Key Stats for Autodesk Stock

- Current Price: $240.99

- Target Price (Mid): ~$429

- Street Target: ~$325

- Potential Total Return: ~78%

- Annualized IRR: ~13% / year

- Earnings Reaction: +5.32% (February 26, 2026)

- Max Drawdown: 33.15% (April 10, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Autodesk (ADSK) has had one of the stranger years in large-cap software. The business keeps beating estimates. The stock keeps getting sold.

ADSK closed at $240.99, down 27% from its 52-week high of $329.09 and just $27 above a 52-week low of $214.10. Five consecutive quarters of beating analyst expectations on revenue, EBITDA, and free cash flow have not stopped the slide. The market’s concern centers on a 7% workforce reduction in January 2026, the fading tailwind from Autodesk’s new transaction model, and a sector-wide rotation out of application software that pushed Citi to cut the stock to Neutral in April. ADSK hit a 33.15% maximum drawdown on April 10.

CFO Janesh Moorjani presented at the Morgan Stanley Technology, Media & Telecom Conference on March 4 and made one of the cleaner articulations of Autodesk’s AI and platform thesis this cycle. What he said about data moats, lifecycle expansion, and consumption-based monetization tells a different story than the one the stock price reflects. With Q1 fiscal 2027 earnings arriving Thursday, May 28, that gap gets its first real test.

The Quarter That Should Have Mattered More

Q4 fiscal 2026, reported February 26, was clean across every metric. Revenue grew 19% year-over-year to $1.957 billion, ahead of the $1.912 billion consensus. Adjusted EPS came in at $2.85 against a $2.64 estimate. Free cash flow for the quarter reached $972 million. The stock rose 5.32% that day, then spent six weeks giving most of it back.

The problem was the narrative, not the numbers. In January, Autodesk cut roughly 7% of its global workforce, approximately 1,000 employees, primarily in customer-facing sales roles. At Morgan Stanley, Moorjani described this as “the final phase of an overall business model transition” a deliberate reallocation, not a retreat. Restructuring savings are being reinvested into new seller profiles, marketing, and AI and platform R&D.

The operating margin effect is modest. Autodesk guided for around 75 basis points of expansion in fiscal 2027, absorbing roughly 100 basis points of accounting headwind from the transaction model while still reflecting real underlying leverage. Consensus on TIKR projects EBITDA margins growing from 40.7% in fiscal 2026 toward around 41% in fiscal 2027 and around 44% by fiscal 2029.

Moorjani acknowledged the sales org risk directly: “There’s near-term disruption in the sales organization associated with the implementation of [the new structure] and the expansion teams.” That candor explains part of why the stock has been punished. It also suggests management is executing a deliberate transition rather than reacting to deteriorating demand.

See historical and forward estimates for Autodesk stock (It’s free!) >>>

Three Moats the Market Is Underpricing

At Morgan Stanley, Moorjani distilled Autodesk’s AI competitive position into three things: data, context, and expertise.

On data, Autodesk has trained its foundation models on project data from hundreds of thousands of customers accumulated over decades, none of which is available in the public domain. As Moorjani said: “We have the rights to train our models on their data, which allows us to build much more powerful capabilities.” Competitors working from publicly available datasets are at a structural disadvantage for design and construction applications.

Context is the second layer. Autodesk’s workflows carry embedded project intelligence, regulatory dependencies, mechanical system relationships, and cost implications of design changes. Moorjani made this concrete: “When you move that wall, what do you do about all the things you can’t see?” A general-purpose model cannot answer that. Autodesk’s can.

Expertise is the third element. Moorjani noted that 3D AI skills are among the scarcest in the industry, and Autodesk has been building that bench for nearly a decade. Project Bernini, the company’s foundational generative AI model for 3D, originated in internal research labs, a runway competitors cannot quickly replicate.

The monetization path runs across three tiers: task automation delivered through existing subscriptions; then workflow and system-wide automation, carrying consumption-based pricing as workloads become more compute-intensive. Moorjani noted that 17% of Autodesk’s business was already in consumption-based models in fiscal 2025, and the go-to-market infrastructure for this shift already exists. The gross margin headwind from heavier compute is acknowledged and, per Moorjani, was already factored into the company’s long-term targets.

The Lifecycle Expansion Nobody Is Fully Pricing

Autodesk Construction Cloud is gaining traction precisely in the segments with the deepest pipelines. Data center construction is one of the strongest demand drivers, Moorjani highlighted. According to the Associated Builders and Contractors, U.S. construction backlog reached 8.8 months in April 2026, driven heavily by data center megaprojects, with contractors in digital infrastructure carrying substantially longer backlogs than the industry average. Moorjani noted that construction customers typically carry 8 to 10 months of project backlog capacity constraints that make technology adoption a necessity, not a choice.

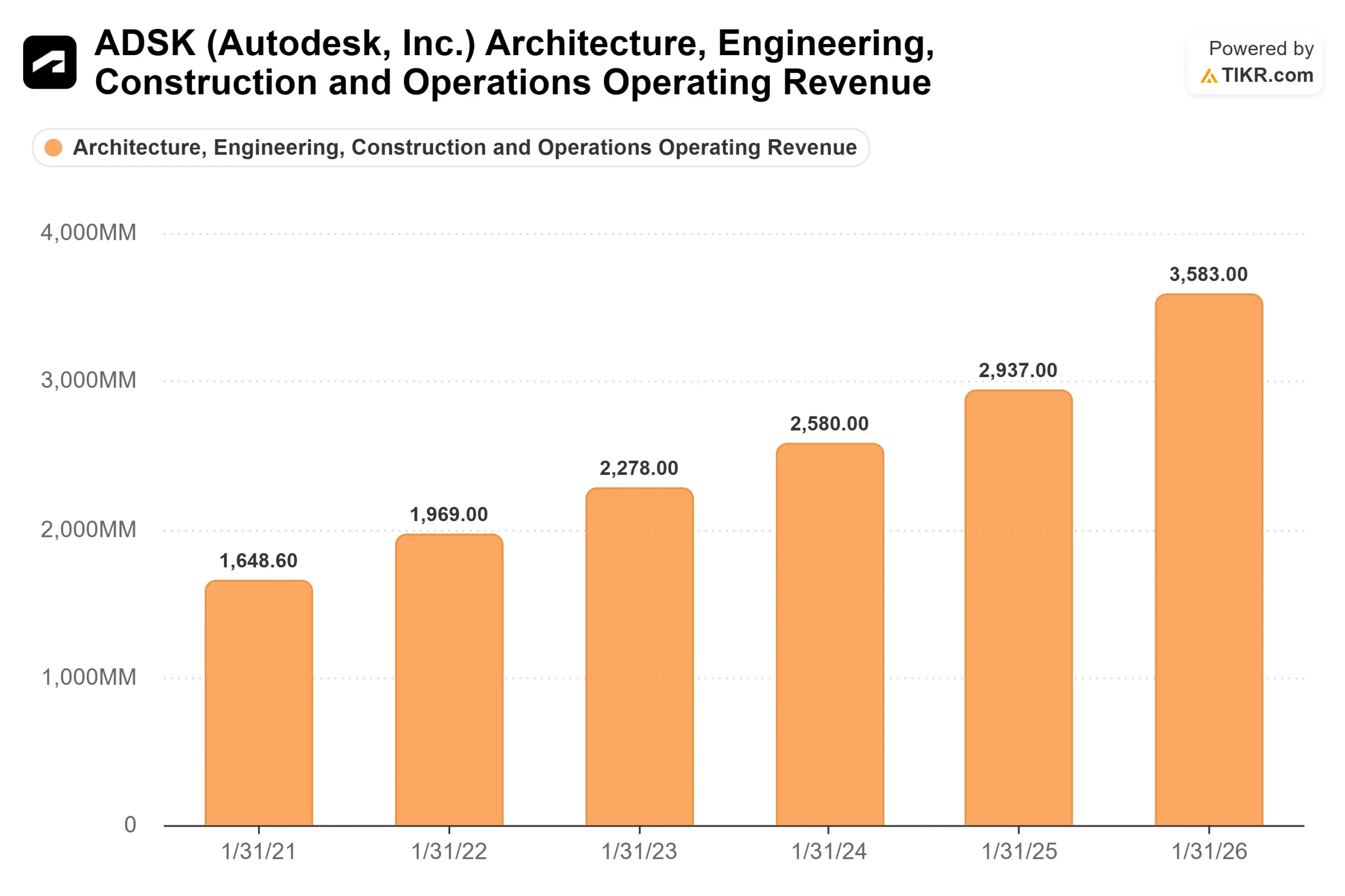

On manufacturing, Fusion, Autodesk’s cloud-based computer-aided manufacturing and engineering platform, is expanding into ten-to-twenty-seat midsized accounts beyond its historical one-to-five-seat base. Per TIKR segment data, Manufacturing revenue grew from $1,189 million in fiscal 2025 to $1,379 million in fiscal 2026, a 16% gain. Architecture, Engineering, Construction, and Operations revenue reached $3,583 million in fiscal 2026, up from $2,937 million the prior year.

The operations layer is the most forward-looking. Moorjani described ambitions spanning both building and manufacturing operations, with an approach mirroring Autodesk’s entry into construction: anchor acquisitions followed by organic buildout. If that lifecycle closes, Autodesk’s involvement with a project shifts from years to decades.

Is ADSK Undervalued Right Now?

Despite five straight beats, ADSK trades at 15.16x NTM EV/EBITDA and 19.40x NTM P/E right around the peer group mean of 14.84x NTM EV/EBITDA. Direct design software peers PTC and Dassault Systèmes trade at 12.89x and 10.55x NTM EV/EBITDA, respectively, with narrower platform footprints. Autodesk is not demanding a premium relative to comparable businesses, which is unusual given its free cash flow profile and margin expansion trajectory.

The 32 analysts covering ADSK include 24 Buys, 6 Outperforms, and 3 Holds, with a mean Street target of ~$325, about 35% above the current price. BofA reinstated coverage at Buy on May 12, with a $300 target, citing Autodesk’s data, 3D context, and decade-long AI investment as structural advantages that are hard to replicate.

See how Autodesk performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $240.99

- Target Price (Mid): ~$429

- Potential Total Return: ~78%

- Annualized IRR: ~13% / year

See analysts’ growth forecasts and price targets for Autodesk stock (It’s free!) >>>

The TIKR mid-case model assumes a revenue CAGR of around 8% from fiscal 2026 through January 2031, a deceleration from the 17.5% one-year rate, but consistent with the 10-year historical average of 11.1%. This is not a hypergrowth story. The return is driven by margin expansion and multiple normalization, not revenue acceleration.

The two primary growth drivers are AECO subscription expansion sustained by construction backlog depth and the platform’s push into operations, and Fusion’s move upmarket into midsized manufacturing accounts. The margin driver is subscription operating leverage as restructuring savings compound, with net income margins reaching around 33% in the mid case. The primary risk is go-to-market execution: if sales force restabilization takes longer than expected, new business billings could disappoint in fiscal 2027’s first half, compressing the valuation multiple further before the recovery builds.

Conclusion

The thing to watch on Thursday is whether Q1 fiscal 2027 results confirm that go-to-market disruption is fading. Consensus expects $1.893 billion in revenue and $2.84 in adjusted EPS. The numbers matter less than the commentary. Moorjani said at Morgan Stanley that near-term friction was “baked into guidance.” A beat with stable or raised full-year guidance would confirm that view and begin closing the gap between a $241 stock and a ~$325 Street consensus target.

If billings disappoint or guidance gets trimmed, the thesis extends rather than breaks. Autodesk’s construction backlog demand, data center pipeline, Fusion expansion, and operations lifecycle ambitions are multi-year drivers. The threshold for Thursday is simple: management needs to signal that disruption peaked in Q1, not that it is still building.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Autodesk?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Autodesk, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Autodesk alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Autodesk on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!