Key Takeaways:

- Eaton delivered Q1 2026 net sales of $7.5 billion, up 17% year over year, fueled by data center electrical infrastructure demand and grid modernization spending.

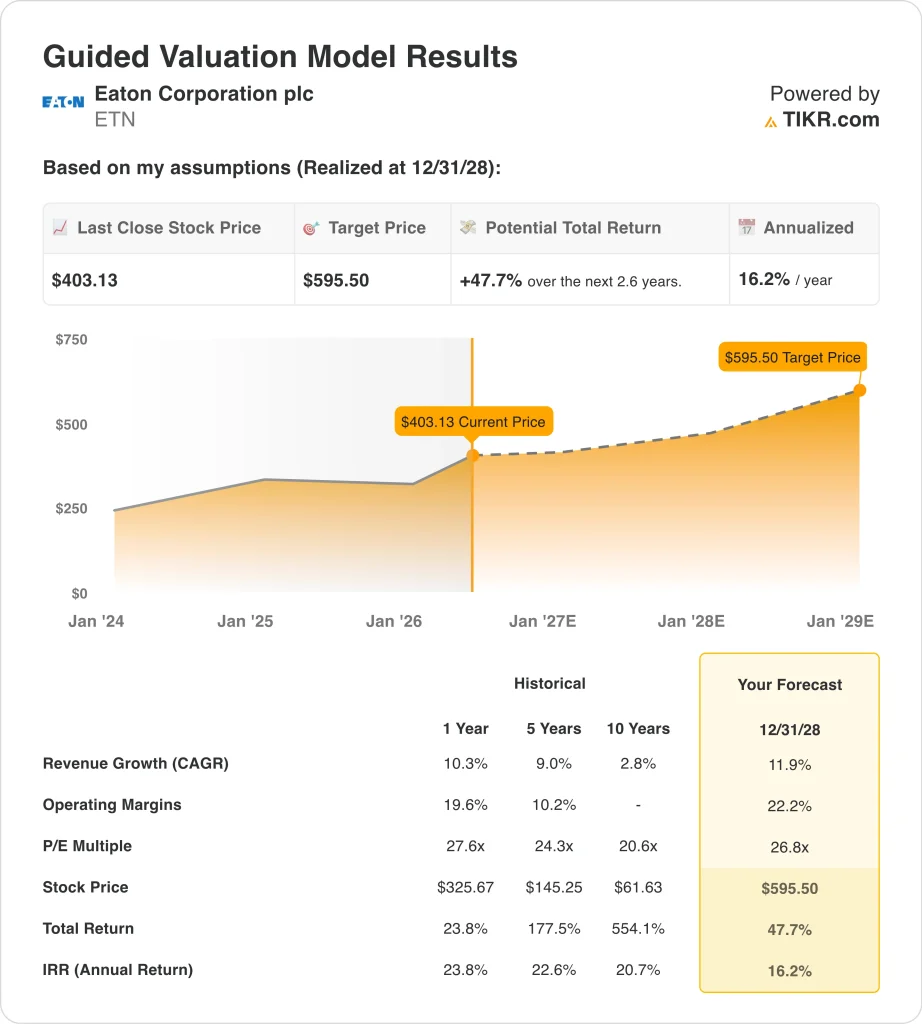

- ETN stock trades near $403, and the Street consensus target is around $452, while the 52-week range spans from $312 to $435.

- ETN stock could rise from $403 to around $596 per share by December 2028, representing a 47.7% total return and a 16.2% annualized return over the next 2.6 years.

What Happened?

Eaton Corporation (ETN) reported Q1 2026 net sales of $7.5 billion, up 17% year over year. Growth was powered by strong demand for electrical switchgear and data center power solutions. Net earnings per share fell 9.4% to $2.22, reflecting higher operating costs during the quarter. Investors found themselves balancing strong top-line momentum against near-term margin headwinds.

Eaton is exploring a potential sale or spinoff of its vehicle unit, estimated at roughly $5 billion. That strategic move would let the company concentrate resources on its faster-growing electrical and aerospace businesses.

Eaton also committed over $30 million to a new Nebraska switchgear plant serving data center customers. A 370,000-square-foot Omaha facility is set to begin production in 2027, signaling long-term capacity confidence.

The company raised its quarterly dividend to $1.10 per share, reflecting confidence in free cash flow generation. ETN stock recently closed near $403, and the Street consensus target sits at around $452. The company also won an EcoVadis gold medal, ranking in the top 4% globally for sustainability.

Eaton’s LTM return on equity stands at 20.8%, pointing to disciplined capital allocation. The electrical segment benefits from AI infrastructure spending, grid modernization, and domestic manufacturing reshoring. These demand drivers are expected to remain supportive across the multi-year buildout cycle.

Here’s why Eaton stock could offer solid capital returns through 2028 as its core business drivers support shareholder value.

What the Model Says for ETN Stock

We analyzed the upside potential for Eaton stock based on its electrical infrastructure leadership, growing data center exposure, and improving operating leverage across its core segments.

Based on estimates of 11.9% annual revenue growth, 22.2% operating margins, and a normalized P/E multiple of 26.8x, the model projects Eaton stock could rise from $403 to around $596 per share.

That would be a 47.7% total return, or a 16.2% annualized return over the next 2.6 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for ETN stock:

1. Revenue Growth: 11.9%

Eaton’s Q1 2026 net sales rose 17% year over year to $7.5 billion. This growth was powered by data center buildout spending and grid modernization projects across the U.S.

The forward two-year revenue CAGR estimate stands at 13.6%, supported by strong backlogs in the electrical segment. Analysts expect reshoring trends and domestic energy infrastructure investment to sustain demand.

Based on analysts’ consensus estimates, we used 11.9% annual revenue growth. This reflects a modest moderation from recent performance while accounting for Eaton’s multi-year backlog and diversified electrical product portfolio.

2. Operating Margins: 22.2%

Eaton’s LTM EBIT margin reached 18.6%, and historical operating margins show consistent improvement over the past several years. The potential vehicle unit divestiture could improve blended margins by removing a lower-margin business from the mix.

AI data center customers typically require high-specification switchgear, which tends to carry better margins than standard electrical products. Eaton’s new Nebraska and Omaha production capacity supports this premium product mix strategy going forward.

Based on analysts’ consensus estimates, we used 22.2% operating margins. This accounts for favorable product mix shifts toward higher-margin electrical infrastructure and operating leverage as revenues scale.

3. Exit P/E Multiple: 26.8x

Eaton currently trades at an NTM P/E of around 28.6x, reflecting investor confidence in the electrification theme. The stock’s pullback from the 52-week high of $435 has modestly compressed the multiple from peak levels.

A normalized multiple of 26.8x is slightly below the current NTM level, keeping the model conservative. This avoids assuming meaningful multiple expansion beyond current market pricing.

Based on analysts’ consensus estimates, we used a 26.8x exit P/E multiple. This reflects Eaton’s durable competitive position in electrical infrastructure and its consistent dividend growth track record.

Build your own Valuation Model to value any stock (It’s free!) >>>

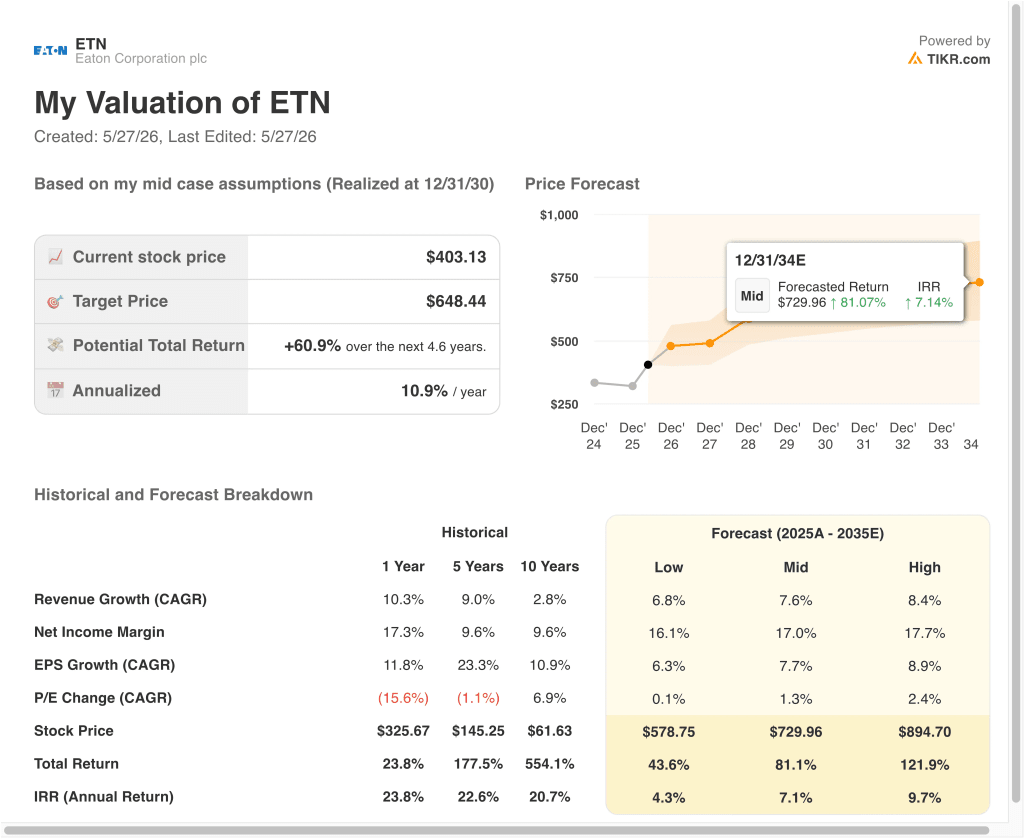

What Happens If Things Go Better or Worse?

Different scenarios for ETN stock through 2035 show varied outcomes based on electrical segment growth rates, margin trajectory, and vehicle unit divestiture execution (these are estimates, not guaranteed returns):

- Low Case: Slower data center demand and margin compression limit overall growth → 4.3% annual returns

- Mid Case: Consistent electrical backlog execution and moderate margin expansion sustain the business → 7.1% annual returns

- High Case: Accelerating AI infrastructure spending and a successful vehicle unit divestiture boost profitability → 9.7% annual returns

Going forward, the near-term model projects 16.2% annualized returns through December 2028, suggesting the stock may be attractively priced relative to its earnings growth potential. However, the longer-term advanced model scenarios range from 4.3% to 9.7% annually through 2035, reflecting more moderate expectations as the initial AI buildout cycle matures.

Investors should watch the vehicle unit strategic review and Q2 2026 results, due July 27, for signs that margins are recovering alongside continued top-line strength.

See what analysts think about ETN stock right now (Free with TIKR) >>>

Should You Invest in Eaton?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up ETN, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track ETN alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze the stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!