Key Stats for Advanced Micro Devices Stock

- 52-Week Range: $111 to $527

- Current Price: $516

- Street Mean Target: $472

- Street High Target: $625

- Analyst Consensus: 36 Buys / 5 Outperforms / 10 Holds

- TIKR Model Target (Dec. 2030): $2,165

AMD Stock Surges as Q1 Beat Signals a CPU Market That Is Bigger Than Anyone Thought

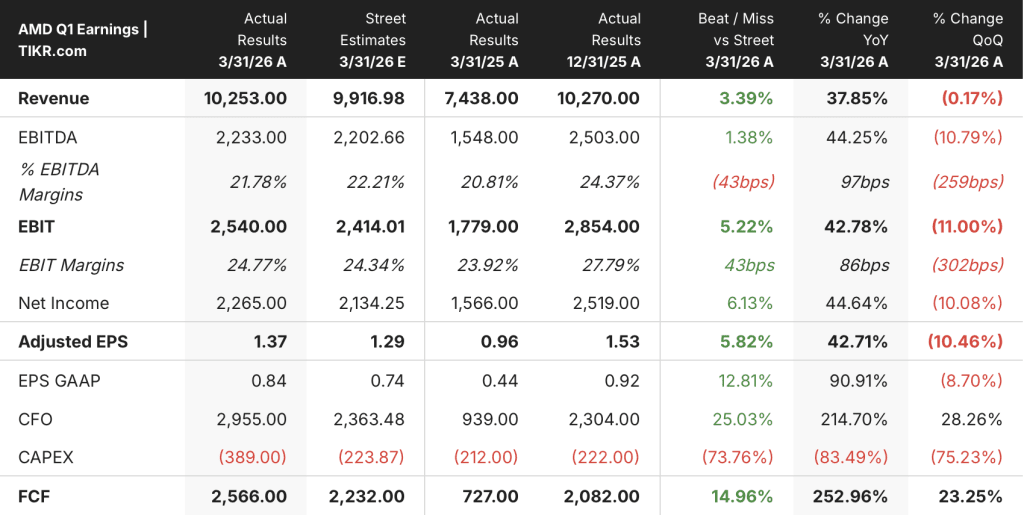

Advanced Micro Devices (AMD) surged to an all-time high following its Q1 2026 earnings on May 6, after reporting revenue of $10,253 million, beating Street estimates of $9,917 million by around 3% and growing 38% year-over-year.

The headline number matters less than what came with it.

On Q1 2026 earnings call, CEO Lisa Su raised AMD’s server CPU total addressable market forecast from around $60 billion growing at 18% annually to over $120 billion growing at greater than 35% annually by 2030, citing the explosion of agentic AI workloads that require significantly more CPU compute per unit of accelerator capacity than prior AI deployments.

“As inferencing scales and you do more agents and agentic AI, they all require CPUs for all of the orchestration and the data processing and these other tasks,” Su said.

Data Center was the engine. Segment revenue hit a record $5.8 billion in Q1, up 57% year-over-year, led by record server CPU revenue growing more than 50% year-over-year across both cloud and enterprise customers. AMD now expects server CPU revenue to grow more than 70% year-over-year in Q2 alone.

The GPU side of the Data Center business also continued to build. AMD confirmed an expanded strategic partnership with Meta to deploy up to 6 gigawatts of Instinct GPUs across multiple product generations, including a custom GPU based on the MI450 architecture co-designed for Meta’s next-generation AI workloads. Combined with the previously announced OpenAI partnership, AMD now has multi-gigawatt, multi-year visibility into GPU deployments at two of the world’s largest AI infrastructure builders.

Client and Gaming contributed $3.6 billion, up 23% year-over-year, with the client business at $2.9 billion growing 26% driven by Ryzen AI processors and accelerating commercial adoption. Embedded returned to growth at $873 million, up 6% year-over-year. Free cash flow reached a record $2,566 million for the quarter, more than tripling year-over-year.

AMD guided Q2 revenue to approximately $11.2 billion, above the Street’s prior estimate, representing around 46% growth year-over-year. Gross margin is expected to come in at approximately 56% in Q2, up from 55% in Q1.

Is AMD Stock a Buy? What Wall Street’s Targets Miss About the 2027 Setup

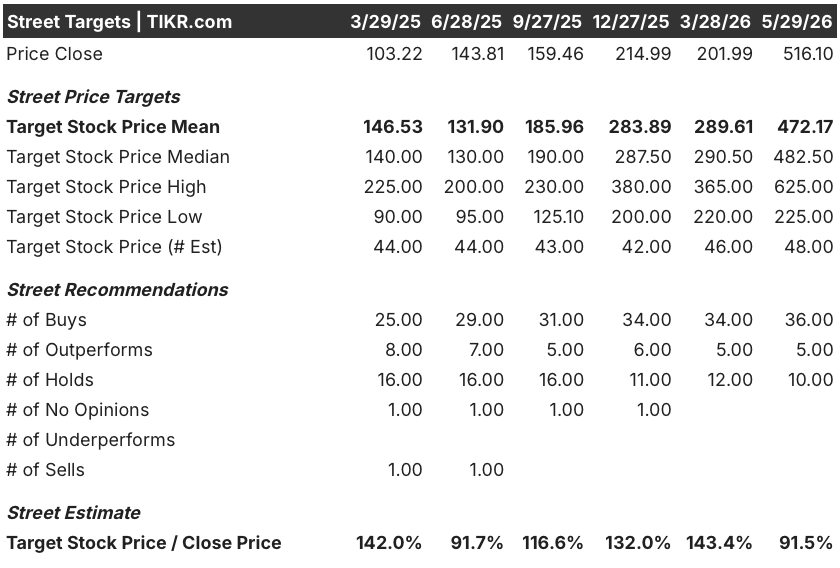

The Street consensus on AMD stock is unusual right now: 36 Buy ratings and 5 Outperforms against 10 Holds, with a mean price target of around $472, which sits below the current price of $516. At the high end, a Street high target of $625 suggests meaningful near-term disagreement within the coverage base.

The disconnect is not a bearish signal. It reflects a coverage base that updated targets immediately after earnings, with over 20 brokerages raising price targets, and a stock that kept running as the scale of the CPU TAM upgrade filtered into broader institutional positioning. The current price has already absorbed much of the near-term rerating.

What the 1-year targets do not capture is the 2027 Data Center AI revenue trajectory. AMD’s management said on the Q1 call that lead customer forecasts for the MI450 and Helios rack-scale platform are now exceeding the company’s initial plans, and that AMD has “strong and increasing confidence” in delivering tens of billions of dollars in annual Data Center AI revenue in 2027. Deployment visibility extends to the specific data centers where GPUs will be installed.

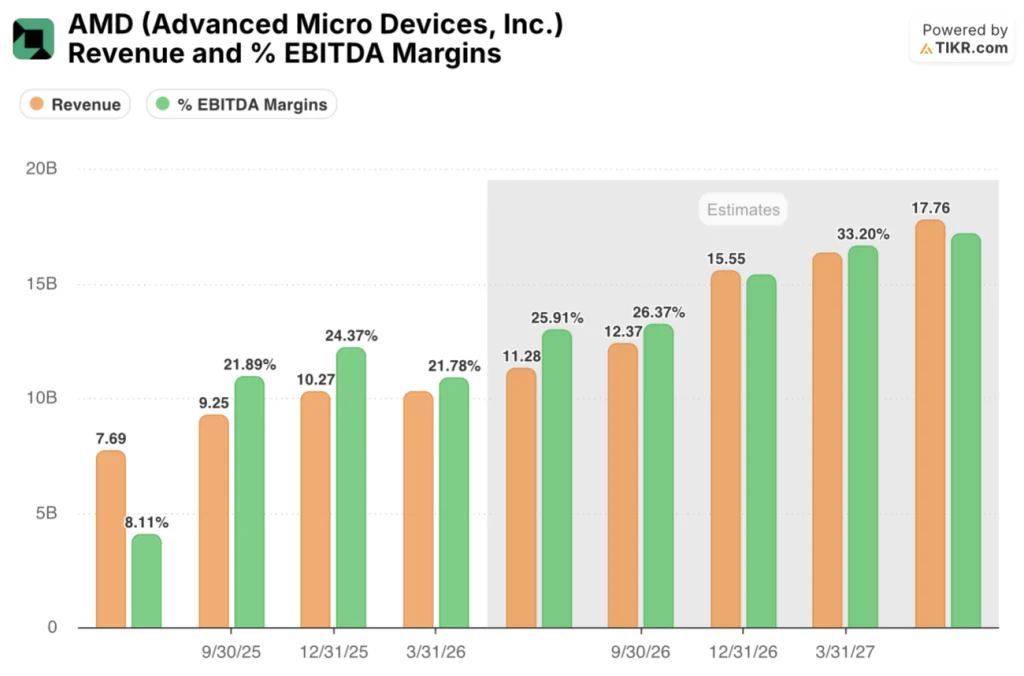

Consensus forward estimates reflect this directionally. Revenue for the June 2026 quarter is estimated at around $11.3 billion, with subsequent quarters stepping up to around $12.4 billion and around $15.6 billion by December 2026. EBITDA margins are expected to expand from the current 22% range to around 26% by mid-2026 and around 31% by December 2026.

The primary risk is execution. MI450 and Helios begin production shipments in the second half of 2026, with an initial volume ramp in Q3 and a significant ramp in Q4. These products carry below-corporate-average gross margins in the early ramp phase, which CFO Jean Hu acknowledged will create near-term margin pressure even as the server CPU tailwind partially offsets it. Memory pricing is also creating demand uncertainty in gaming and consumer PC for the second half of 2026.

Additional context comes from Citigroup’s server CPU market analysis, which forecasts that market reaching around $132 billion by 2030, driven by agentic CPUs growing at extraordinary rates, and currently assigns AMD around 34% of that market by 2030. AMD has explicitly targeted greater than 50% share.

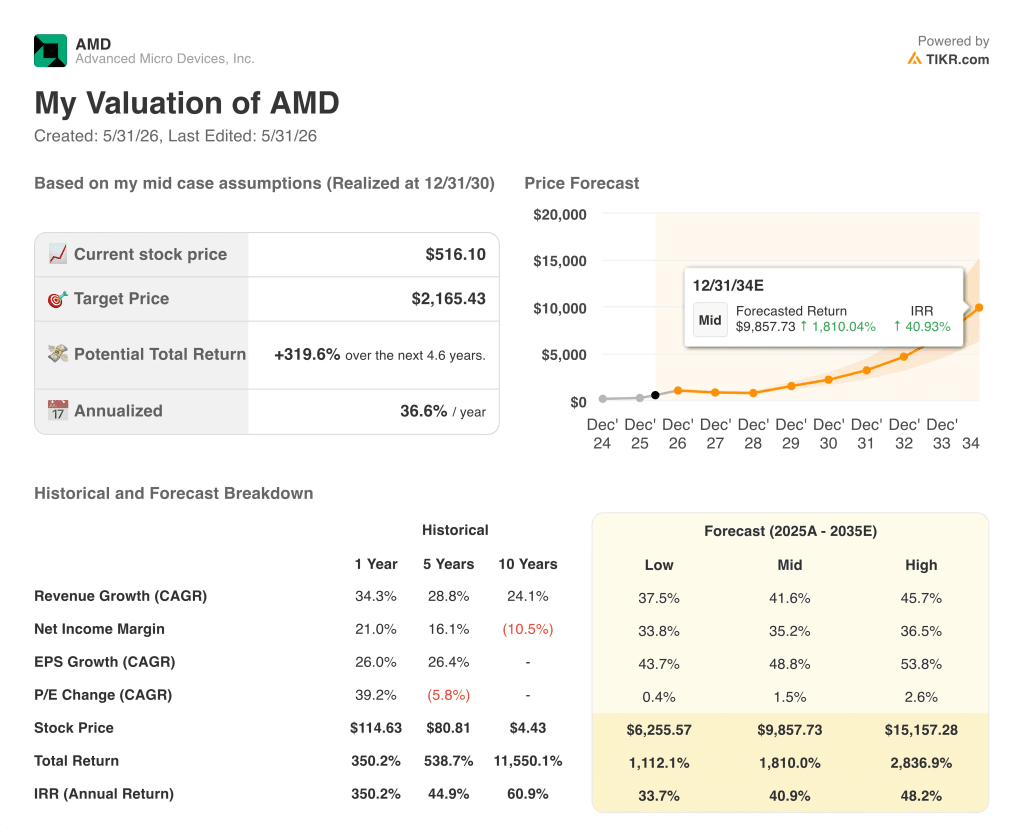

Is AMD Stock Undervalued? TIKR’s $2,165 Mid-Case Points to a Multi-Year Mispricing

TIKR’s base case values AMD stock at approximately $2,165 by December 2030, implying around 320% total return from the current price of $516, or roughly 37% annualized over approximately 4 and a half years.

AMD stock looks undervalued against that multi-year horizon. The low case in TIKR’s model produces a target of around $6,256 by 2035, and the high case reaches approximately $15,157, reflecting the range of outcomes if AMD captures materially more or less than consensus on both the GPU and the server CPU market opportunity over the next decade.

The scenario logic is grounded in what AMD has already committed to.

If the Helios rack-scale platform ramps on schedule in the second half of 2026, the MI450 customer pipeline converts into large-scale 2027 deployments, and server CPU revenue continues compounding at the pace implied by the revised TAM, the base case IRR of around 37% annually is achievable.

If memory pricing delays the PC and gaming recovery into 2027, the GPU ramp underperforms its initial production cadence, or competition from ARM-based merchant CPUs accelerates beyond AMD’s current visibility, the lower scenario of around $6,256 by 2035 frames the downside with an IRR of roughly 34% annually.

The high case, requiring AMD to reach or exceed its greater-than-50% server CPU share target while scaling Instinct into a mainstream second accelerator platform for hyperscalers, implies around $15,157 by 2035 and an IRR of roughly 48% annually.

Is AMD stock a buy right now?

AMD stock carries 36 Buy and 5 Outperform ratings from 51 analysts, with a Street high target of $625 implying around 21% near-term upside from current levels.

The investment case rests on whether the company executes the MI450 and Helios ramp in the second half of 2026 and converts its current pipeline into the tens of billions in annual AI revenue management has committed to for 2027.

TIKR’s multi-year model puts the base-case target at approximately $2,165 by December 2030.

What do analysts say about AMD stock?

Wall Street has 51 analysts covering AMD stock, with 36 Buys and 5 Outperforms against 10 Holds.

The Street mean target of around $472 sits below the current price following the post-earnings rally, but the Street high target of $625 and Evercore ISI’s target of $579 suggest the conviction base expects continued outperformance.

More than 20 brokerages raised price targets after the Q1 2026 earnings beat.

Should You Invest in Advanced Micro Devices, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Advanced Micro Devices, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Advanced Micro Devices, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze AMD stock on TIKR for Free →