Key Stats for Celsius Stock

- 52-Week Range: $28 to $67

- Current Price: $30

- Street Mean Target: $62

- Street High Target: $85

- Analyst Consensus: 12 Buys / 6 Outperforms / 4 Holds / 0 Underperforms / 0 Sells

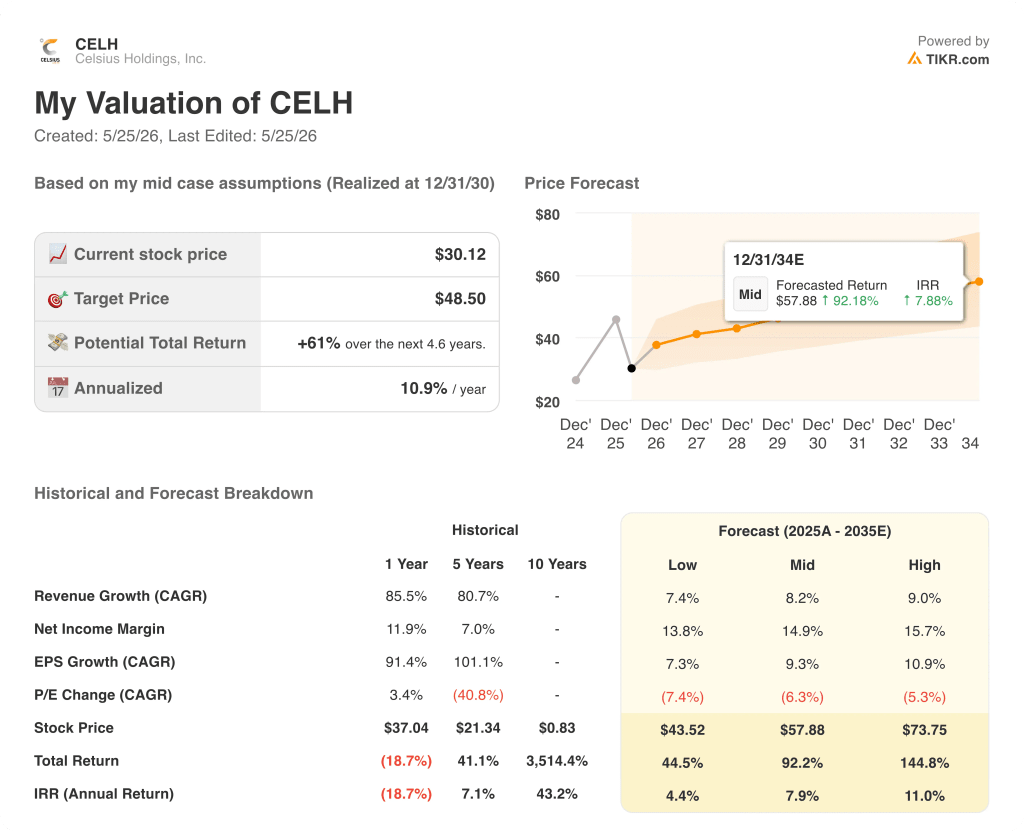

- TIKR Model Target (December 2030): $49

Celsius Holdings Beat the Street by 40% on EPS While the Stock Sat Near a 52-Week Low

Celsius Holdings (CELH), the functional beverage company behind the CELSIUS, Alani Nu, and Rockstar Energy brands, reported record Q1 revenue of approximately $782.6 million after its May 7 earnings, up 138% year over year, beating analyst estimates of roughly $766 million on the strength of its first fully consolidated quarter across all three brands.

The headline number is acquisition-inflated — Alani Nu and Rockstar together contributed over approximately $434 million — but that framing misses the point.

Alani Nu delivered approximately $368 million in net sales, representing roughly 60% pro forma growth year over year, with tracked-channel scanner data showing 85% growth on a clean comparable basis once the Cherry Bomb sell-in timing is stripped out.

Brand CELSIUS, under pressure from SKU rationalization and limited Q1 innovation, posted approximately $348 million in net sales, up roughly 6% year over year — the softest quarter in recent memory, but one management explained with specificity: slower-moving SKUs were deliberately pulled from shelves before faster-moving velocity SKUs had fully replaced them.

The company’s combined portfolio reached approximately 21% dollar share of the U.S. energy drink category in the four weeks ending April 12, according to CEO John Fieldly on the Q1 earnings call, crossing the threshold of one in every five energy drinks purchased in America.

Adjusted EBITDA reached approximately $195.5 million — a roughly $125 million increase versus the prior year quarter — with adjusted EBITDA margins expanding to 24.9% from 21.2%, roughly 370 basis points of improvement year over year.

The company repurchased approximately 700,000 shares for around $24.1 million in Q1, with approximately $236.1 million remaining under its $300 million buyback authorization, and CFO Jarrod Langhans confirmed on the call that repurchases have continued into Q2.

CFO Jarrod Langhans also stated on the Q1 earnings call that “the integration-related cost headwinds we discussed in Q4 have largely rolled off, which gives us a cleaner foundation entering the year.”

The stock fell roughly 11% in the days following the beat — not because the quarter was weak, but because gross margin at 48.3% came in below the low-50s target management had been guiding toward, and aluminum costs spiked through March and into Q2.

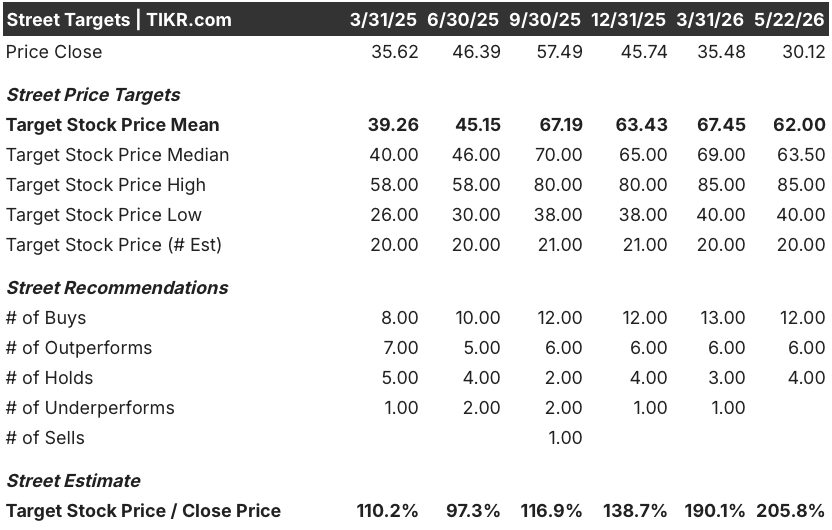

18 Analysts Rate CELH a Buy While the Stock Trades at Less Than Half the Street High Target

The thesis for Celsius stock is not complicated: 18 of 22 analysts covering the stock rate it Buy or Outperform, with a mean price target of around $62 — roughly 106% above the current price of $30.

That is not a mild disagreement between the stock price and analyst consensus; it is one of the widest gaps in the consumer staples space.

The street high target sits at around $85, and even the most cautious analyst has a target of around $40 — still 33% above where the stock trades today.

Wall Street’s conviction is built on two forward arguments: continued distribution ramp for Alani Nu through PepsiCo’s convenience network, where the brand remains significantly underpenetrated, and a margin recovery path back to the low 50s that management has now framed with specific operational milestones.

Consensus estimates project revenue of roughly $900 million in Q2 2026 — a 21% year-over-year increase — with the growth rate moderating as the acquisition anniversaries begin to lap, settling toward roughly 20% for the full year before stepping down into the low double digits in 2027.

EBITDA estimates show a roughly flat Q2 before stepping up through the back half of the year as the second manufacturing line at Big Beverages comes online in July and freight and raw material costs benefit from the orbit model improvements management described.

The analyst cuts following the quarter — Morgan Stanley lowering its target from around $64 to around $55 while maintaining Overweight — reflect the aluminum and freight headwind, not a change in the underlying thesis.

Four analysts hold the stock, and none rate it Underperform or Sell, which means there is no institutional short case built into the current rating distribution.

The specific variable the street is watching: gross margin trajectory in Q3 and Q4, where management has guided a sequential step-up after a Q2 “sidestep” that keeps margins roughly in line with Q1’s 48.3%.

With 18 Buy and Outperform ratings against a stock trading at roughly half its mean target, Celsius stock looks materially undervalued — provided the margin recovery arrives on the schedule management has laid out.

Is Celsius Stock Undervalued in 2026? TIKR’s $49 Target Says Yes — With a Condition

TIKR’s base case values Celsius stock at approximately $49 by December 2030, implying around 61% total return from the current price of $30, or roughly 10.9% annualized over 4 and a half years.

The mid-case assumes a revenue CAGR of roughly 8% through 2035 and net income margins expanding toward approximately 15%, figures that require Alani Nu to sustain its distribution momentum through convenience, CELSIUS to rebuild velocity after SKU rationalization, and the margin recovery to the low 50s to arrive substantially in 2027 rather than slipping further.

If Alani Nu’s velocity holds as it expands into convenience — where dollars per TDP increased 13% from January through April despite rapid ACV gains — and the orbit model delivers the freight savings management has outlined, Celsius Holdings stock reaches approximately $58 by December 2034, delivering around 7.9% annualized on the mid-to-long horizon.

The low case, assuming a revenue CAGR of roughly 7% and net income margins of approximately 14%, prices the stock at around $44 — still roughly 44% above today’s price — and reflects a scenario where aluminum and resin costs remain elevated for the full year, slowing but not derailing the margin recovery.

The bull case rests on one underappreciated variable: Alani Nu’s convenience channel is less than one year into a PepsiCo distribution ramp that typically takes two to three years to fully penetrate. A brand growing velocity as it expands TDPs — which Alani was doing through April — is a rare signal. At around $74 in the high case, the IRR reaches approximately 11% annualized, a return profile that carries meaningful risk premium given the commodity exposure but a credible ceiling if the macro cooperates.

The risk the model cannot resolve is aluminum. Elevated LME and Midwest premium costs are not company-specific; every aluminum-packaging business carries this exposure. But Celsius is absorbing that cost across three brands simultaneously at a moment when its margin structure is already compressed by integration overhead — meaning the buffer that existed at peak margin is thinner than it appears. A sustained commodity spike into 2027 delays the low-50s gross margin target, compresses EPS estimates, and gives the stock less room to re-rate.

Is Celsius Holdings Stock a Good Investment Right Now?

TIKR’s base case puts Celsius Holdings stock at approximately $49 by December 2030, implying around 61% upside from $30, or roughly 11% annualized.

With 18 of 22 analysts rating it Buy or Outperform and a mean target of around $62, the institutional view supports that direction.

The key variable is gross margin: if the orbit model and raw material normalization deliver the guided step-up in Q3 and Q4, the thesis holds cleanly. If aluminum stays elevated through year-end, the timeline shifts but the destination does not.

What Is the Price Target for Celsius Stock?

The mean street target is around $62, with 20 analyst estimates ranging from around $40 at the low end to around $85 at the high.

TIKR’s base case mid-point is approximately $49 by December 2030.

The spread between the street mean and the TIKR target reflects different time horizons — Wall Street is pricing a 12-month recovery; TIKR’s model prices a multi-year compounding thesis.

Should You Invest in Celsius Holdings?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Celsius stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Celsius Holdings alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze CELH stock on TIKR for Free →