gross margin firmly in the 62% to 63% range.

Free cash flow reached $520 million in the quarter, again exceeding 100% conversion, funding $175 million in share repurchases and a $0.60 per share dividend.

The company also announced the $340 million acquisition of Noctrix Health, targeting the restless legs syndrome market with an FDA de novo-classified nerve stimulation device called Nidra, which CEO Mick Farrell described as growing faster than ResMed with higher gross margins.

The most analytically significant development had nothing to do with the quarter’s headline numbers.

ResMed presented real-world data from a 1.7 million-patient cohort showing that PAP patients who subsequently start GLP-1 therapy have resupply rates that are 5.1% higher at two years and 6.2% higher at three years than PAP-only patients — directly inverting the premise that GLP-1 drugs cannibalize CPAP demand.

Farrell was direct on Q3 2026 earnings call: “We believe GLP-1s are truly a megatrend and a once-in-a-generation demand gen opportunity for ResMed.”

A separate 2.1 million-patient claims analysis found that patients with prescriptions for both PAP and GLP-1 are approximately 11% more likely to initiate PAP therapy than those with a PAP prescription alone.

Despite Apnimed’s experimental pill AD109 meeting its late-stage trial goal of reducing sleep apnea breathing interruptions, management pushed back hard on the device substitution narrative, noting that CPAP eliminates apnea events in more than 90% of patients — a bar no pharmaceutical option currently meets.

Wall Street Holds a 30% Upside Conviction on RMD Despite the Discount

Wall Street’s current read on ResMed stock is constructive but not unanimous, and the gap between where analysts think the stock belongs and where it trades is unusually wide.

Fifteen analysts covered RMD with 8 Buys, 3 Outperforms, 7 Holds, and 1 Sell — a distribution that leans positive but carries real caution.

The street mean target sits at around $271, implying roughly 30% upside from the current price of $208, which is an unusually wide spread for a company that has delivered consistent execution.

The top analyst target reaches $340, pointing to a scenario where the GLP-1 narrative resolves in ResMed’s favor and organic market growth accelerates.

The thesis most analysts are running is a structural growth compounder: a business with 80% of its addressable sleep apnea market still undiagnosed, a recurring-revenue mask and accessories segment that now generates double-digit annual growth, and a margin profile expanding toward 37% EBIT margins by fiscal 2027 estimates.

EPS is the metric where the forward picture is clearest. TIKR’s estimates table shows consensus EPS of $2.90 for the June 2026 quarter — up around 14% year-over-year — stepping to $3.12 for the March 2027 quarter, a trajectory that assumes sustained high-single-digit revenue growth compounds into faster earnings growth as SG&A scales.

Revenue consensus for the June 2026 quarter sits at around $1.46 billion, growing to approximately $1.53 billion by the March 2027 quarter — the deceleration from Q3’s 11% pace to around 7-8% growth reflects both the harder year-over-year compares and the market’s residual skepticism about sustained device demand.

The key risk analysts are watching is the incoming Noctrix integration cost drag, with management guiding an approximately $0.02 headwind to Q4 non-GAAP EPS, and the ongoing question of whether the Philips competitive re-entry into the U.S. market in 2026 captures any of ResMed’s device share.

RMD is undervalued: a company delivering 21% EPS growth, 62.8% gross margins, and a 1.7 million-patient dataset disproving the central bear thesis does not typically trade at a 29% discount to its street consensus target — and the TIKR model puts a more specific number on that gap.

ResMed’s Margin Architecture: Revenue Compounds, Costs Don’t Follow

Total revenues reached $1.43 billion in the March 2026 quarter, up 10.8% year-over-year, extending a streak of uninterrupted high-single-digit or better top-line growth that stretches back four consecutive quarters across the income statement.

Gross profit rose to $0.90 billion, with gross margins expanding to 62.8% — up from 59.9% in the March 2025 quarter and the highest level in the trailing eight quarters shown in TIKR’s income statement data.

Operating income reached $0.51 billion in the March quarter, with operating margins at 35.3% — a 230-basis-point improvement from the year-ago period and part of a consistent operating leverage pattern where operating income has grown faster than revenue in each of the last four quarters.

Total operating expenses came in at $0.39 billion for the quarter, essentially flat sequentially despite an acceleration in SG&A associated with the VirtuOx integration — a signal that the underlying cost structure is not running away from the top line.

The margin expansion story has legs: from 59.1% gross margins in June 2024 to 62.8% in March 2026, ResMed has added nearly 370 basis points of gross margin in eight quarters while simultaneously accelerating revenue growth — a combination that directly funds the increased R&D and commercial investment management is signaling for fiscal 2027.

Is ResMed Stock Undervalued in 2026? TIKR’s $311 Model Says the Market Is Mispricing the Growth

TIKR’s base case values ResMed at around $311 by June 2030, implying approximately 50% total return from the current price of around $208, or roughly 10% annualized over 4 years.

The mid-case rests on a revenue CAGR of around 8% through 2035 and net income margins expanding toward 30% — consistent with management’s own stated 5-year outlook for high-single-digit revenue growth with earnings growing faster.

The key tension is whether the current multiple contraction, which TIKR’s model embeds as a 4% annualized P/E headwind, acts as a sustained ceiling or mean-reverts as the GLP-1 narrative resolves.

In the low case, revenue growth decelerates to around 7% and net income margins hold near 28% — enough to push the stock to approximately $341 by 2034, delivering around 6% annualized.

This is a scenario where the Philips re-entry creates real device pricing pressure, the Noctrix integration underperforms initial growth expectations, and the market keeps a discount multiple on the name indefinitely. Even here, the return is positive, which says something about the quality of the underlying business.

In the high case, the GLP-1 demand flywheel accelerates, the mask portfolio drives resupply growth above 12% annually, and net income margins approach 31%. In that scenario, the stock reaches around $545 by 2034 at an IRR of approximately 13%.

That is the outcome where the 11% PAP initiation lift from GLP-1 prescriptions compounds across a patient base that is just beginning to feel the pharma demand gen effect, and where the fabric mask platform cements market share gains already visible in the current data.

ResMed stock is undervalued. A company at $208 with a 62.8% gross margin, a demonstrated GLP-1 tailwind confirmed across 2.1 million patients, a decade of 10%+ revenue CAGRs, and a mid-case TIKR target of $311 is not priced for the business it is running — it is priced for a disruption that the data has not found.

Is ResMed stock a buy right now?

The analyst consensus as of May 2026 leans bullish, with 8 Buys, 3 Outperforms, and 7 Holds across 15 analysts covering RMD. The street mean target of around $271 implies roughly 30% upside from the current price of around $208.

TIKR’s mid-case valuation model sets a target of around $311 by June 2030, implying around 50% total return. The key variable is whether the GLP-1 narrative continues to resolve as a demand tailwind rather than a device substitution threat, which the current data — including a 2.1 million-patient claims analysis showing 11% higher PAP initiation — supports.

Should You Invest in ResMed Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up ResMed Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track ResMed Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze RMD stock on TIKR for Free →