Key Stats for Broadcom Stock

- Today’s Performance: 6%

- 52-Week Range: $244 to $495

- Valuation Model Target Price: $407

- Implied Upside: 8%

Analyze your favorite stocks like Broadcom Inc. with TIKR (It’s free) >>>

What Happened?

Broadcom Inc. stock rose about 6% today, recently trading near $409 per share as investors stepped back into one of the market’s most important AI infrastructure names after a sharp June pullback. The stock had been pressured after Broadcom’s AI chip guidance came in slightly below Wall Street’s elevated expectations, but buyers returned as the market refocused on the company’s custom AI chip demand, VMware software growth, and strong margins.

The stock moved higher today because JPMorgan’s bullish update helped investors view the recent selloff as too harsh compared with Broadcom’s actual AI growth outlook. JPMorgan kept an Overweight rating and a $580 price target, pointing to Broadcom’s custom AI chip position, advanced packaging strength, IP portfolio, execution record, and long-running Google TPU relationship. The update mattered because Broadcom had sold off after its Q3 AI chip outlook of $16 billion came in slightly below analyst expectations, even though its total Q3 revenue outlook of $29.4 billion remained strong.

On the Q2 call, Broadcom gave investors a stronger 2026 AI story, with total revenue reaching a record $22.2 billion, AI semiconductor revenue hitting a record $10.8 billion, up 143%, and AI bookings topping $30 billion during the quarter. CEO Hock Tan said, “Demand for XPUs and networking is simply insatiable,” as Broadcom guided for Q3 AI semiconductor revenue of $16 billion, up over 200%, and full-year 2026 AI semiconductor revenue of $56 billion. XPUs are custom AI accelerators built for large cloud customers, while TPUs are Google’s version of those chips, making Broadcom a key supplier behind the AI computing buildout.

Institutional updates added another layer to the story, though positioning was mixed. Gotham Asset Management raised its Broadcom stake by 3.8% to 333,654 shares worth about $116 million, while Element Capital Management opened a new position worth about $6 million and Evolve Private Wealth opened a new position worth about $20 million. Other firms trimmed exposure, but additions from Bamco and Clough Capital showed Broadcom remained a large institutional AI infrastructure holding. That matters because Broadcom is no longer just a chip stock, but a mix of custom AI accelerators, AI networking chips, and VMware infrastructure software, competing with Nvidia in AI chips, Marvell in custom silicon, AMD in accelerators, and Cisco in networking.

Value Broadcom Inc. instantly (Free with TIKR) >>>

Is Broadcom Fairly Valued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth (CAGR): around 30%

- Operating Margins: around 55%

- Exit P/E Multiple: around 24x

Broadcom’s revenue outlook still looks strong, with sales expected to rise from about $64 billion in fiscal 2025 to about $148 billion by fiscal 2030 as AI semiconductors and VMware software keep expanding.

The model estimates a target price of $407, implying about 8% total upside from the valuation model’s last close price near $377, which suggests the stock looks close to fairly valued rather than deeply undervalued.

See analysts’ growth forecasts and price targets for Broadcom Inc. (It’s free) >>>

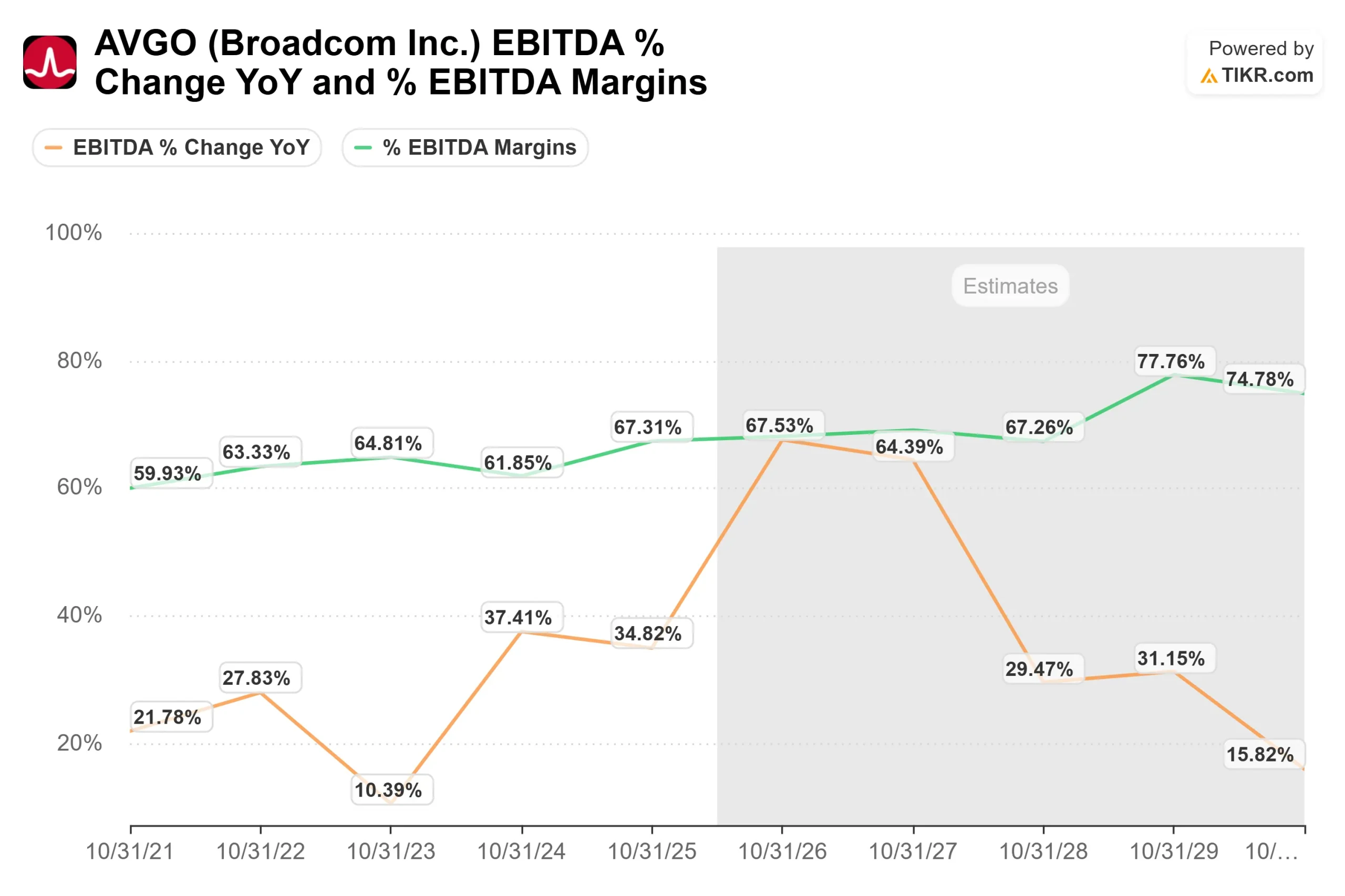

Broadcom’s EBITDA margin profile is a key reason the stock still earns a premium valuation, with profitability expected to remain high as AI semiconductor demand scales and VMware adds more recurring software revenue.

That conclusion matters because Broadcom already trades like a premium AI infrastructure winner, with a P/E near 98x, above Cisco near 40x but below more stretched AI-linked peers like Marvell near 113x and AMD near 175x. Nvidia trades at a lower P/E near 32x, which shows Broadcom’s valuation already reflects high expectations for AI revenue execution and VMware margin strength.

The next year depends heavily on whether Broadcom can keep turning hyperscaler demand into larger custom AI chip and networking orders, especially from major customers building massive AI data centers.

VMware integration is also important because better renewals, stronger subscription pricing, and tighter cost control could keep software margins high while making Broadcom less dependent on chip cycles.

At current levels, Broadcom looks fairly valued, with future returns driven more by AI revenue execution, VMware cash flow, and margin discipline than by multiple expansion.

How Much Upside Does Broadcom Stock Have From Here?

Investors can estimate Broadcom’s potential share price, or what any stock could be worth, in under a minute using TIKR’s New Valuation Model tool.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

Value Broadcom Inc. in under 60 seconds with TIKR (It’s free) >>>