Key Stats for Fiserv Stock

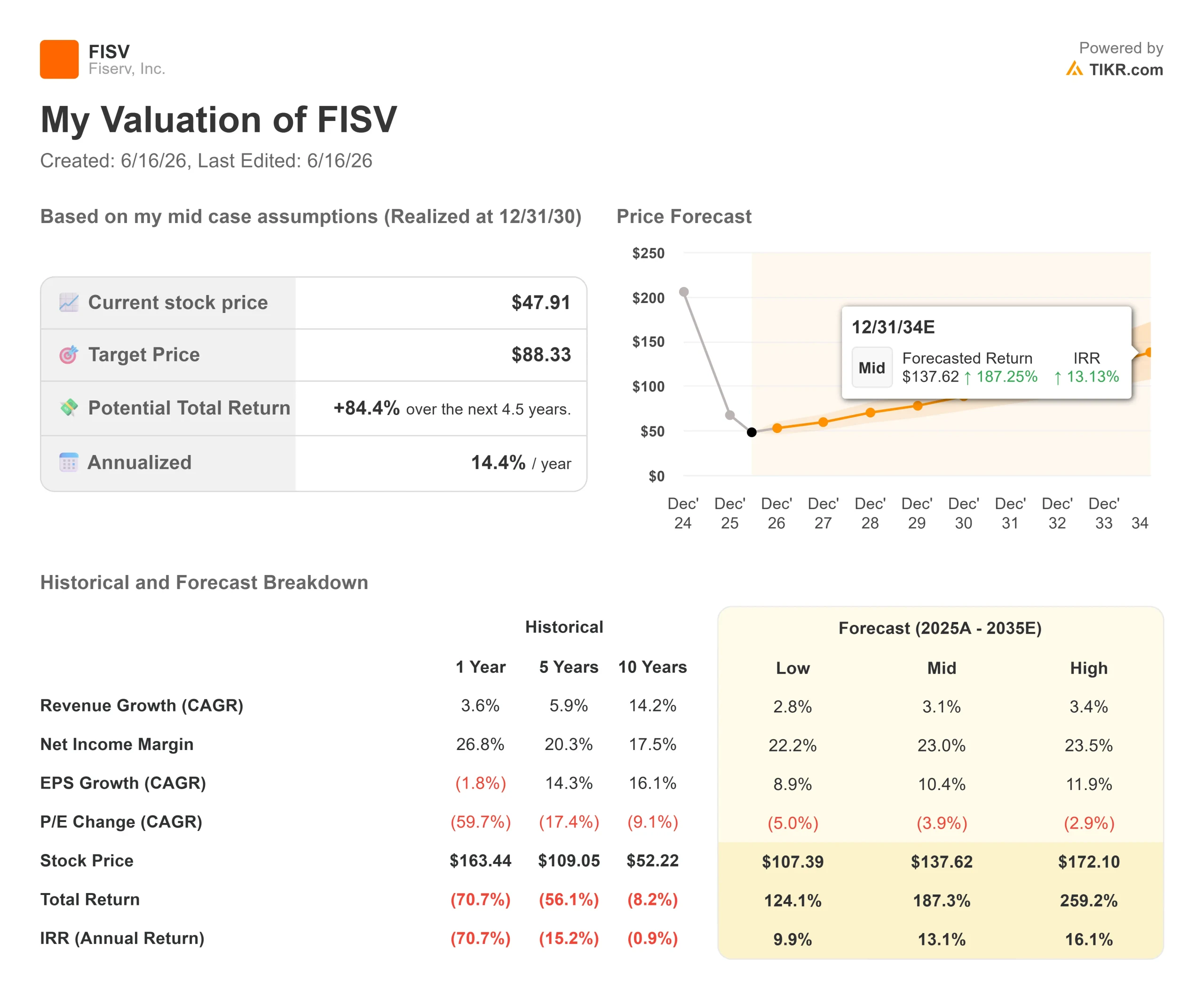

- Current Price: $48.64

- Target Price (Mid): ~$88

- Street Target: $70

- Potential Total Return: ~84%

- Annualized IRR: ~14% / year

- Earnings Reaction: down 2.04% (May 5, 2026)

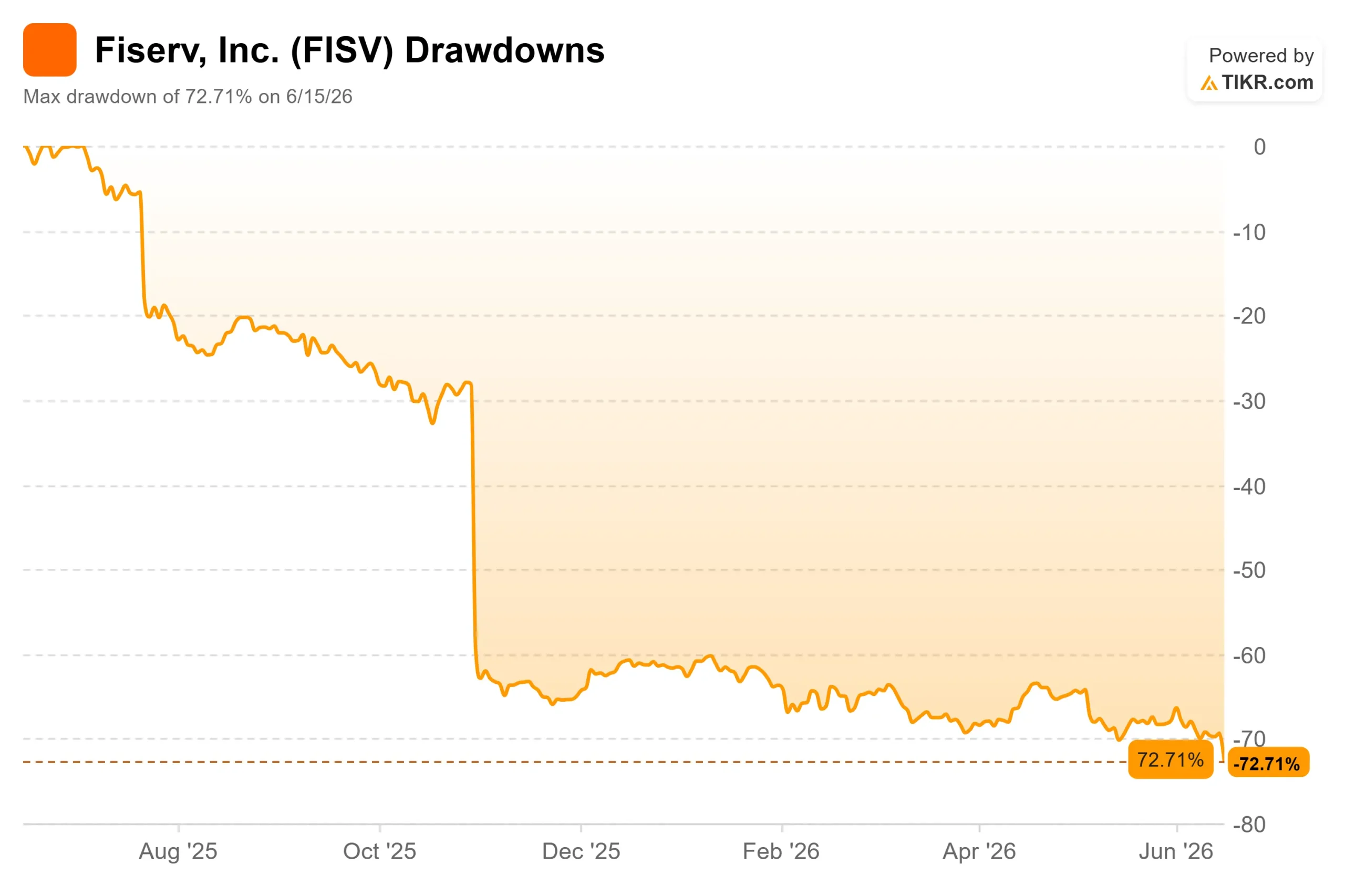

- Max Drawdown: 72.71% (June 15, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Fiserv (FISV) investors woke up on June 15 to a headline almost nobody saw coming. CEO Mike Lyons, barely a year into the job, abruptly stepped down to run Truist Financial, and the board handed the company to Takis Georgakopoulos that morning. The stock fell roughly 8% to multi-year lows, even as Fiserv reaffirmed its full-year guidance.

This is a stock that was already on the floor. Fiserv has fallen 72.71% from its high as of June 15, 2026. So the real debate is not whether the news was bad. It is whether a CEO change this sudden, on a name this beaten down, is the final crack in the thesis or the kind of capitulation that marks a bottom.

A CEO swap that raised more questions than it answered

Georgakopoulos is not an outsider. He joined Fiserv in 2024 from J.P. Morgan, where he ran payments for the Corporate and Investment Bank, and most recently served as Co-President over Merchant Solutions and Technology. That continuity is the bull’s comfort: the new CEO already owns the Clover and merchant strategy that the turnaround leans on.

The timing is the problem. Lyons left less than a month after an Investor Day meant to sell the Street on the long-term plan. Bernstein called the exit a “bad look,” and Morgan Stanley said it adds to the uncertainty around the name. What blunts the panic: Fiserv reaffirmed its 2026 outlook the same day, with no change to the numbers.

- Organic revenue growth: 1% to 3%

- Adjusted EPS: $8.00 to $8.30

For a business built on recurring, contracted revenue, that nothing-changed-but-the-name distinction is the whole argument.

See historical and forward estimates for Fiserv stock (It’s free!) >>>

The activist in the room

The swap did not happen in a vacuum. Six days earlier, activist hedge fund Jana Partners went public with its campaign, pushing Fiserv to sell non-core assets and refresh its board with directors who understand payments and banking software. A board under activist pressure, a sudden CEO change, and a reaffirmed plan all inside one week is less a coincidence than a company in motion. Jana’s track record, from Pinnacle Foods to Conagra, says it does not buy positions to sit quietly.

Why the operating story still holds together

Strip away the drama, and the business is doing roughly what management said it would. CFO Paul Todd, speaking at the Baird Global Consumer, Technology & Services Conference on June 2, 2026, argued the volume engine is intact even when reported revenue looks noisy:

“The underlying volumes across the business have been very stable, and we expect that stability to continue.”

That matters because volume, not pricing, underpins Fiserv’s 4% to 6% long-term revenue framework. Clover is the growth driver, and Todd’s guidance breaks down cleanly:

- Clover volume growth: 10% to 15%

- Clover revenue growth: 15% to 20%, with the gap from value-added services like Clover Capital and the new Clover Savings

- Merchant Solutions (second half): 6% to 8%, partly on contracted revenue coming online

Todd was honest that the back-half strength is partly timing, calling it “slightly above the normalized 4% to 6%” range. The flip side: 2026 earnings are still set to dip below 2025 before the algorithm is meant to reassert in 2027.

What the valuation is actually pricing

Here is the disconnect. Fiserv trades at an NTM (next twelve months) P/E of 5.89x and an NTM EV/EBITDA of 6.14x. For a company that compounded double-digit EPS growth for most of its 40-year history, those are distressed multiples on a business that is not distressed. Free cash flow is still real, with LTM levered FCF near $4.6 billion, and net debt to EBITDA of 3.32x is elevated but manageable.

The bear case writes itself: low-single-digit organic growth, first-half margin compression, buybacks on hold, and now a CEO who walked. Analyst sentiment reflects caution. As of June 15, 2026, the Street sits at:

- 6 Buys, 3 Outperforms, 24 Holds, 1 Underperform, 1 Sell

- Mean target: $70

Todd said buybacks wait until leverage drops “below 3x,” which he framed as a next-year event, so the capital-return lever that long supported EPS is parked for now.

The bull case is the mirror image. If volumes are as stable as Todd insists and the second-half acceleration shows up, a stock near 6x earnings has priced in a permanent stall that the data does not yet support. The whole question is whether the first-half margin trough is a reset or a leak.

See how Fiserv performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $48.64 (TIKR model entry price: $47.91)

- Target Price (Mid): ~$88

- Potential Total Return: ~84%

- Annualized IRR: ~14% / year

See analysts’ growth forecasts and price targets for Fiserv stock (It’s free!) >>>

The model uses the mid-case because it mirrors management’s own framework: a transition year now, then a return to compounding. Off a $47.91 entry, that points to a target of around $88, or roughly 84% total return and about 14% annualized.

- Revenue drivers: Clover and the small-business segment (high-single-digit growth led by value-added services), plus the stable transaction-volume base across issuing, banking, and enterprise merchant

- Margin driver: operating leverage, including the Project Elevate efficiency program

- Primary risk: execution under brand-new leadership

- The upside: if volumes hold and margins recover, a stock under 6x earnings re-rates higher.

- The downside: if first-half margin compression proves structural, the cheap multiple is cheap for a reason, and Jana gets a longer fight than it wants.

Conclusion

Watch Fiserv’s second-quarter 2026 report, expected in late July. It is the first hard checkpoint on management’s promise that the back half accelerates.

- Good: organic growth holding inside the 1% to 3% guide, with margins recovering sequentially

- Bad: another margin miss and a guide-down, which would hand Jana its strongest argument and pressure a CEO in his first quarter

The leadership change did not break the thesis. It raised the stakes on proving it. By the end of July, the numbers will say more than any press release.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Fiserv?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Fiserv, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Fiserv alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!