Key Stats for Expedia Group Stock

- 52-Week Range: $160.00 – $303.80

- Current Price: $239.47

- Street Mean Target: around $286

- TIKR Mid-Case Model Target (2030): around $465

- Mid-Case Annualized IRR: around 16% per year

- Q1 2026 Revenue: $3.43 billion, up 15% year over year

- Q1 2026 Adjusted EBITDA Margin: 15.8%, highest Q1 in 15 years

What Happened at Expedia Group

The Q1 2026 results were hard to argue with, as Expedia’s (EXPE) Revenue grew 15% year over year to $3.43 billion, gross bookings rose 13% to $35.5 billion, and adjusted EBITDA came in at $542 million, up 83% from a year earlier.

Adjusted EBITDA margin hit 15.8%, the highest first-quarter level in 15 years, as adjusted EPS of $1.96 nearly quintupled from $0.40 a year prior. CEO Ariane Gorin called it the highest first-quarter profitability in the company’s history.

The driver behind most of that performance is B2B, Expedia’s business of selling travel inventory and technology to airlines, banks, and corporate travel managers who want to offer booking without building the infrastructure themselves.

B2B revenue grew 25% in the quarter to $1.18 billion, now representing roughly 35% of total revenue. New partnerships with Uber and Bank of Montreal’s AIR MILES program were among the additions. Expedia also announced the acquisition of CarTrawler, a B2B platform focused on car rental and ground transportation, expected to close in the second half of 2026.

Management also addressed the AI question directly on the earnings call. CEO Gorin described active booking integrations with both ChatGPT and Claude, framing AI assistants as distribution partners rather than disintermediators.

The logic holds in a B2B context: if a traveler books through an AI assistant and the underlying inventory comes from Expedia’s platform, Expedia still collects the economics. The B2B buildout is partly a hedge against exactly this scenario.

See analysts’ growth forecasts and price targets for Expedia stock (It’s free) >>>

What the Valuation Model Says

The disconnect between Expedia’s operating momentum and its stock price is clear in TIKR’s model.

At a current price of $239.47, the mid-case scenario targets around $465 by the end of 2030, implying a total return of roughly 94% and an annualized return of roughly 16%. That assumes revenue growth of around 6% annually, net income margins expanding toward 18%, and a P/E multiple that contracts modestly over time.

Even with that multiple headwind baked in, the model implies returns well above what most large-cap equities are priced to deliver today.

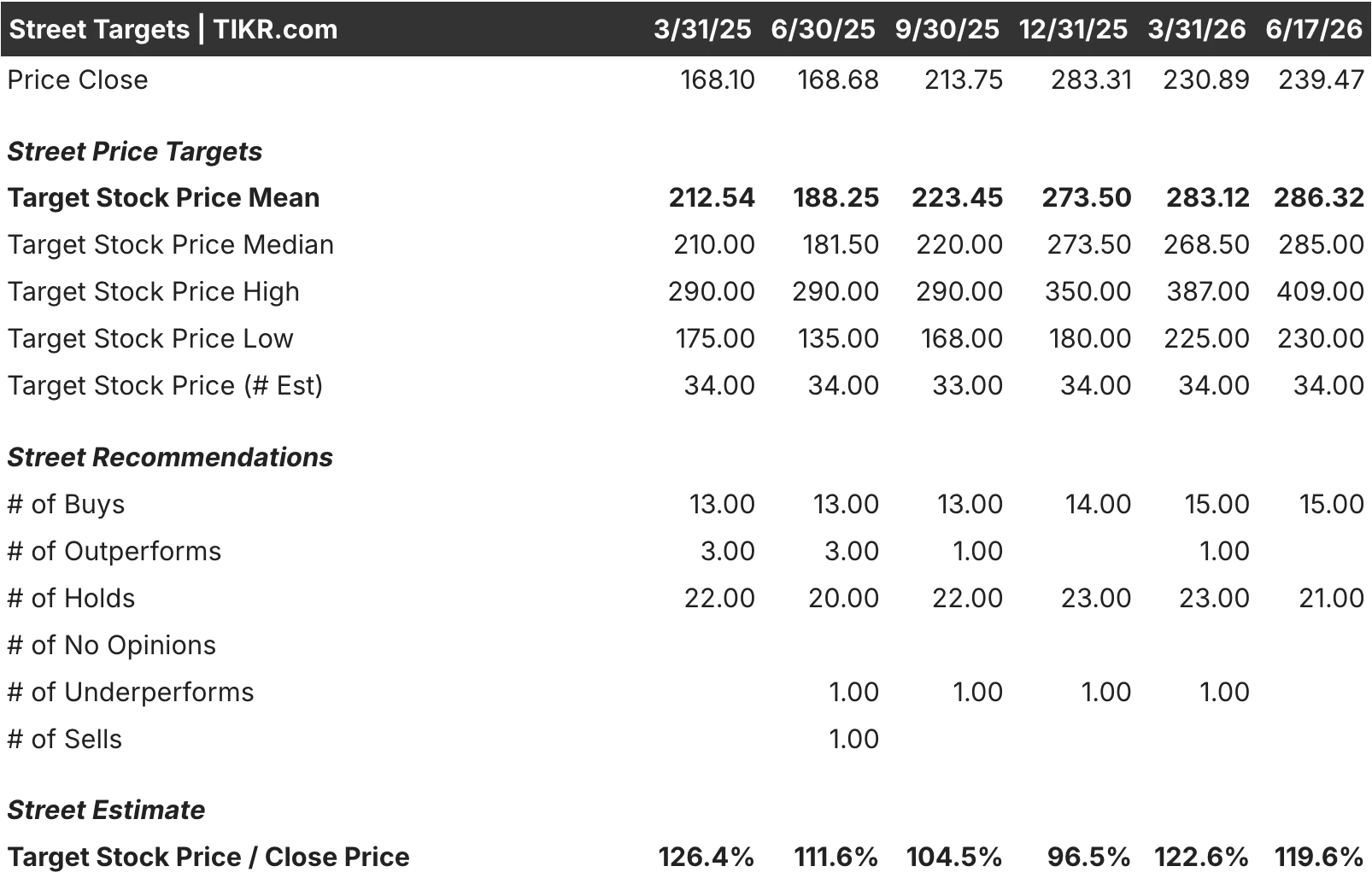

The Street lands at a more conservative mean target of around $286, implying about 20% upside from current levels. Of the 34 analysts TIKR tracks, 15 rate the stock a buy and 21 sit at hold, an unusually hold-heavy distribution for a company beating estimates and expanding margins.

That cautious majority reflects a specific concern: analysts are unsure what AI-native search means for the long-term volume of traffic flowing through consumer brands like Expedia and Hotels.com, and they are unwilling to pay full price for a business model facing a structural question that has yet to be answered.

The range of targets, from a low of $230 to a high of $409, reflects genuine analytical disagreement rather than noise.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in Expedia Group, Inc.

The bull case is that Expedia is executing at the highest margin level in years, the B2B business is growing fast and diversifying revenue away from consumer OTA traffic, and TIKR’s model prices in around 16% annualized returns at current levels, with the company also holding net cash and a new $5 billion buyback authorization.

The bear case is that the consumer OTA business, still roughly 62% of revenue, is structurally exposed to AI tools that could erode the direct traffic that drives its economics. If that erosion outpaces B2B’s ability to compensate, the margin expansion story stalls.

Expedia Group is not a distressed turnaround or a speculative bet. It is a profitable, cash-generative business trading at a meaningful discount to its own history and to peers like Booking Holdings, for a reason that matters.

Whether that reason will resolve in Expedia’s favor over the next few years is the question TIKR’s model asks investors to take a position on.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!