Key Stats for AMD Stock

- Current Price: $540.91

- Target Price (Mid): ~$2,240

- Street Target: ~$486

- Potential Total Return: ~310%

- Annualized IRR: ~36% / year

- Earnings Reaction: +18.61% (May 5, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Advanced Micro Devices (AMD) has spent 2026 forcing Wall Street to answer one question: how do you value a company that keeps outrunning its own analysts? On June 12, one of the Street’s most stubborn skeptics blinked. Citi’s Atif Malik upgraded AMD to Buy from Neutral and lifted his target to $575 from $460, and the stock rose about 5% that day. Three days later, AMD acquired memory startup MEXT and touched a record high, pushing its market value above $900 billion.

The tension is that none of this is cheap. AMD trades near $541, yet the average analyst target sits around $486. The stock is already priced above where the typical analyst thinks it belongs. Bulls say the Street is modeling the wrong company. Bears say a stock at more than 60 times next year’s earnings has no room for error.

Why Citi Finally Upgraded AMD Stock

The upgrade was not a new data point. It was a new lens. Malik argued the market still treats AMD as a CPU company that dabbles in graphics chips, when the GPU business alone may be worth more than the whole stock was trading for before his call. His sum-of-the-parts model values AMD’s data center GPU segment at $281 per share on its own.

The anchor is Meta. AMD has confirmed a deal to deploy up to 6 gigawatts of Instinct GPUs for Meta, built around its next-generation MI450 chip. Citi believes AMD wins the bulk of that custom-chip business, a view that shifts the debate from whether AMD can compete in AI accelerators to how much of that business the stock still fails to price in. TIKR covered the underlying setup after AMD’s Q1 2026 earnings beat and doubled the CPU market forecast. What is new is that a holdout analyst has joined the bulls.

See historical and forward estimates for AMD stock (It’s free!) >>>

The MEXT Deal Solves a Problem AMD Just Flagged

On June 15, AMD acquired MEXT, whose technology makes flash storage behave more like DRAM (the fast memory beside a processor), expanding usable memory capacity without the cost. Shares rose about 7% and closed at a record.

The timing is the tell. Two weeks earlier, at the Bank of America Global Technology Conference on June 2, CFO Jean Hu named memory cost inflation as a problem AMD was managing. “The memory cost increase at this kind of level we have never seen,” Hu said. MEXT is the answer: rather than fight record memory prices on cost, AMD bought technology that cuts how much expensive memory a workload needs. That is why it matters more than a typical bolt-on.

The same conference showed why memory demand is exploding. Hu pointed to agentic AI, meaning systems that chain many automated steps rather than answering one question, as the fastest-growing driver of CPU demand. “It’s not about answering questions anymore. It’s about orchestration, it’s about database access and a lot of tool execution. And all of those require significant CPU performance,” she said. AMD grew CPU revenue more than 50% year-over-year in Q1 and guided Q2 to more than 70% growth.

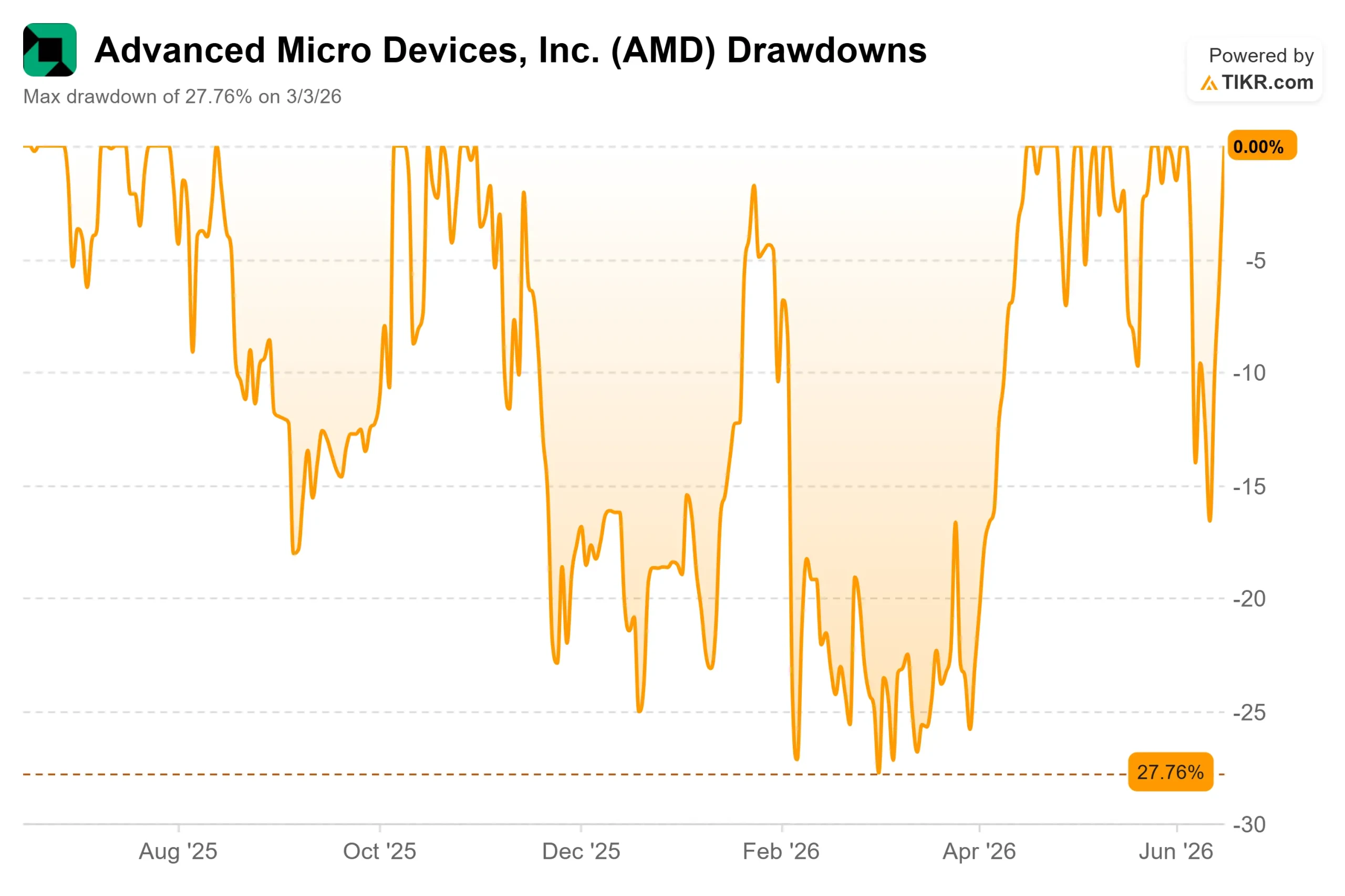

Is AMD Stock Overvalued After Its 2026 Run?

Here, conviction meets arithmetic. AMD has returned more than 330% over the past year and trades near 54 times next-twelve-months EV/EBITDA. That is steep even for this sector. NVIDIA trades near 17 times and Broadcom near 20 times, with the semiconductor peer group averaging about 25 times. AMD’s multiple is more than double that of its closest rivals.

A premium that wide only holds if growth outpaces the group by an equally wide margin, which is exactly the bet bulls are making. TIKR data shows AMD’s forward two-year revenue growing at a roughly 48% compound annual rate, with EBITDA growing faster as the data center mix improves. The engine is visible: Data Center revenue has climbed from $3.7 billion in 2021 to $16.6 billion in 2025.

The risk runs the other way. The MI450 ramp carries below-average margins early, which Hu acknowledged will pressure profitability. NVIDIA’s planned move into server CPUs threatens AMD’s most reliable profit engine. And at this multiple, any slip in the GPU ramp leaves a long way to fall. The bull and bear cases are not really arguing about the company. They are arguing about the price.

See how AMD performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

TIKR’s mid-case values AMD at around $2,240 by the end of 2030, a potential total return of around 310%, or roughly 36% annualized over about four and a half years. The model entry price is $547.26 versus the live quote of $540.91.

- Current Price: $540.91

- Target Price (Mid): ~$2,240

- Potential Total Return: ~310%

- Annualized IRR: ~36% / year

See analysts’ growth forecasts and price targets for AMD stock (It’s free!) >>>

Two drivers carry the case: data center GPU revenue scaling as the MI450 ramps through 2027, and server CPU revenue compounding on the agentic-AI demand Hu described. The margin driver is operating leverage as the mix shifts to higher-value products, lifting net income margins toward the mid-30% range. The primary risk is GPU-ramp execution, where early margins are thin, and the schedule leaves little slack.

The upside: if the MI450 pipeline converts into large 2027 deployments and CPU share keeps rising, the 36% annual return is in reach. The downside: if memory pricing delays the consumer recovery or the ramp underperforms, returns compress toward the low case.

Conclusion

The next test is AMD’s Advancing AI 2026 event on July 22 and 23, followed by Q2 earnings in early August. Watch the data center GPU commentary above all. Management guided server CPU revenue to more than 70% growth in Q2, so meeting that confirms the CPU engine is intact. The swing factor is the MI450: a concrete update showing the ramp on schedule for late 2026, with named 2027 deployments, would validate Citi’s thesis. A vague update, or any slippage, would leave a stock trading above its average target exposed. By early August, investors will know which story is winning.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in AMD?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up AMD, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track AMD alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!