Key Stats for GWW Stock

- Year-to-Date Performance: 7%

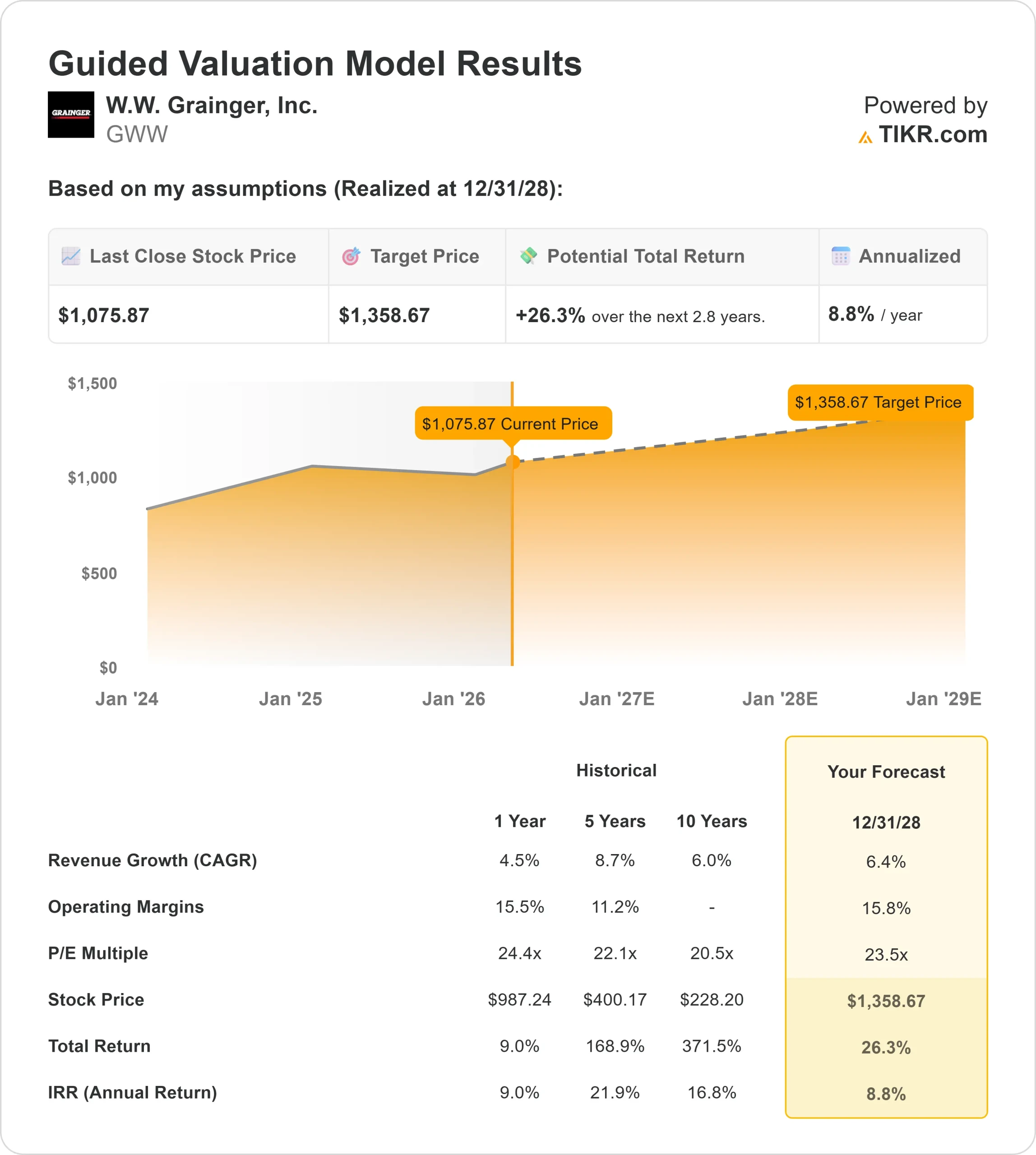

- 52-Week Range: $894 to $1,219

- Valuation Model Target Price: $1,359

- Implied Upside: 26%

Analyze your favorite stocks like W.W. Grainger with TIKR (It’s free) >>>

What Happened?

W.W. Grainger, Inc. stock is up about 7% year to date, recently trading near $1,076 per share as investors have increasingly rotated into high-quality industrial companies with stable earnings and strong pricing power amid a more uncertain macro backdrop.

That shift has supported steady demand for shares, particularly for companies that can deliver consistent results even as industrial activity remains uneven.

The stock is up mainly because Grainger is delivering steady revenue growth and strong margins, which are holding up well relative to industrial peers, supported by resilient demand in its maintenance, repair, and operations distribution business and faster growth in its Endless Assortment online platforms like Zoro and MonotaRO.

This combination has allowed the company to compete effectively against peers such as Fastenal and MSC Industrial, which operate similar distribution models, while benefiting from digital growth and pricing discipline.

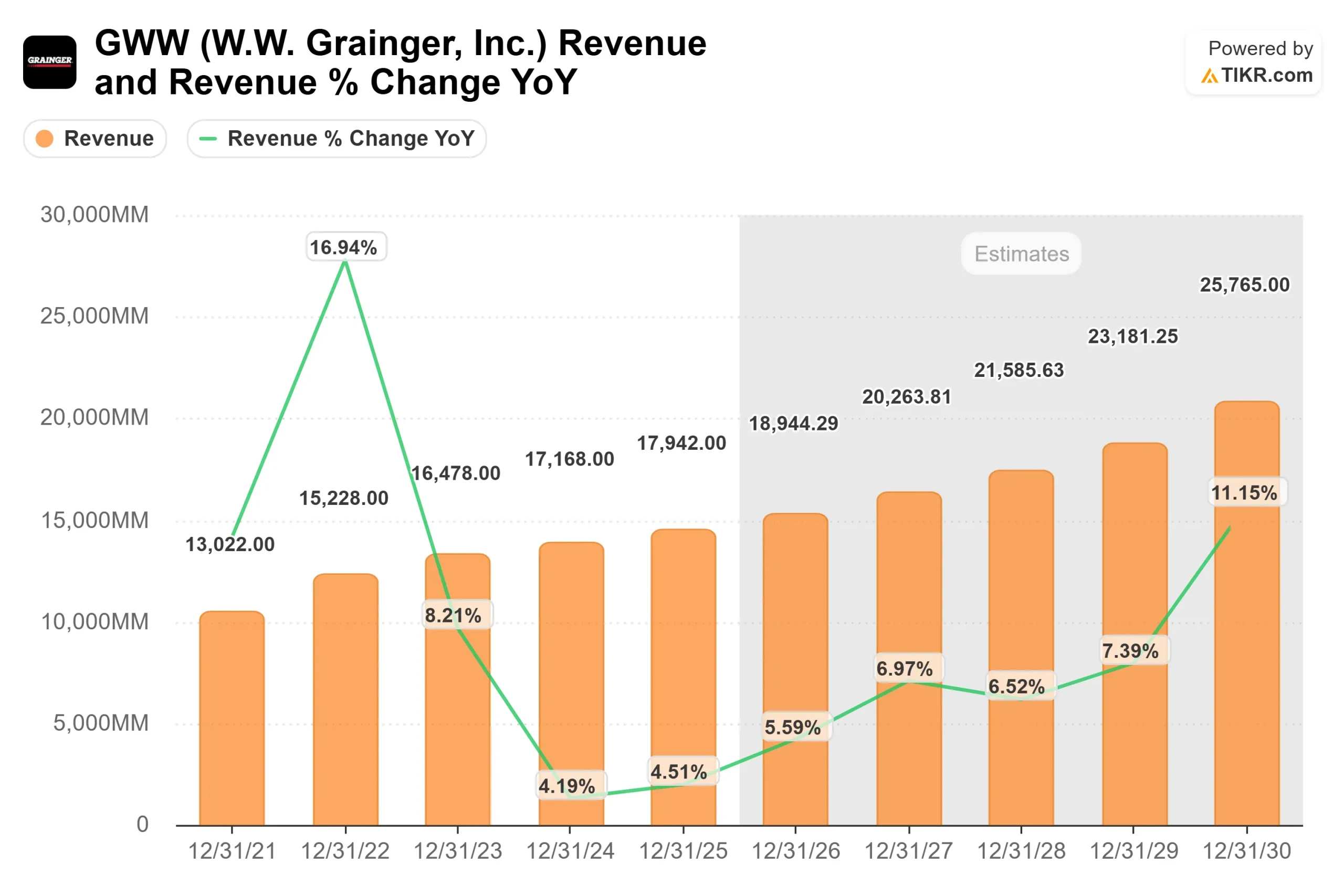

In 2025, Grainger generated $17.9 billion in revenue, with Endless Assortment sales rising 16%, highlighting how these drivers continue to support earnings expansion.

Recently, sentiment has also been supported by reaffirmed 2026 guidance, with management expecting revenue of $18.7 billion to $19.1 billion, organic sales growth of 6.5% to 9%, and EPS of $42.25 to $44.75, up about 10% at the midpoint.

CFO Deidra Merriwether said the company is “well within the range that we provided” for first-quarter growth, while also highlighting expected margin expansion of 40 to 90 basis points driven by pricing actions, supply chain efficiency, and the exit of the lower-margin U.K. business.

Analyst and institutional activity has added to the momentum and reinforced the stock’s move higher. Barclays raised its price target to $1,047 while maintaining an underweight rating, pointing to valuation concerns, while Oppenheimer set a higher target at $1,300 and the broader analyst average sits around $1,080, reflecting divergence in views.

Institutional positioning has remained active, with the California Public Employees Retirement System increasing its stake by 34.9% to about $129 million, Ossiam boosting its position by over 440% to roughly $17 million, and new positions from firms like FORA Capital and Magnetar Financial, while Hudson Bay Capital and Swiss Life Asset Management reduced exposure, signaling a balanced but still engaged investor base with total institutional ownership near 81%.

Value W.W. Grainger instantly (Free with TIKR) >>>

Is GWW Undervalued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth (CAGR): 6.4%

- Operating Margins: 15.8%

- Exit P/E Multiple: 23.5x

Revenue growth remains supported by Grainger’s role as a critical supplier of maintenance, repair, and operations products, which creates recurring demand across industrial, commercial, and government customers.

See analysts’ growth forecasts and price targets for W.W. Grainger (It’s free) >>>

Margins are expected to stay elevated due to a favorable mix shift toward higher-margin digital channels such as Zoro and MonotaRO, alongside continued pricing discipline and supply chain efficiency.

This reflects Grainger’s ability to sustain higher margins through pricing discipline and a growing mix of more efficient digital sales.

Based on these inputs, the model estimates a target price of $1,359, implying about 26% total upside over roughly 3 years, indicating the stock appears undervalued at current prices.

Expansion of the Endless Assortment segment continues to increase product breadth and capture incremental share in the fragmented small business market.

Digital penetration is improving customer retention and order frequency, reinforcing long-term revenue visibility and margin expansion.

Pricing actions and supplier relationships are helping offset cost pressures, including tariffs, while supporting gross margin recovery.

High returns on invested capital above 30% enable efficient reinvestment while still supporting consistent shareholder returns.

Execution in 2026 will depend on maintaining mid-single-digit growth and delivering incremental margin expansion as guided.

At current levels, Grainger appears undervalued, with future performance driven by digital growth, margin durability, and continued share gains across a fragmented industrial distribution market.

How Much Upside Does GWW Stock Have From Here?

Investors can estimate W.W. Grainger potential share price, or what any stock could be worth, in under a minute using TIKR’s New Valuation Model tool.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

Value W.W. Grainger in under 60 seconds with TIKR (It’s free) >>>