Key Takeaways for FedEx Stock

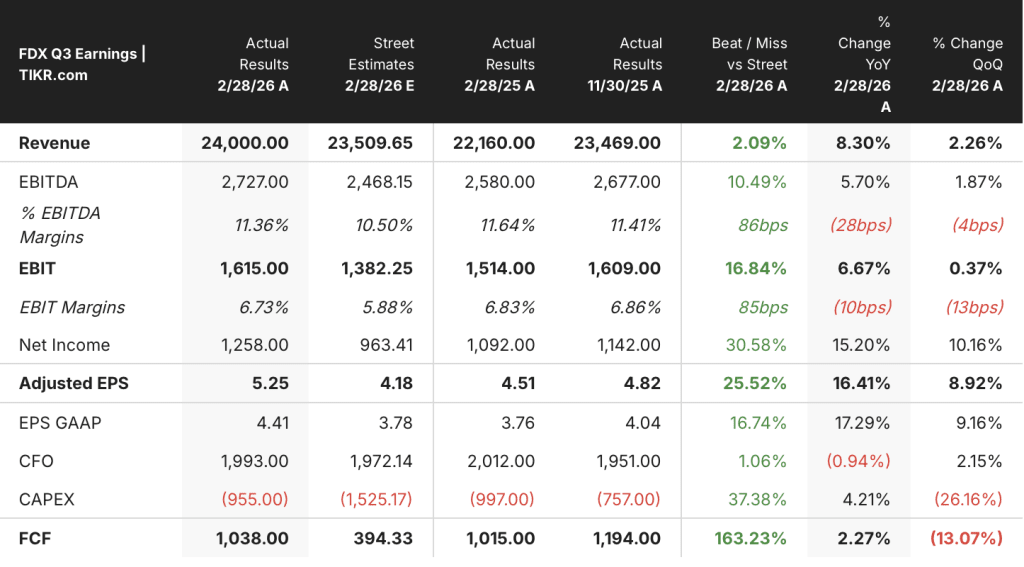

- FedEx grew Q3 revenue 8% year-over-year to $24.00 billion, the strongest quarterly growth rate in at least eight quarters.

- Operating income held at $1.67 billion for the second consecutive quarter while operating margins compressed to 7% despite the revenue acceleration.

- The Federal Express segment expanded adjusted operating margin by 50 basis points, marking its sixth consecutive quarter of margin expansion.

- TIKR’s model values FDX stock at approximately $370 by May 2030, implying around 13% total return from the current price.

FedEx Delivered Its Strongest Revenue Quarter in Years, but the Margin Story Cuts Both Ways

FedEx Corporation (FDX) posted its highest quarterly revenue growth rate in years following Q3 fiscal 2026 earnings, reporting $24 billion in revenue against a backdrop of B2B momentum and a record peak season.

The company operates one of the world’s largest logistics networks, moving packages and freight across more than 220 countries through its Federal Express air-and-ground system and, until June 1, its FedEx Freight less-than-truckload unit.

Revenue growth of 8% year-over-year came primarily from the Federal Express segment, which grew its own top line by 10%.

U.S. domestic package revenue grew 10% and international export package revenue grew 8%, both driven by yield improvement and volume gains.

CEO Raj Subramaniam called Q3 “our most profitable peak yet,” crediting improved demand forecasting, revenue quality discipline in B2B verticals, and early Network 2.0 efficiency gains.

The company now expects full-year adjusted earnings per diluted share of $19.30 to $20.10, raised from a prior range of $17.80 to $19.00.

The planned June 1 spin-off of FedEx Freight remains on track, and management described the separation as a catalyst to unlock meaningful long-term stockholder value.

FedEx Revenue Is Accelerating, but Operating Margin Has Not Followed

Revenue growth reached 8% year-over-year in the most recent quarter, the highest rate in the trailing eight-quarter window.

Gross profit came in at $6.29 billion, holding roughly flat with the prior-year period despite the accelerating top line.

Gross margins compressed to 26%, down from 31% in the same quarter a year earlier, signaling that cost growth has outrun the revenue lift at the gross level.

Operating income held at $1.67 billion for the second consecutive quarter, unchanged even as revenue climbed.

Operating margins landed at 7%, flat with the prior period and well below the 11% the business produced in the comparable quarter one year ago.

The gap is the thesis: FedEx is growing revenue at its fastest rate in years, and the income statement shows the cost structure has not yet responded to match it.

FedEx Trails DHL on Operating Margins While UPS Sits Even Further Behind

Deutsche Post AG (DHL) posted a 7% operating margin in the most recent quarter, edging above FedEx’s 7% result and above the 6% UPS delivered.

FedEx has held the middle position in this peer group for three consecutive quarters, trailing DHL while leading United Parcel Service (UPS) by a narrow margin.

The spread between DHL and FedEx is smaller than the article’s income statement suggests it should be: FedEx’s gross margin compression has not yet created a peer-level disadvantage on operating margins, which means the cost structure problem is partially absorbed rather than fully visible in the competitive comparison.

Is FedEx Stock Undervalued in 2026? TIKR’s $370 Model Puts a Condition on It

TIKR’s model values FedEx at approximately $370 by May 2030, implying around 13% total return from the current price of $326, or roughly 3% per year.

The condition the income statement attaches to that target is operating margin recovery.

Revenue is already there: the 8% growth rate in Q3 is the income statement proof that FedEx’s commercial strategy is gaining traction in high-margin B2B verticals.

What has not yet followed is the operating income expansion that Network 2.0’s $2 billion in cumulative savings is expected to deliver, and the TIKR target depends on that translation happening before the end of the decade.

Should You Invest in FedEx Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up FedEx Corporation stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track FedEx Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze FDX stock on TIKR for Free →

What did FedEx say about the Freight spin-off?

Management confirmed the June 1, 2026 spin-off of FedEx Freight remains on track and expects the separation to unlock meaningful long-term stockholder value by allowing the core Federal Express business to focus on higher-margin verticals.