Key Stats for EOG Resources Stock

- Year-to-Date Performance: 15%

- 52-Week Range: $102 to $132

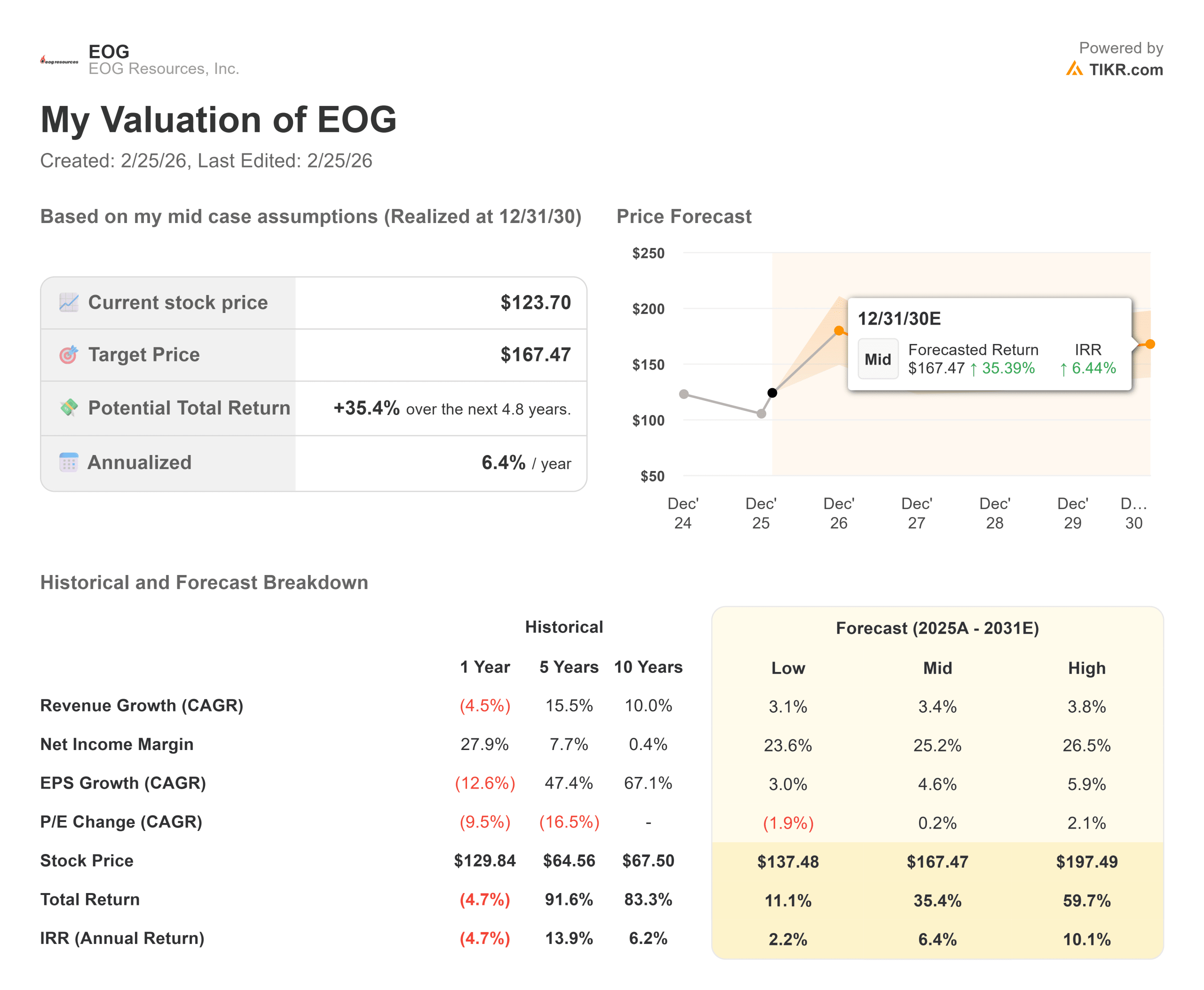

- Valuation Model Target Price: $167

- Implied Upside: 35%

Value your favorite stocks like EOG Resources with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

EOG Resources is up about 15% year to date, recently trading near $121 per share as investors responded to improving capital efficiency, disciplined spending, and sustained shareholder returns heading into 2026.

Shares have remained resilient despite range-bound oil prices, signaling growing confidence in the company’s free cash flow durability.

The stock advanced after management outlined a leaner $6.5 billion capital plan for 2026, slightly below the prior $6.6 billion run-rate, while guiding to no to low oil growth versus the fourth quarter of 2025.

Investors reacted positively to visible cost reductions in the Delaware Basin and faster-than-expected integration of the Encino acquisition, which is expected to generate about $150 million in synergies. Lower capital intensity combined with strong well-level economics reinforced the stability of EOG’s cash flow profile.

This week at the Goldman Sachs Energy Conference, CFO Ann Janssen noted that Delaware well costs have fallen about 15% over the past two years and continue to generate greater than 60% after-tax returns with paybacks around one year, calling the basin “the gift that keeps on giving.”

Management reaffirmed its commitment to returning 90% to 100% of free cash flow to shareholders, supported by a $4.08 annual dividend yielding 3.9%, underscoring confidence in capital returns even in a softer pricing backdrop.

Institutional positioning has also supported sentiment. Fiera Capital raised its stake by 20.7% to 68,635 shares worth about $7.7 million, Alberta Investment Management boosted its holdings by 254.5% to 19,500 shares, and NewEdge Wealth increased its position by 40.5% to 356,650 shares valued near $37.5 million.

NEOS Investment Management lifted its stake by 43.4% to 77,750 shares, and Vanguard added 94,203 shares to hold 53,369,215 shares, or 9.77% of the company, as institutional ownership stands near 89.91%. While some firms trimmed exposure, overall positioning suggests continued long-term conviction.

See analysts’ growth forecasts and price targets for EOG Resources (It’s free) >>>

Is EOG Resources Undervalued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth (CAGR): 3.4%

- Net Income Margin: 25.2%

- Exit P/E Multiple Change: 0.2%

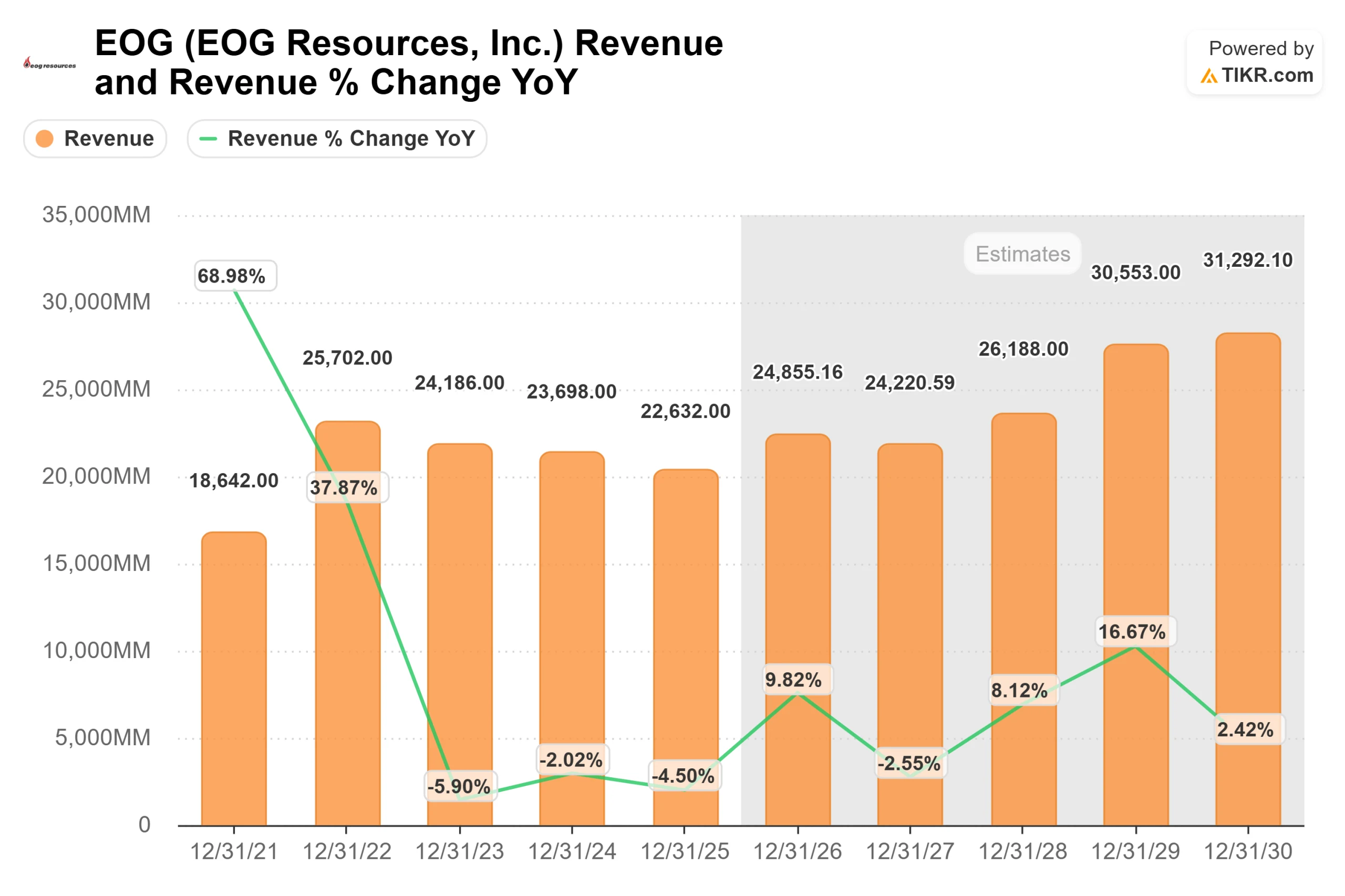

Revenue is projected to recover from $22.6 billion in 2025 to about $31.3 billion by 2030, reflecting steady production volumes and disciplined reinvestment rather than aggressive expansion.

With LTM EBIT margins near 32% and gross margins around 62%, EOG maintains one of the strongest profitability profiles among large-cap exploration and production companies.

The key driver is capital efficiency. Delaware Basin well costs have declined roughly 15%, and the basin continues generating greater than 60% after-tax returns with payouts near one year.

That cost structure allows EOG to remain profitable even at lower oil prices, creating operating leverage if commodity prices improve. At a flat $45 WTI environment, management indicated returns can still exceed 100%, highlighting resilience across cycles.

Encino integration adds incremental upside through roughly $150 million in identified synergies, while international exploration in Bahrain and the UAE introduces longer-term optionality.

At the same time, the company continues returning 90% to 100% of free cash flow to shareholders through dividends and buybacks, supporting per-share value creation.

At around $121 per share, the model’s mid-case target of $167 implies roughly 35% upside into 2026, suggesting the stock appears undervalued if operational discipline and cost efficiencies persist.

Realized crude pricing, continued well productivity gains, and free cash flow execution will likely determine how much of that upside materializes this year.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Value Any Stock in Under 60 Seconds (It’s Free)

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>