Key Stats for LRCX Stock

- Past-Week Performance: 16%

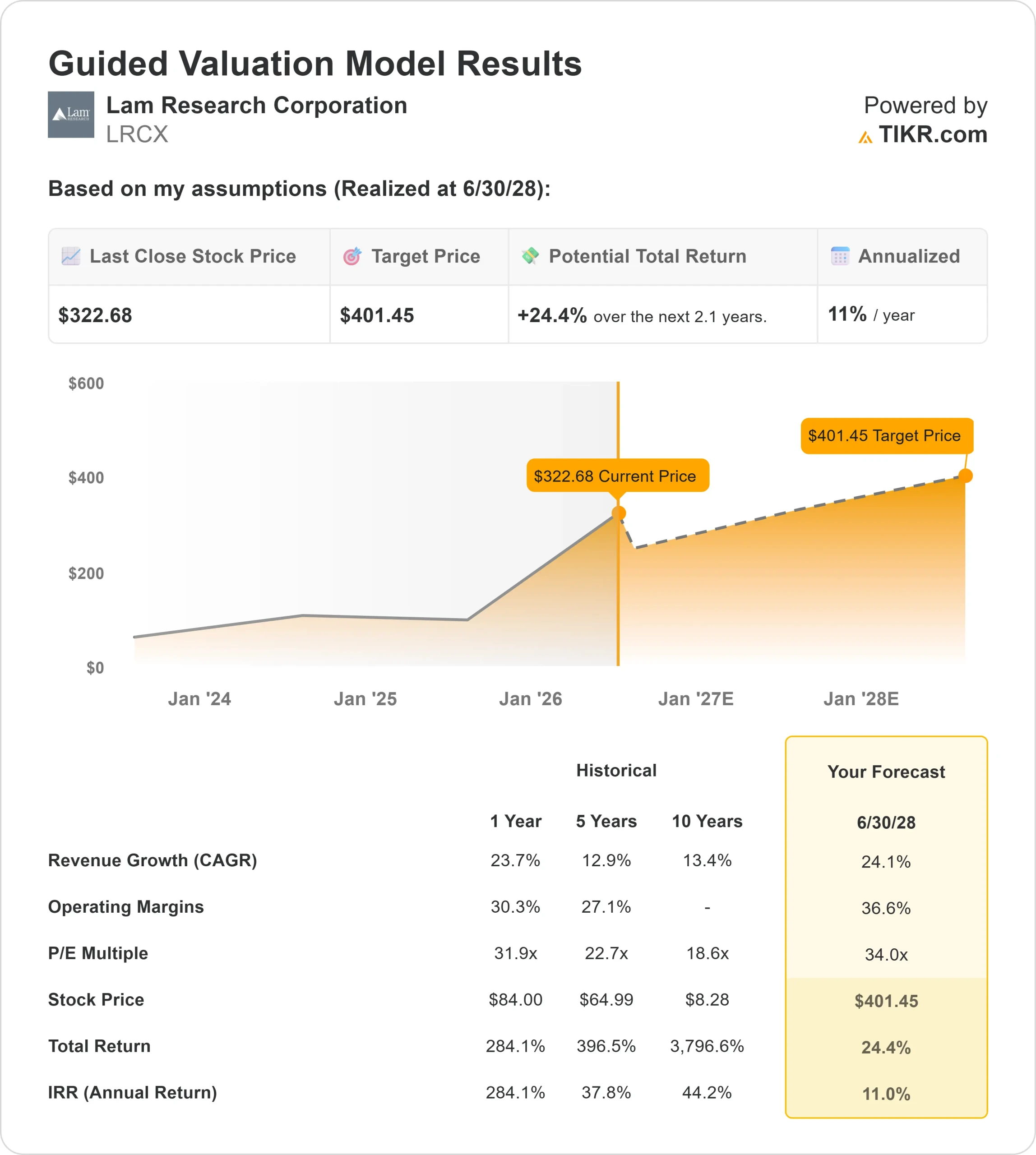

- 52-Week Range: $79 to $324

- Valuation Model Target Price: around $400

- Implied Upside: 24%

Analyze your favorite stocks like Lam Research Corporation with TIKR (It’s free) >>>

What Happened?

Lam Research Corporation stock rose about 16% this week, finishing near $323 per share as investors moved back into semiconductor equipment stocks tied to AI chip demand and rising memory investment. Lam makes etch, deposition, and customer support tools that help chipmakers manufacture advanced semiconductors, putting it in the same equipment conversation as Applied Materials, KLA, ASML, Tokyo Electron, and ASM International. The peer context matters because Applied Materials competes across several chip-equipment categories, KLA is stronger in inspection and process control, ASML dominates lithography, and Lam’s edge is especially important in etch and deposition steps used for more complex memory chips.

The stock moved higher because Morgan Stanley’s upgrade gave investors a clear reason to reprice Lam around stronger AI-driven memory equipment demand in 2026.

Morgan Stanley upgraded Lam Research to Overweight from Equal-weight and raised its price target to $331 from $293, citing a stronger NAND outlook, sustained systems shipment strength, margin expansion drivers, and Lam’s positioning in DRAM and advanced packaging transitions. That mattered because NAND, DRAM, and high-bandwidth memory are becoming more important for AI servers, and Lam’s tools help chipmakers build those more complex memory devices at higher yields.

The recent earnings call added more support to the move, with March-quarter revenue rising 24% year over year and 9% sequentially to a record $5.84 billion, while non-GAAP EPS reached a record $1.47.

CEO Tim Archer said the AI-driven demand environment is creating an “ideal setup for continued outperformance,” and the company raised its 2026 wafer-fab equipment outlook to $140 billion with upside bias. Lam also guided for June-quarter revenue of $6.60 billion, non-GAAP gross margin of 50.5%, non-GAAP operating margin of 36.5%, and record non-GAAP EPS of $1.65, showing that AI-related demand is already flowing through the income statement.

Recent company-related news also gave investors a more practical reason to care about Lam’s role in AI manufacturing. Lam is adding more AI and sensing capabilities to its chipmaking tools while expanding its U.S. footprint near major customers. Better sensors and AI can help chipmakers spot defects earlier, improve yield, and produce more usable chips per wafer, which is especially valuable when AI chip supply remains tight.

Value Lam Research Corporation instantly (Free with TIKR) >>>

Is LRCX Undervalued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth (CAGR): around 24%

- Operating Margins: around 37%

- Exit P/E Multiple: 34x

Lam Research appears undervalued based on the valuation model, which estimates a target price of around $400 and implies about 24% total upside.

The main business driver is memory equipment spending, because AI servers need more NAND, DRAM, and high-bandwidth memory, and those chips require more complex etch, deposition, and advanced packaging steps.

See analysts’ growth forecasts and price targets for Lam Research Corporation (It’s free) >>>

Margins could also keep improving if higher revenue spreads fixed costs across a larger base, while better product mix and Lam’s customer support business help customers improve output from existing fabs.

The biggest factor for 2026 is whether memory customers keep pulling forward NAND conversions and adding capacity to meet AI data center demand, while China exposure and customer capex timing remain the main risks.

At current levels, Lam Research looks undervalued, with future performance driven by AI-related memory investment, advanced packaging growth, and the company’s ability to turn stronger demand into higher earnings power.

How Much Upside Does LRCX Stock Have From Here?

Investors can estimate Lam Research Corporation’s potential share price, or what any stock could be worth, in under a minute using TIKR’s New Valuation Model tool.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

Value Lam Research Corporation in under 60 seconds with TIKR (It’s free) >>>