Key Stats for Advanced Micro Devices Stock

- Current Price: $467.51

- Target Price (Mid): ~$1,742

- Street Target: ~$472

- Potential Total Return: ~273%

- Annualized IRR: ~33%/year

- Earnings Reaction: +18.61% (5/5/26)

- Max Drawdown: 27.76% (3/3/26)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Advanced Micro Devices (AMD) just triggered one of the most aggressive post-earnings analyst re-ratings in the semiconductor sector in years. On May 6, Goldman Sachs upgraded AMD to Buy and raised its price target to $450 from $240, an 88% increase in a single note. Bernstein went further, upgrading to Outperform and nearly doubling its target to $525 from $265. Both firms arrived at the same conclusion: AMD is no longer just competing in AI chips. It is becoming the infrastructure that the entire AI buildout depends on.

The stock surged 18.61% on May 5. The Street consensus mean now sits at around $472, essentially where AMD is trading today, meaning the old target has already been lapped. The Street’s full target range runs from $225 to $625, which tells you how wide the disagreement is. Goldman and Bernstein are near the top of that range, but not alone. Morgan Stanley raised its target to $410 from $360, keeping an equal-weight rating but acknowledging the CPU story has more room to run than the market has priced in.

Who is closer to being right? The Q1 earnings call transcript answers this better than any press release.

What the Upgrades Are Actually Pricing In

Goldman’s upgrade rests on a specific thesis about agentic AI (AI systems that autonomously execute multi-step tasks, requiring far more compute than traditional workloads). Analyst James Schneider’s framework applies a 30x multiple to a $15 normalized EPS estimate, arriving at the $450 target. Goldman’s own 2027 and 2028 EPS estimates are reportedly around 20% above Wall Street consensus, reflecting confidence in AMD’s ability to sustain revenue compound annual growth rates well above 40% for multiple years.

Bernstein’s call is anchored on earnings power. The firm now models AMD delivering more than $14 in EPS in 2027 and said approaching $20 in 2028 “feels plausible assuming the AI boom continues.” For context, TIKR’s consensus has AMD at around $13 in normalized EPS for 2027, meaning Bernstein is sitting materially above the Street.

What separates these from routine post-earnings bumps is that each target requires AMD to sustain growth it has not yet proven at scale. The Q1 transcript is where you find out whether the business is actually building toward it.

See historical and forward estimates for Advanced Micro Devices stock (It’s free!) >>>

The Detail That Changes the Math

At AMD’s Financial Analyst Day in November 2025, the company projected the server CPU total addressable market (TAM, the total revenue opportunity across all companies selling data center processors) at approximately $60 billion by 2030, growing at roughly 18% annually. Five months later, on the Q1 call, CEO Lisa Su told analysts that AMD now expects that TAM to grow at greater than 35% annually, reaching over $120 billion by 2030. The TAM more than doubled in five months.

The driver is an agentic AI. “As inferencing scales and you do more agentic AI, they all require CPUs for all of the orchestration and the data processing,” Su said. The logic is mechanical: every GPU rack a hyperscaler deploys needs CPUs to manage it. As AI agents multiply, the CPU-to-GPU ratio inside data centers shifts. Su put numbers to this directly on the call. Traditional configurations run roughly one CPU per four to eight GPUs. As agentic AI scales, that ratio is moving toward 1:1, and in high-agent-density environments, Su suggested it could even invert.

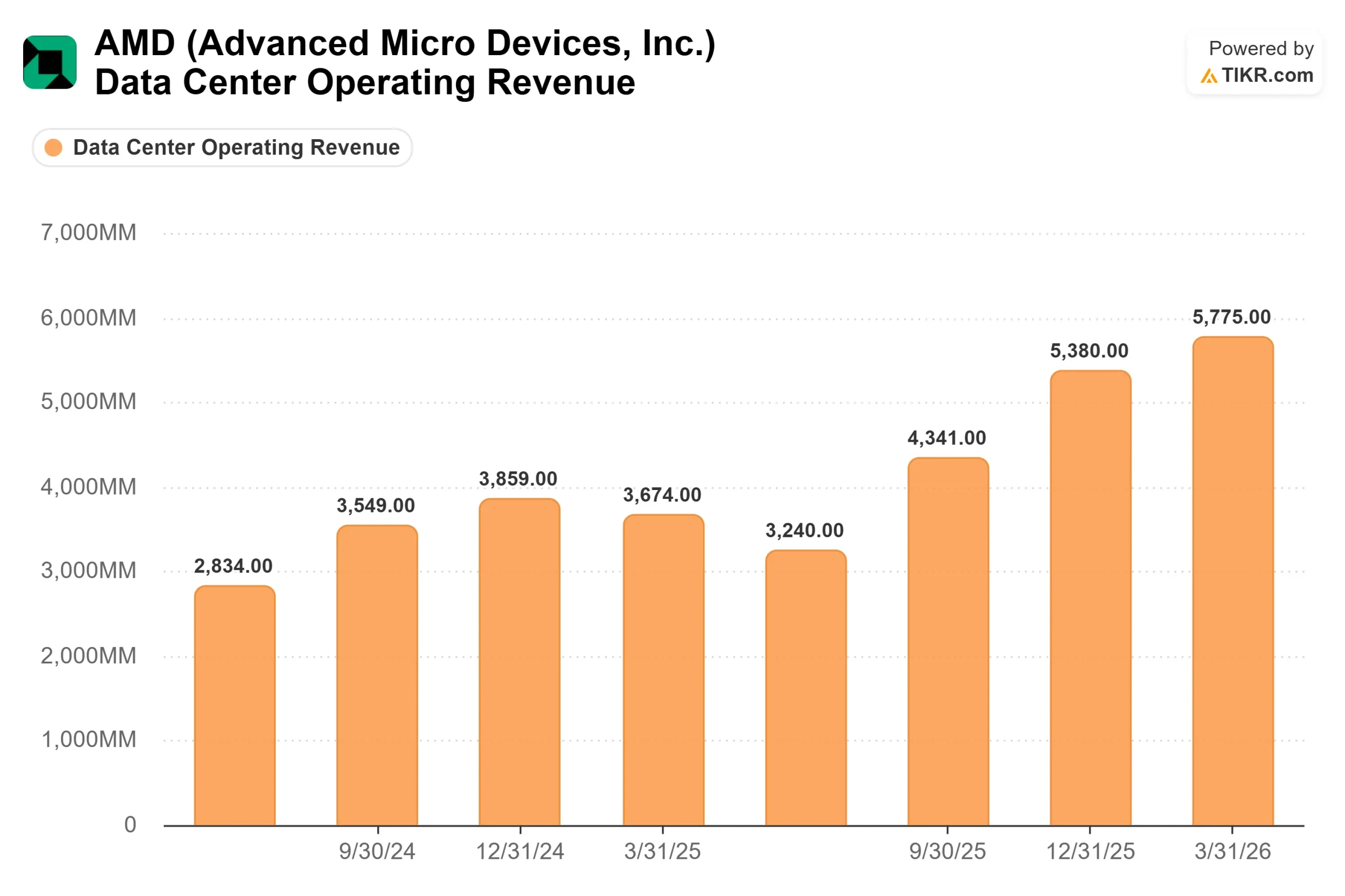

If the ratio shift is structural and sustained, AMD’s server CPU revenue trajectory is not cyclical. It is durable. The Q1 numbers support this view. Data Center revenue hit a record $5.8 billion, up 57% year-over-year, with server CPU revenue growing more than 50% year-over-year. AMD’s fifth-generation EPYC Turin processor crossed 50% of the server CPU revenue mix for the first time. Every major cloud provider expanded its EPYC footprint, and AMD-powered cloud instances grew nearly 50% year-over-year to more than 1,600. For Q2 2026, AMD guided server CPU revenue growth above 70% year-over-year.

The GPU Side: Contracted, but Not Yet Proven

The Instinct GPU business is where the upgrade debate is sharpest. Two contracted anchor relationships give AMD multi-year visibility: a multi-generation agreement with Meta for up to 6 gigawatts of Instinct GPUs, including a custom MI450-based accelerator, and a previously announced partnership with OpenAI. Su confirmed on the call that lead customer forecasts for MI450 are now exceeding initial plans, with a growing number of new customers engaging in multi-gigawatt-scale deployments.

The risk is simple: MI450 and the Helios rack-scale platform (which integrates Instinct GPUs with EPYC Venice CPUs into a fully optimized AI infrastructure system) have not yet generated production revenue. Sampling began in Q1 2026, with production shipments targeting initial volume in Q3 and a significant ramp in Q4. Morgan Stanley called this plainly a “show-me” story. CFO Jean Hu noted that MI450 carries below-corporate-average gross margins in its early production phase, though she guided Q2 non-GAAP gross margin at approximately 56% and expressed confidence in the full-year trajectory toward the company’s 55% to 58% long-term target.

AMD’s ROCm ecosystem (the platform allowing AI developers to run workloads on Instinct GPUs, analogous to CUDA for Nvidia) added day-zero support for Google Gemma 4, Qwen, and Kimi in Q1. Progress is real, but Nvidia’s decade-long developer moat does not close in a single quarter.

Is AMD Undervalued at $467?

AMD’s 46.0x NTM EV/EBITDA sits well above peers on TIKR’s Competitors page: Broadcom at 24.8x and Texas Instruments at 25.1x. That premium is only justified if AMD sustains its growth trajectory.

The free cash flow picture is what makes the bull case credible. AMD generated $2.6 billion in free cash flow in Q1 2026, more than triple the year-earlier figure, representing 25% of revenue. TIKR consensus projects full-year 2026 free cash flow at around $8 billion, up from $5.5 billion in 2025. AMD ended Q1 with $12.3 billion in cash and no meaningful net debt, giving it the balance sheet to sustain heavy R&D investment through the ramp.

TIKR consensus has full-year 2026 revenue at around $49 billion, up roughly 43% from $34.6 billion in 2025. Normalized EPS is expected to be around $7 for 2026, rising toward around $13 in 2027 as operating leverage expands. Su pointed to $20-plus in EPS over the company’s strategic time frame as the long-term destination. If AMD gets there, the current multiple looks reasonable in hindsight. If it doesn’t, 46x forward EV/EBITDA leaves very little margin for error.

AMD has beaten revenue estimates in every quarter shown in TIKR’s earnings surprises data, including a 3.39% beat in Q1 2026 and a 6.20% beat in Q4 2025. The execution record supports the premium. The valuation multiples demand it continue.

See how Advanced Micro Devices performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $467.51

- Target Price (Mid): ~$1,742

- Potential Total Return: ~273%

- Annualized IRR: ~33%/year

See analysts’ growth forecasts and price targets for Advanced Micro Devices stock (It’s free!) >>>

TIKR’s mid-case model sets a 12/31/30 target of around $1,742, representing roughly 273% total upside and an annualized return of approximately 33% per year. The two primary revenue CAGR drivers are EPYC server CPU share gains inside AMD’s revised $120 billion-plus TAM, and the Instinct MI450 ramp delivering on contracted hyperscaler pipelines. The margin driver is mix shift: as the Data Center segment grows as a share of total revenue, profit margins expand toward approximately 35% net income margin by 2030.

The primary downside risk is execution-specific: a Helios ramp delay, further China export control restrictions on AI chips, or a pullback in hyperscaler AI capital expenditure would pressure the 2026 and 2027 estimates, on which the current multiple depends. At 46x forward EBITDA, estimate cuts move the stock hard before the business recovers.

Conclusion

Goldman and Bernstein raised their targets because the Q1 transcript showed a structural shift, not just a strong quarter. Lisa Su’s CPU-to-GPU ratio comments, if they continue materializing in customer orders through Q2 and Q3, are the data point that either validates every aggressive price target on the Street or exposes them.

The specific catalyst to watch is AMD’s Q2 2026 earnings, expected in early August. The threshold is clear: server CPU revenue needs to hit the guided above-70% year-over-year growth, and Helios commentary needs to confirm the Q4 production ramp is on schedule. Those two data points will tell investors whether Goldman and Bernstein got this right.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Advanced Micro Devices?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Advanced Micro Devices, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Advanced Micro Devices alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Advanced Micro Devices on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!