Key Takeaways:

- Medicare Advantage Growth: Return to growth expected in 2026 after strategic reset.

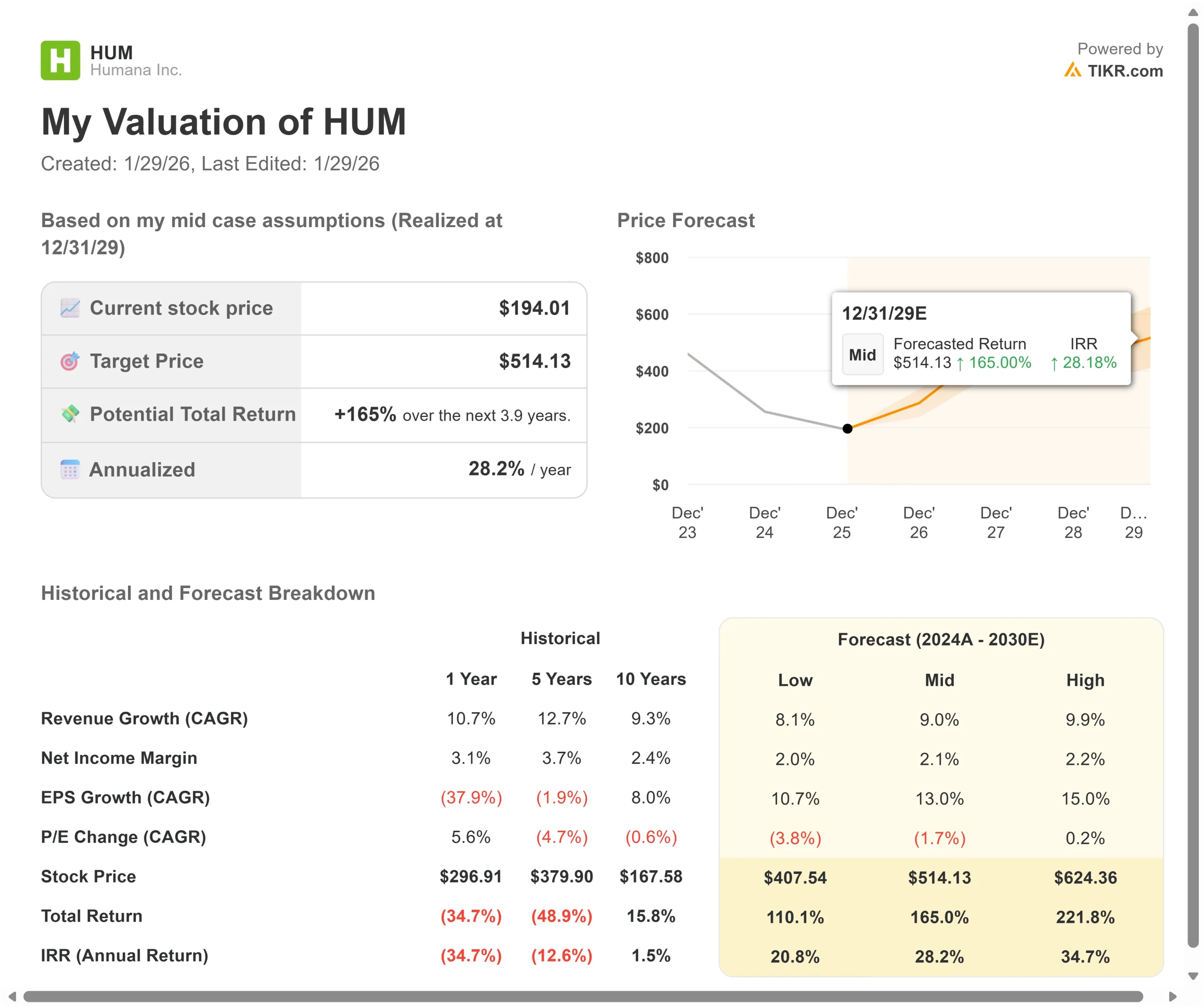

- Price Projection: Based on current execution, HUM stock could reach $317 by December 2027.

- Potential Gains: This target implies a total return of 63.5% from the current price of $194.

- Annual Return: Investors could see roughly 29.1% growth over the next 1.9 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Humana (HUM) is navigating a critical turnaround in its business. After two years of benefit cuts and market exits to stabilize margins, the company is returning to growth while maintaining pricing discipline.

CEO Jim Rechtin is executing a customer lifetime value strategy that prioritizes retention over raw enrollment numbers.

With early Annual Election Period data showing sales at the high end of expectations and improved channel mix, Humana is capturing desirable growth while protecting operational capacity.

The company expects individual MA pretax margins (excluding Stars) to double in 2026 from 2025 levels.

Management is also making meaningful progress on Stars’ recovery, with 600,000 additional gaps closed year over year as operational improvements continue.

Despite near-term Stars headwinds, Humana stock trades at $194, offering significant upside for investors who recognize the company’s improving fundamentals and disciplined growth approach.

See analysts’ full growth forecasts and estimates for HUM stock (It’s free) >>>

What the Model Says for Humana Stock

We analyzed Humana’s transformation from aggressive growth to sustainable profitability in Medicare Advantage.

The company is deconsolidating its oversized H5216 contract, which represents 43-45% of membership, to create a balanced portfolio. Management is shifting members to 4 and 4.5-star contracts while maintaining benefit stability to reduce voluntary attrition.

Early AEP results show a favorable product mix with higher-than-expected sales in 4-star and above plans. Channel mix has meaningfully improved, with greater volume in owned distribution, select high-performing partners, and digital channels that deliver higher lifetime value.

Using a forecast of 9.9% annual revenue growth and 2.5% operating margins, our model projects the stock will rise to $317 within 1.9 years. This assumes a 12.8x price-to-earnings multiple.

That represents compression from Humana’s historical P/E averages of 17.4x (one year) and 18.4x (five years). The lower multiple reflects near-term margin pressure from Stars headwinds, though this should reverse as the company returns to top-quartile Stars performance.

The real value lies in executing the retention strategy and capturing growth in higher-margin products, while transforming operations through AI and outsourcing initiatives that are expected to generate over $100 million in savings.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for HUM stock:

1. Revenue Growth: 9.9%

Humana’s growth centers on returning to membership expansion after strategic resets in 2024 and 2025.

The company is seeing new sales at the high end of anticipated ranges. Management expects significantly reduced plan-to-plan switching, which typically correlates with better retention. This is a key early indicator that the stable benefit strategy is working.

Revenue growth will also benefit from improving member mix as the company shifts toward 4-star contracts and value-based care arrangements. CenterWell Pharmacy is expanding its direct-to-consumer and direct-to-employer offerings, particularly for GLP-1 medications.

2. Operating margins: 2.5%

Humana is rebuilding margins after two years focused on repricing for risk and reducing benefits.

Individual MA pretax margins (excluding Stars) are expected to double in 2026 versus 2025. The company is pricing appropriately for risk across all products rather than relying on low-margin plans that degrade over time.

Management is investing approximately $150 million in incremental funding for Stars, clinical excellence, and network management.

These investments position the company for margin expansion as Stars performance improves and operational efficiencies take hold through AI deployment and finance outsourcing partnerships.

3. Exit P/E Multiple: 12.8x

The market values Humana at 14.5x earnings. We assume the P/E will compress to 12.8x over our forecast period.

Near-term Stars headwinds create uncertainty. Bonus Year ’27 results were disappointing, though consistent with expectations. However, Bonus Year ’28 shows meaningful year-over-year improvement across most metrics.

As Stars’ performance returns to the top quartile and margins expand through operational transformation, Humana should command a higher multiple.

The company’s dual-eligible focus in Medicaid provides outsized margins, and management has demonstrated pricing discipline in the current environment.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Healthcare stocks face regulatory changes and competitive pressures. Here’s how Humana stock might perform under different scenarios through December 2029:

- Low Case: If revenue growth slows to 8.1% and margins stay at 2.0%, investors still see a 110.1% total return (20.8% annually).

- Mid Case: With 9.0% growth and 2.1% margins, we expect a total return of 165.0% (28.2% annually).

- High Case: If AEP momentum accelerates and Humana achieves 2.2% margins while growing at 9.9%, total returns could reach 221.8% (34.7% annually).

See what analysts think about HUM stock right now (Free with TIKR) >>>

The range reflects execution on retention targets, success in Stars recovery, and the pace of margin expansion.

In the low case, new member growth strains operations, or Stars’ improvement stalls.

In the high case, stable benefits drive industry-leading retention, Stars returns to the top quartile by Bonus Year ’28, and operational transformation delivers ahead of expectations.

How Much Upside Does Humana Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!