Key Stats for Carnival Corporation Stock

- 52-Week Range: $22 to $34

- Current Price: $26

- Street Mean Target: $34

- Street High Target: $45

- Analyst Consensus: 15 Buys / 5 Outperforms / 5 Holds

- TIKR Model Target (November 2030): $50

Carnival Beats Q1 Estimates and Introduces a $2.5 Billion Buyback. The Stock Hasn’t Noticed

Carnival Corporation (CCL), the world’s largest cruise operator, reported record first-quarter revenues of around $6.2 billion in its fiscal Q1 2026 earnings release on March 27, beating the Street estimate of around $6.1 billion.

Net income of around $275 million was more than 55% higher than the prior year.

Adjusted EPS came in at $0.20, beating the Street estimate of $0.18.

Free cash flow for the quarter reached around $700 million, more than doubling year-over-year.

Customer deposits hit a new first-quarter record of nearly $8 billion — surpassing last year’s high watermark by nearly 10%.

With nearly 85% of 2026 already on the books at historically high prices and less inventory available than this time last year, management raised its full-year EBITDA outlook to around $7 billion.

That $7 billion EBITDA target stands even after absorbing a $500 million fuel headwind from the Middle East conflict — and it was alongside that full-year guidance that CEO Josh Weinstein introduced PROPEL, the company’s new multi-year capital return framework targeting more than $14 billion in shareholder distributions through 2029, beginning with a $2.5 billion buyback authorization.

“These PROPEL targets will not come at the expense of financial strength, corporate responsibility or investing in our future,” Weinstein said on the Q1 2026 earnings call.

Three weeks after earnings, Carnival Corporation also completed its long-planned redomiciliation to Bermuda and unified its dual-listed structure, with Carnival plc becoming a UK subsidiary and the CCL ticker continuing on the NYSE — a structural simplification the company said would improve governance, reduce administrative costs, and lift US index weighting.

The Supreme Court meanwhile handed Carnival a procedural setback in the Havana Docks litigation, reinstating a combined $440 million judgment across four cruise operators — though Carnival noted that several of its key legal arguments remain unresolved and that the case will continue.

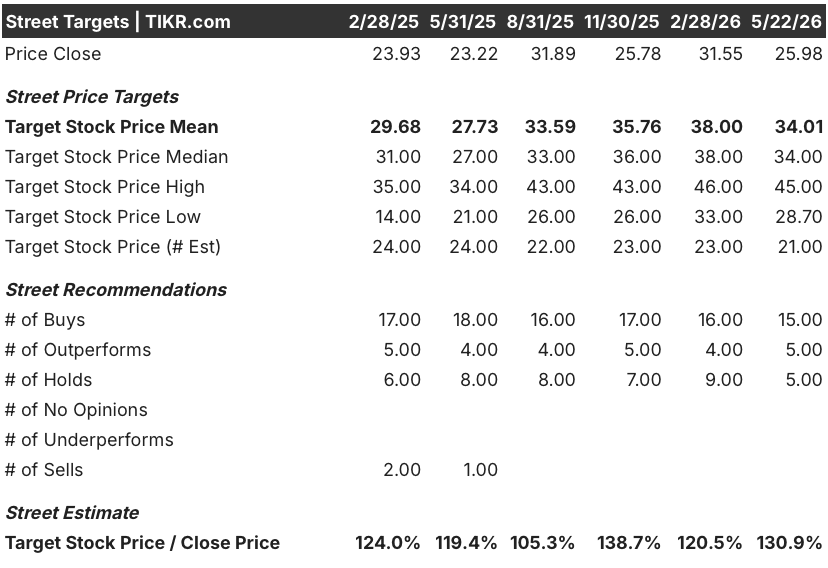

Analysts Back CCL Stock at $34 Mean Target. One Catalyst Changes the Math

The thesis on Carnival Corporation stock right now is a fuel-discounted recovery play — a business delivering record operational results that the market is penalizing for a cost headwind the company has already quantified and partially offset through consumption savings.

Fifteen analysts rate CCL a Buy, five rate it Outperform, and five rate it a Hold, with no Underperforms or Sells in the current consensus.

The Street mean target sits at around $34 against a current price of around $26, implying around 31% upside, with the high target reaching around $45.

For fiscal Q2 2026, analysts project revenue of around $7 billion, reflecting around 6% growth year-over-year, with full-year revenue estimates tracking toward around $27 billion.

Free cash flow estimates for Q2 2026 reach around $2 billion — an 18% jump year-over-year — before moderating in the back half as the company’s non-newbuild capital spending of around $2.4 billion flows through.

EBITDA consensus for Q2 2026 stands at around $3 billion, broadly flat year-over-year given the fuel headwinds the company already disclosed.

The one variable that would re-rate this stock quickly is fuel: Carnival’s guidance assumes Brent crude averaging $85 per barrel in Q3 and $80 in Q4, and management noted that a 10% change in fuel cost per metric ton for the remainder of the year moves the bottom line by around $160 million.

CCL is undervalued at around $26. Fifteen buy ratings and a Street mean of around $34 already reflect a fuel-adjusted view — and the TIKR model, which targets around $50 by November 2030, implies the Street’s consensus is still undershooting the long-term earnings path.

Is Carnival Corporation Stock Undervalued? TIKR’s $50 Model Target Says Yes

TIKR’s base case values Carnival Corporation at around $67 by November 2034, implying around 159% total return from the current price of around $26, or roughly 12% annualized — with the mid-case realized at November 2030 showing around $50 and around a 91% total return.

The model’s assumptions are conservative by design: mid-case revenue growth of around 3% annually from 2025 to 2035, net income margins expanding toward around 13%, and EPS growth compounding at around 8% per year.

If demand holds at current booking levels, the company’s near-full book position for 2026 at historically high prices converts to operating leverage that most cruise-sector models have not yet fully repriced.

The stock reaches around $55 in the low case — delivering around 9% annually — while the high case at around $80 implies around 14% per year, assuming revenue growth runs closer to around 3% and margin improvement tracks toward the high end of the model’s range.

The key tension is fuel. The mid-case does not assume a return to $60 oil — it assumes the company continues reducing consumption per unit while the macro environment normalizes.

Carnival’s own data supports that: management cited around $650 million in annual savings from consumption improvements since 2019, which more than offset the current fuel spike. If fuel remains structurally elevated, the mid-case holds — it just takes longer to get there. If fuel normalizes, the upside case becomes the likely outcome.

Is Carnival Stock a Buy Right Now?

Based on TIKR’s mid-case model, CCL is priced at a significant discount to its intrinsic value.

The stock trades at around $26, while TIKR’s base case targets around $50 by November 2030 — implying roughly 91% total return and around 12% annualized.

With 15 Buy ratings, a Street mean of around $34, and nearly 85% of 2026 already booked at historically high prices, the fundamental setup is constructive.

What Do Analysts Say About CCL Stock?

Twenty-five analysts currently cover CCL, with 15 rated Buy and 5 Outperform — 80% bullish with no Underperforms or Sells.

The Street mean target is around $34, implying around 31% upside from the current price of around $26, while the Street high sits at around $45.

TD Cowen recently moved CCL to a Top Pick and raised its target, while Truist maintained a Hold following the Supreme Court Helms-Burton ruling.

Should You Invest in Carnival Corporation Ltd.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Carnival Corporation stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Carnival Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze CCL stock on TIKR for Free →