Key Takeaways:

- Revenue Growth: 5-6% annually, driven by banking digital transformation and payments innovation.

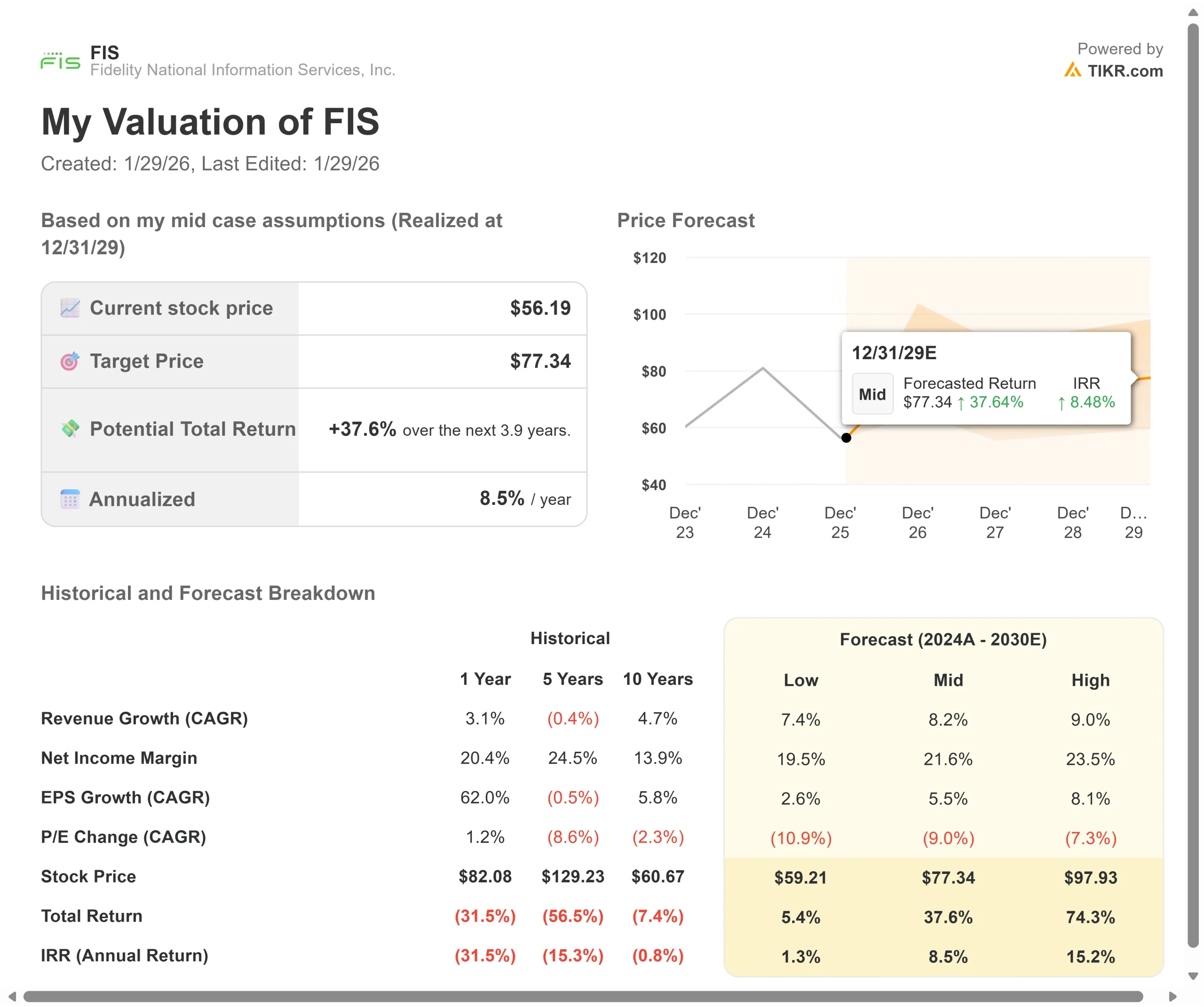

- Price Projection: Based on current execution, FIS stock could reach $65 by December 2027.

- Potential Gains: This target implies a total return of 16% from the current price of $56.

- Annual Return: Investors could see roughly 8% growth over the next 1.9 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Fidelity National Information Services (FIS) just delivered its strongest quarter in years, exceeding its outlook on revenue, EBITDA, and EPS.

The company posted 6.3% revenue growth in Q3, with adjusted EBITDA margins hitting 41.8% and EPS climbing 8% year-over-year.

CEO Stephanie Ferris is executing a Future Forward strategy that’s transforming FIS into a technology powerhouse at the center of financial services innovation.

With AI-powered solutions gaining traction and a pending credit issuer acquisition, FIS is capturing market share while maintaining pricing discipline.

Adjusted free cash flow conversion reached 142% in Q3, enabling management to increase the share repurchase target to $1.3 billion for the year.

The company returned $509 million to shareholders through buybacks and dividends during the quarter alone.

Despite strong execution, FIS stock trades at $56, offering upside for investors who recognize the company’s competitive advantages in banking technology and payments infrastructure.

See analysts’ full growth forecasts and estimates for FIS stock (It’s free) >>>

What the Model Says for Fidelity National Information Services Stock

We analyzed FIS through its transformation from a legacy processor into a modern financial technology leader with comprehensive AI capabilities.

- The company is expanding across high-growth verticals, including digital banking, real-time payments, and cloud-native solutions.

- Management controls over 200 petabytes of data, powering an average of 20+ products per client across the money lifecycle.

- This data advantage becomes exponentially more valuable as AI adoption accelerates.

Using a forecast of 12% annual revenue growth and 16.9% operating margins, our model projects the stock will rise to $65 within 1.9 years. This assumes a 7.8x price-to-earnings multiple.

That represents compression from FIS’s historical P/E averages of 12.1x (one year) and 13.8x (five years).

The lower multiple acknowledges near-term integration costs from recent acquisitions and the competitive dynamics in financial services technology.

The real value lies in executing the banking modernization strategy and leveraging AI to drive operational efficiency across the client base.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for FIS stock:

1. Revenue Growth: 12%

FIS’s growth centers on three strategic priorities: operational excellence, core and digital banking, and payments innovation.

Banking segment revenue grew 6.2% in Q3, well above management’s initial guidance. Recurring revenue expanded 6% with strong transaction growth across payments and digital banking platforms.

The company’s annual contract value in its sales pipeline has increased 13% annually since 2023, demonstrating sustained commercial momentum.

Management expects the recently announced Credit Issuer Solutions acquisition to close in Q1 2026, adding scale in U.S. and international credit processing. This transaction will contribute $500 million of free cash flow in 2026, rising to $700 million post-integration.

Digital banking users have grown by over 30% across FIS platforms. The Money Movement Hub, launched just one quarter ago, has already signed over 40 new clients. NICE network sales more than doubled with pipeline growth of 3x versus last year.

2. Operating margins: 16.9%

FIS is expanding margins while investing aggressively in AI and product innovation.

The company achieved sequential margin improvement of approximately 200 basis points in Q3, driven by strong profitability across both Banking and Capital Markets segments.

Management expects margin expansion of more than 60 basis points in 2026 as recent acquisitions become accretive and cost-optimization programs deliver results.

FIS has deployed AI across the business, from sales-force productivity to client-support automation. The company is helping banks automate back-office operations, improve fraud detection through machine learning, and deliver personalized customer experiences at scale.

3. Exit P/E Multiple: 7.8x

The market currently values FIS at 9.1x earnings. We assume the P/E will compress to 7.8x over our forecast period.

Near-term headwinds from integrating acquisitions and technology investments weigh on the multiple. However, FIS operates in a rational pricing environment with stable net pricing trends providing a consistent tailwind.

As the credit issuer deal closes and AI-powered solutions drive differentiation, FIS should command a premium for its recurring-revenue quality and cash-generation capabilities. The company targets 90% free cash flow conversion in 2026, up from 85% in 2025.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Financial technology companies face competitive pressures and evolving client needs. Here’s how FIS stock might perform under different scenarios through December 2029:

- Low Case: If revenue growth slows to 7.4% and margins compress to 19.5%, investors still see a 5% total return (1.3% annually).

- Mid Case: With 8.2% growth and 21.6% margins, we expect a total return of 38% (8.5% annually).

- High Case: If digital and payments momentum accelerates and FIS maintains 23.5% margins while growing at 9%, returns could hit 74% total (15.2% annually).

See what analysts think about FIS stock right now (Free with TIKR) >>>

The range reflects execution on banking modernization initiatives, success in cross-selling the credit issuer platform, and the ability to monetize AI capabilities.

In the low case, competitive pricing pressures intensify, or bank technology spending slows more than expected.

In the high case, the pending $500 million+ cash flow addition froma credit issuer accelerates margin expansion, AI solutions drive higher retention rates, and bank consolidation creates additional growth opportunities as FIS wins displacement deals.

How Much Upside Does Fidelity National Information Services Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!