Key Stats for Doximity Stock

- 52-Week Range: $17 to $77

- Current Price: $20

- Street Mean Target: $25

- Street High Target: $42

- Analyst Consensus: 5 Buys / 5 Outperforms / 12 Holds

- TIKR Model Target (Mar. 2031): $31

Doximity Drops 24% After FY27 Revenue Guidance Falls $13 Million Short of Wall Street

Doximity (DOCS) fell sharply following fiscal Q4 2026 earnings after management guided FY27 revenue to between $664 million and $676 million, roughly $13 million below the Wall Street consensus of around $689 million.

The guidance miss landed on top of an already struggling Doximity stock. DOCS had fallen around 47% year-to-date heading into the print, pressured by CFO Anna Bryson’s mid-April resignation after a medical leave and a market increasingly skeptical about near-term pharma advertising spend.

The quarter itself held up: Q4 revenue came in at $145.4 million, a 5% year-over-year increase that finished above the high end of guidance, and adjusted EBITDA of $65.8 million beat the $64.3 million consensus estimate.

The full fiscal year told a more constructive story, with revenue reaching $645 million, up 13% year-over-year, and free cash flow of $317 million, up 19%.

What unnerved the street was not what happened but what management said about fiscal 2027: this is, by their own framing, an “AI investment year.”

CEO Jeff Tangney was direct about the trade and stated on Q4 2026 earnings call: “We’ve forecasted minimal AI revenue contribution this fiscal year while allowing for a wider range of AI investments and related expenses meaning higher R&D, compute and marketing spend that will weigh on near-term margins.”

The investment being made has a specific origin (the $63 million acquisition of Pathway AI last summer) and a specific commercial target: entering pharma’s paid search market with an AI Search product the company launched commercially in late April.

Engagement is running hard ahead of monetization.

Quarterly active prescribers using workflow tools reached over 800,000 in Q4, up roughly 30% year-over-year, the fastest rate of growth on record, and nearly half of that base used Doximity’s AI tools in the quarter.

140 health systems have purchased the clinical AI suite, including 7 of the top 20 hospitals in the U.S., and Doximity reached that milestone in two quarters, a pace that took two full years with its telehealth product.

The thesis break the market is betting on is that pharma ad budgets remain soft long enough to make the AI investment year a permanent deceleration story rather than a temporary reset.

Tangney disagrees: “Longer term, we believe AI search alone represents a multibillion dollar new TAM on top of the existing pharma marketing budgets we serve today.”

Whether that TAM materializes in the fiscal back half is the unresolved question that makes Doximity stock worth watching closely from here.

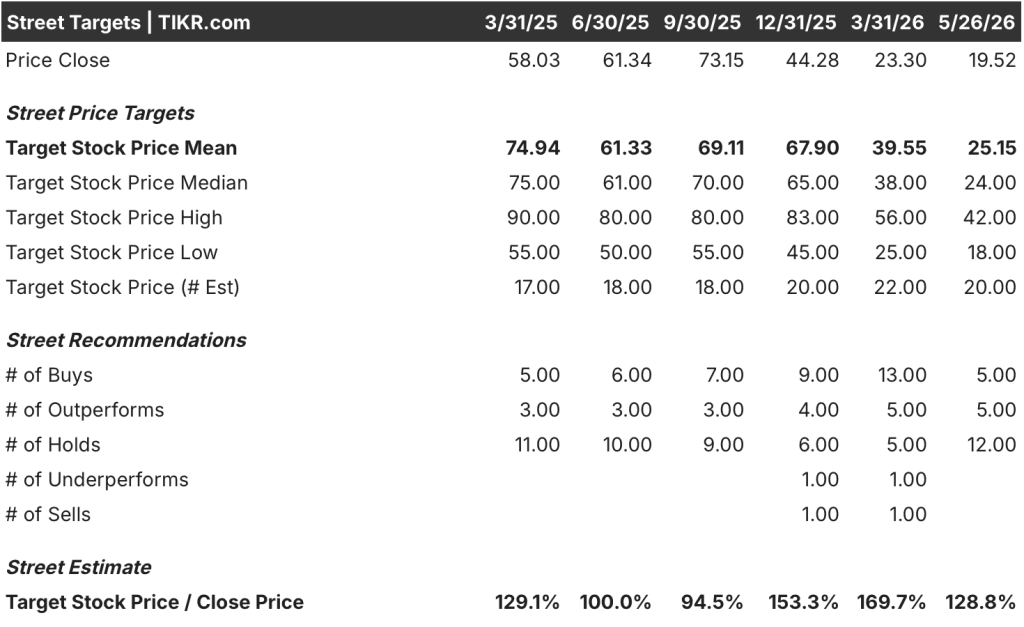

With 20 Analysts Covering DOCS, Here Is What the Consensus and the Data Actually Say

The selloff stripped Doximity stock of most of its premium, and Wall Street’s response was mixed: a cluster of cuts, a handful of holds, and a small core of buy-rated analysts who kept their theses intact.

The current analyst breakdown sits at 5 Buys, 5 Outperforms, and 12 Holds, with no sells, a distribution that reflects genuine disagreement about the pace of AI monetization rather than a fundamental rejection of the business.

The Street Mean Target of $25 implies around 28% upside from the current price of around $20, with the high target of $42 implying more than 100% if the AI Search cycle inflects faster than the base case assumes.

DOCS’ EPS normalized is the sharpest lens on the near-term trade: at $0.26 for Q4 actual, the year-over-year decline of 31.6% captures exactly what the market is pricing, a profitability air pocket during the AI investment period.

Consensus sees EPS Normalized recovering, with estimates of $0.30 for the June 2026 quarter, $0.37 for September, and $0.44 for December, a trajectory suggesting the market bottom for earnings is likely Q4 that just closed.

Free cash flow also offers the cleaner view of DOCS’s underlying economics: $317 million for full fiscal 2026, up 19% year-over-year, representing around 49% of revenue, a margin that no amount of AI compute spend has meaningfully eroded at the full-year level.

The risk case is not hidden: FY27 adjusted EBITDA guidance of $323 to $335 million implies a margin step-down from fiscal 2026’s 55% to roughly 49%, a compression that Wall Street is attributing to rising AI compute costs and brand marketing investment.

The catalyst the bulls are watching is the second half of fiscal 2027, when AI Search deals that survive pharma’s regulatory review process should begin converting to recognized revenue.

At 5 Buys, 5 Outperforms, and 12 Holds, the distribution says: most analysts believe the business is intact, but they want one more quarter of data before upgrading.

With the engagement rate growing at 30% year-over-year and the AI monetization pipeline now open, the data DOCS needs to show is not growth in physician usage (it has that) but conversion of that usage into paid search revenue from pharma budgets.

Is DOCS Stock Undervalued in 2026? What TIKR’s Model Says About the $31 Target

TIKR’s base case values Doximity at around $31 by March 2031, implying around 59% total return from the current price of around $20, or roughly 10% annualized over approximately 5 years.

The mid-case assumptions running beneath that target are a revenue CAGR of around 6%, a net income margin of around 44%, and an EPS growth CAGR of around 6%, with a modest P/E contraction of around 1% annually over the forecast period, a conservative framing that does not require AI Search to become a meaningful revenue line to get DOCS to $31.

The tension is the timeline: with AI monetization revenue not expected to be meaningful until the fiscal back half at earliest, the path to the target requires the market to regain confidence in pharma ad spend recovery before the model’s assumptions start appearing in reported results.

If pharma budgets remain soft and AI Search revenues ramp later than the second half guidance implies, the low case produces a stock price of around $29 by March 2031 and an IRR of around 5%, a scenario where Doximity stock still returns capital but slowly, and the 10% annualized base case never arrives.

If AI Search closes a meaningful share of pharma’s paid search budgets in the fiscal back half, the high case points to around $46 by March 2031 and an IRR of around 10%, a return profile that would re-rate the stock well before the target date.

TIKR’s model signals DOCS is undervalued at the current price of around $20, with the mid-case alone implying around 59% total return from here and the high case nearly doubling that.

Is Doximity stock undervalued right now?

At around $20, Doximity stock trades at approximately 75% below its 52-week high of $77. TIKR’s base case values DOCS at around $31 by March 2031, implying roughly 59% total return or around 10% annualized.

The Street Mean Target of $25 also sits above the current price. The variable is timing: how quickly AI Search revenue converts after the commercial launch in late April 2026.

What is the price target for DOCS stock?

The Street Mean Target for DOCS is $25, based on 20 analysts, with the high target sitting at $42. Both sit above the current price of around $20. TIKR’s independent model puts the mid-case target at $31 by March 2031.

The wide spread between the mean and the high target reflects genuine disagreement about how fast AI Search monetization accelerates through fiscal 2027.

Should You Invest in Doximity, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Doximity, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Doximity, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze DOCS stock on TIKR for Free →