Key Stats for Generac Stock

- 52-Week Range: $109 to $241

- Current Price: $220

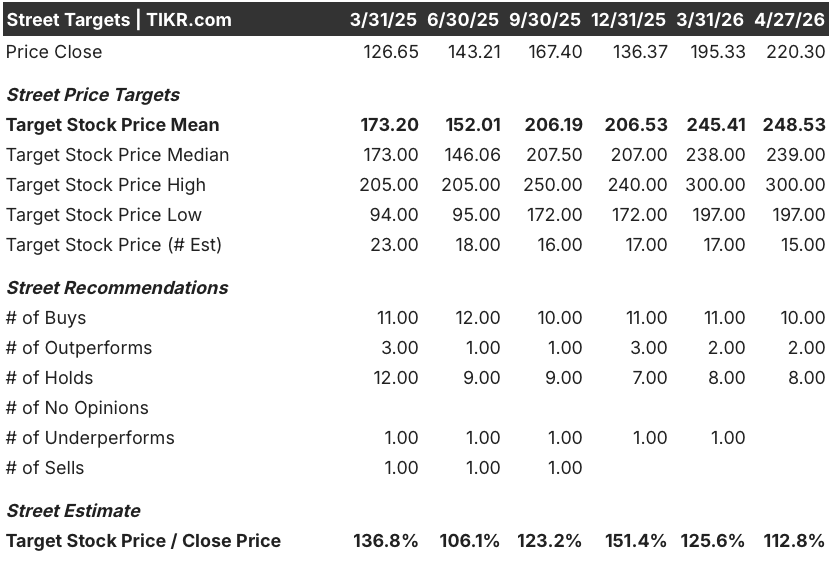

- Street Mean Target: $249

- Street High Target: $300

- Analyst Consensus: Buy

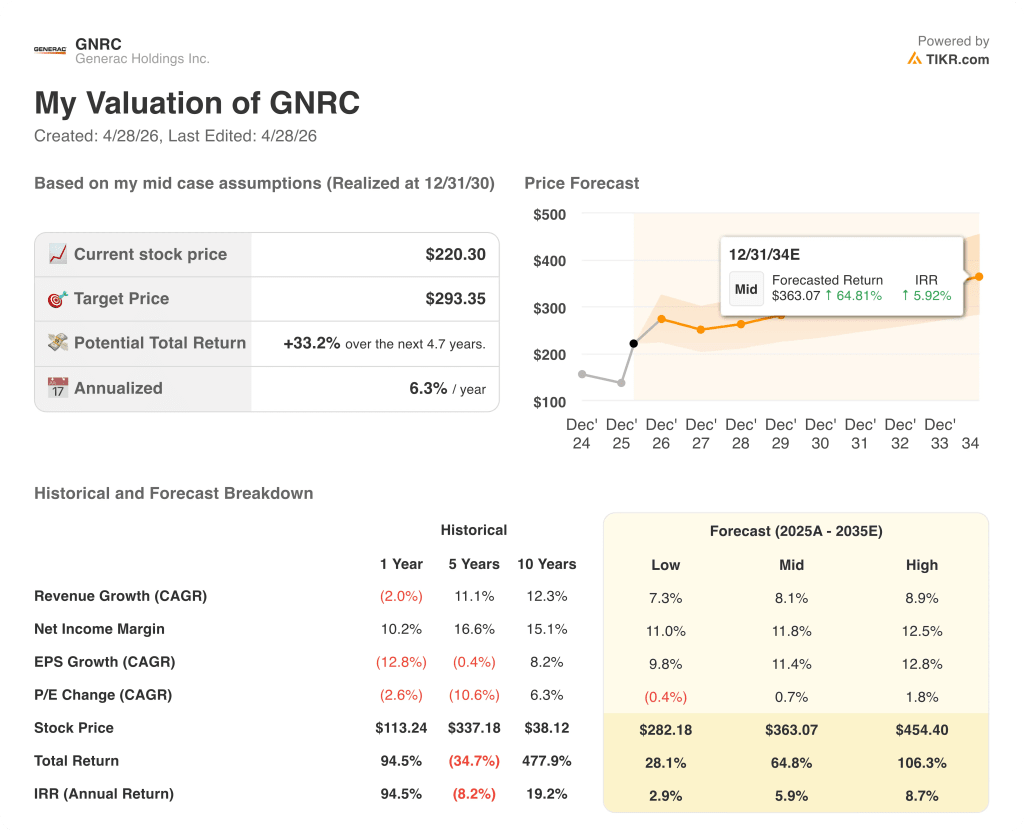

- TIKR Model Target (Dec. 2030): $293

What Happened?

Generac Holdings (GNRC), which manufactures backup power generators and energy technology systems for residential and commercial customers, sits at a structural turning point as demand from data center operators begins to redefine the company’s long-term earnings profile.

The catalyst was Q4 2025 earnings, reported February 11, where residential product sales fell 23% to $571.87 million due to historically low power outage activity, but commercial and industrial product sales rose 10% to $400 million on growing data center revenue.

The C&I division’s $400 million backlog at the time of reporting — built without any material hyperscaler purchase orders — validated that Generac’s newly launched large megawatt diesel generators had found real commercial traction with co-location customers ahead of any formal supply agreements.

CEO Aaron Jagdfeld stated on the Q4 2025 earnings call that “momentum in the data center end market has further accelerated,” and that the company had “progressed to the pilot phases” with two specific hyperscale customers preparing for potential significant volume in 2027 and 2028.

On March 25, Generac’s Investor Day revealed the backlog had grown to $700 million and that one hyperscaler had issued a nonbinding notice to proceed for over $600 million of product, with the company targeting domestic manufacturing capacity above $1 billion by year-end.

The company simultaneously reorganized its segments into Residential and Commercial and Industrial, effective March 31, a structural realignment designed to surface the C&I growth story more explicitly and reduce the earnings volatility driven by residential outage cycles.

A 3-year financial framework presented at Investor Day projects consolidated revenue growing at a mid-teens compound annual rate, from $4.21 billion in 2025 to a range of $6.2 billion to $6.6 billion by 2028, with EBITDA margins expanding from 17% toward low-20% territory.

Wall Street’s Take on GNRC Stock

The Q4 miss was a distraction, and investors who focused on the headline revenue shortfall missed the more important signal: Generac’s C&I business was quietly building a backlog-driven earnings profile that the residential segment never had.

GNRC’s EBITDA is forecast to grow from $715.54 million in 2025 to around $890 million in 2026 (around 25% growth), then compound toward the $1.25 billion to $1.45 billion range by 2028 as data center volume scales behind a $700 million backlog and a potential $600 million-plus hyperscaler award not yet in guidance.

Twelve analysts carry buy or outperform ratings on Generac stock, with eight holds and no sells; the mean price target stands at $249, implying around 13% upside from current levels, with Wall Street watching whether hyperscaler purchase orders materialize from the current pilot programs in the first half of this year.

The bull-bear spread is wide enough to matter: the street high target of $300 anchors on full hyperscaler commercialization while the low of $197 reflects a scenario where residential demand stays soft and data center contract timing slips, leaving investors to watch Q1 2026 C&I revenue and any hyperscaler AVL announcement as the deciding data points.

If the residential recovery stalls because power outage activity remains below the 5-year baseline average in the second half of 2026, the margin expansion story loses its residential contribution and EBITDA guidance comes under pressure.

Generac reports Q1 2026 earnings before market open on April 29: watch C&I revenue for confirmation the $700 million backlog is converting, and whether management upgrades full-year guidance to reflect the nonbinding $600 million hyperscaler notice to proceed.

What Does the Valuation Model Say?

The TIKR model’s mid-case target of around $293 implies a total return of roughly 33% over approximately 5 years at a 6% annualized IRR, anchored on around 8% to 9% revenue CAGR through 2030 and net income margins recovering from 9% in 2025 toward the high-11% range by 2028 as C&I operating leverage kicks in.

At the TIKR model’s target price, Generac stock appears fairly valued given the 33% total return is real but unremarkable unless the hyperscaler awards arrive ahead of the model’s conservative placeholder assumptions.

The central tension in the Generac investment case is a timing question: the data center opportunity is confirmed, the backlog is growing, but the hyperscaler purchase orders that would transform the earnings trajectory are still pending formal AVL approval and supply agreement execution.

What Has to Go Right

- Generac receives approved vendor list status from at least one of the two hyperscalers currently in pilot programs, converting the nonbinding $600 million notice to proceed into firm purchase orders before year-end

- The Sussex, Wisconsin facility reaches full run-rate capacity in Q3, ahead of the original Q4 target, giving the company incremental 2026 delivery flexibility

- C&I revenue grows at the guided 30%-plus rate in 2026, driven by the $700 million backlog that is majority weighted toward 2026 shipments

- Residential demand stabilizes in the second half as outage activity returns toward the 5-year baseline, contributing mid-teens growth in home standby and restoring the segment’s 22.5% EBITDA margins from the 2025 weather-suppressed level

- The Enercon Engineering acquisition, expected to close in Q2, adds over 100 basis points of C&I segment margin through packaging cost internalization

What Could Go Wrong

- AVL qualification delays push the $600 million hyperscaler notice to proceed into 2027 or later, leaving full-year 2026 C&I revenue dependent entirely on co-locators and traditional channels at a lower run rate than guidance requires

- A second consecutive soft outage year in 2026 again suppresses home standby demand, forcing a residential guidance cut that offsets C&I strength at the consolidated EBITDA line

- Alternator supply constraints, flagged by management at Investor Day as the most acute near-term bottleneck, limit the rate at which Generac can ramp large megawatt production even with capacity available

- The legal settlement provision that reduced 2025 net income by $104.5 million signals broader liability exposure in the portable generator product category that could recur

- The residential energy technology segment (solar storage, ecobee, PowerMicro) remains below EBITDA breakeven in 2026, absorbing operating expense that management is not prepared to cut if market conditions deteriorate further

Should You Invest in Generac Holdings Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up GNRC stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Generac Holdings Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze GNRC stock on TIKR for Free →