Key Stats for GE Aerospace Stock

- 52-Week Range: $176 to $348.5

- Current Price: $311.9

- Street Mean Target: $352.8

- Street High Target: $425

- TIKR Model Target (Dec. 2030): $536.6

What Happened?

GE Aerospace (GE), the world’s largest commercial jet engine maker, delivered a breakout 2025 that resets the earnings bar heading into what management is calling the company’s strongest setup since its 2023 spin from the legacy GE conglomerate.

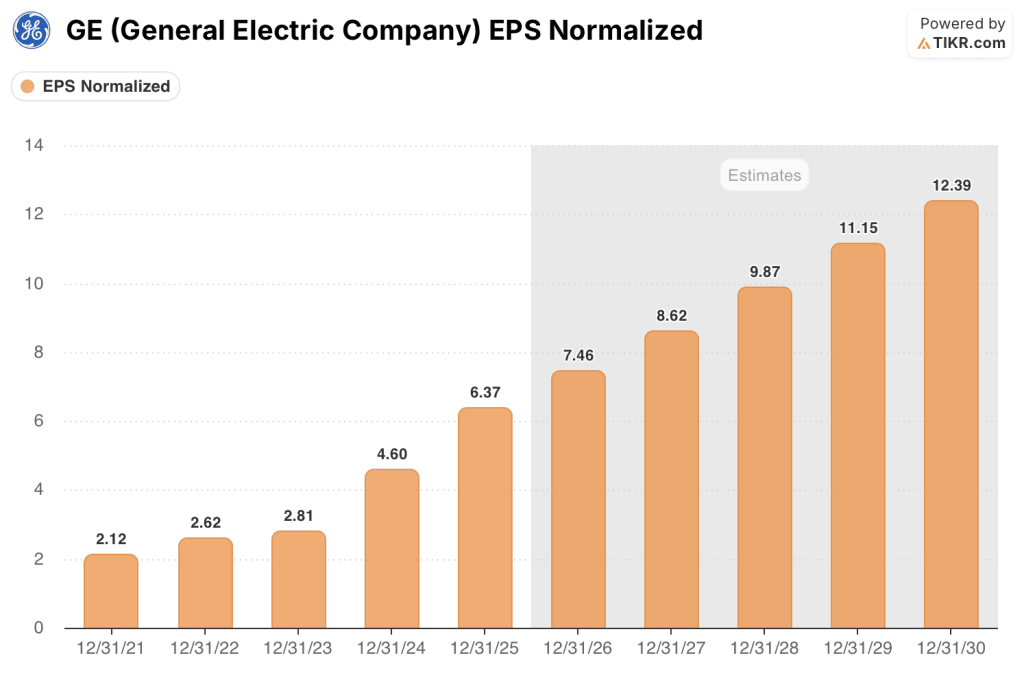

The fourth quarter was the exclamation point: adjusted EPS of $1.57 beat the $1.43 consensus estimate, and full-year normalized EPS of $6.37 surged 38.5% year over year, well ahead of guidance.

The engine driving that beat is GE’s aftermarket services business, which generates revenue by repairing and overhauling the jet engines already flying on commercial aircraft — a captive, recurring revenue stream tied directly to flight hours and fleet age.

LEAP engine deliveries (the next-generation narrowbody platform that powers Boeing 737 MAX and Airbus A320neo jets, replacing the older CFM56) hit a record 1,800-plus units in 2025, up 28%, while internal LEAP shop visit volume grew 27%, fueling a 26% rise in commercial services revenue.

On March 9, GE committed an additional $1 billion in U.S. manufacturing investment for 2026, a second consecutive year at that level, targeting 5,000 new jobs and expanded capacity for both the CFM LEAP engine and defense platforms.

Larry Culp, Chairman and CEO, stated on the Q4 2025 earnings call that “we expect to deliver mid-teens revenue growth between ’24 and ’26 compounded and $10 billion of profit in ’26, 2 years earlier than our outlook at spin,” anchoring management’s conviction to the $190 billion backlog built across commercial and defense customers.

GE Aerospace stock enters 2026 with 2026 operating profit guidance of $9.85 billion to $10.25 billion, EPS guidance of $7.10 to $7.40 (up nearly 15% at the midpoint), and free cash flow of $8 billion to $8.4 billion, all supported by a LEAP installed base management expects to roughly triple between 2024 and 2030.

Wall Street’s Take on GE Stock

The 2025 results close a chapter that began with GE’s restructuring and open one defined by a single compounding mechanism: an 80,000-engine installed base that generates decades of locked-in services revenue, with the faster-growing LEAP fleet still in the early innings of its aftermarket cycle.

GE Aerospace’s normalized EPS reached $6.37 in 2025, up 38.5%, and the Street expects it to compound at 17.1% to $7.46 in 2026 and 15.5% to $8.62 in 2027, driven by the $3.5 billion in incremental services revenue CFO Rahul Ghai cited on the earnings call as the primary 2026 growth engine, alongside continued LEAP equipment growth and defense deliveries up 30% in 2025.

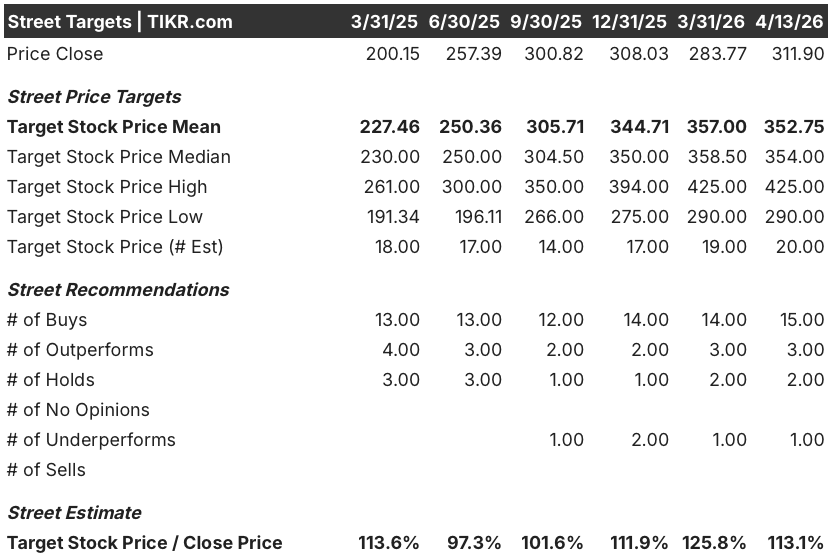

Eighteen of 20 analysts covering GE Aerospace stock rate it a buy or outperform, with a mean price target of $352.75, implying 13.1% upside from the current $311.90 price; analysts are specifically waiting on the pace of LEAP shop visit acceleration and CFM56 retirement trends, which management guided to remain in the 2,300-to-2,400 range through 2028 versus prior expectations of 2,300.

The spread between the $290 low target and $425 high target reflects a genuine valuation debate: bears argue that GE Aerospace stock already commands a premium industrial multiple that leaves little room for error if aftermarket pricing softens, while bulls point to the LEAP installed base tripling through 2030 as a structural revenue driver no current multiple can fully price.

Priced at roughly 41.8x 2026 consensus EPS of $7.46, GE Aerospace stock sits above the historical industrial peer average, yet EPS is compounding at 15%-plus annually through at least 2028 against a $190 billion backlog with over 100% free cash flow conversion, leaving GE Aerospace stock appearing undervalued relative to the multi-year earnings power the backlog guarantees.

When asked on the earnings call whether the company could outperform its mid-teens services guidance, Culp responded that there was “nothing here at the beginning of the year that gives us pause relative to the tailwinds,” directly signaling to the market that the conservative 2026 guide has room to prove too low.

A deterioration in commercial air travel demand, whether from geopolitical disruption (jet fuel prices have already spiked following Middle East conflict) or a global demand slowdown, would compress shop visit volume and break the aftermarket compounding thesis.

The number to watch at Q1 2026 earnings is LEAP internal shop visit growth against management’s 25% full-year target and commercial services revenue growth against the mid-teens guide.

GE Aerospace Financials

GE Aerospace’s total revenues grew 18.5% to $45.9 billion in 2025, the second consecutive year of accelerating growth after a 9.5% gain in 2024, as services volume and higher equipment deliveries compounded across both commercial and defense segments.

The operating leverage is unambiguous: operating income rose 22.3% to $9.5 billion in 2025, outpacing revenue growth for the third straight year, as the higher-margin services mix and FLIGHT DECK productivity improvements (GE’s Lean manufacturing system borrowed from Japanese industrial methods) expanded operating margins to 20.7%, up from 20.0% in 2024.

Gross profit grew 20.4% to $14.4 billion, lifting gross margins to 31.5% from 31.0%, a four-year high that reflects the cumulative shift in revenue mix toward services, where engine repair and overhaul commands structurally higher margins than new equipment sales.

What Does the Valuation Model Say?

The TIKR model prices GE Aerospace at a mid-case target of $536.64, implying 72% total return from today’s $311.90 over roughly 4.7 years, built on an 8.0% revenue CAGR, 18.4% net income margins, and 11.3% EPS CAGR through 2030 — assumptions the $190 billion backlog and structural LEAP aftermarket ramp make conservative rather than optimistic.

GE Aerospace stock appears undervalued at current levels, with the mid-case scenario implying a 12.2% annualized return to 2030 even as EPS is already growing at 15%-plus annually heading into the period.

The TIKR model’s three scenarios map directly to one variable: how fast the LEAP aftermarket flywheel compounds relative to the GE9X losses and supply chain headwinds that pressure near-term margins.

Low Case ($582.67 | 7.4% IRR | 7.2% revenue CAGR | 17.3% net margins)

- LEAP shop visit growth decelerates below the 25% 2026 target as geopolitical disruption compresses air travel demand and jet fuel prices (already doubled in European markets since late February) keep airlines cautious on discretionary MRO spend

- GE9X losses double year over year in 2026 as guided, and a 777X certification delay beyond 2027 extends the headwind into 2028, capping CES margin recovery below the 26.6% level

- Rare earth shortages, specifically yttrium used in engine thermal barrier coatings, remain unresolved, periodically slowing both new engine deliveries and MRO throughput through 2027

- Revenue compounds at 7.2% annually, net income margins reach 17.3%, and the stock delivers 86.8% total return to 2030 but underperforms the mid-case by roughly $168 per share

Mid Case ($750.87 | 10.6% IRR | 8.0% revenue CAGR | 18.4% net margins)

- LEAP internal shop visits grow 25% in 2026 as guided, building on 27% growth in 2025, sustaining mid-teens commercial services revenue growth through 2028 as the installed base expands toward the tripling management targets by 2030

- CFM56 retirements hold at roughly 2% of fleet annually, keeping shop visits in the 2,300-to-2,400 range through 2028 and sustaining the high-margin CFM56 aftermarket as a durable earnings floor

- LEAP OE turns profitable in 2026 as guided, removing the equipment-margin drag and allowing CES margins to recover above current levels even as 9X shipment volumes grow

- Revenue compounds at 8.0%, net income margins reach 18.4%, and the stock delivers 140.7% total return to 2030, consistent with a 10.6% annualized IRR

High Case ($942.23 | 13.5% IRR | 8.8% revenue CAGR | 19.2% net margins)

- LEAP services revenue outperforms mid-teens guidance as widebody programs (GEnx, GE90) sustain elevated work scopes and the 300 GEnx engines ordered by United Airlines in February begin entering heavier maintenance cycles

- Defense delivers above the 30% growth rate from 2025, supported by the $21 billion DPT backlog, a $12.4 million U.S. Air Force GEK1500 engine contract awarded February 23, and accelerating NATO defense budgets driving incremental F414 and T700 demand

- FLIGHT DECK productivity improvements compound across the expanded MRO network, driving operating margin expansion well beyond 20.7% as automation investments in Singapore (up to $300 million through 2029) and the U.S. ($1 billion in 2026 alone) lift throughput without proportional cost growth

- Revenue compounds at 8.8%, net income margins reach 19.2%, and the stock delivers 202.1% total return to 2030, consistent with a 13.5% annualized IRR

Should You Invest in GE Aerospace?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up GE stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track GE Aerospace alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze GE stock on TIKR for Free →