Key Stats for Danaher Stock

- Past-Week Performance: -1.5%

- 52-Week Range: $171 to $242.8

- Current Price: $209.5

What Happened?

Danaher‘s $9.9 billion acquisition of Masimo has repositioned the life sciences giant toward patient monitoring, but the market’s immediate verdict was swift punishment, sending DHR shares down roughly 3% to $206 on February 17 as investors questioned whether the deal represents a strategic pivot or an admission that core biotech growth remains constrained.

The flashpoint arrived when J.P. Morgan analysts flagged the acquisition as “unexpected,” warning that the shift toward patient-monitoring equipment could pressure shares in the near term, signaling that institutional gatekeepers had not anticipated Danaher straying this far from its life sciences and diagnostics core.

Driving the deal’s logic is Masimo’s commanding position in pulse oximetry, its strong recurring-revenue base, and a projected $125 million in combined cost synergies, with Danaher expecting a $0.2 EPS boost in the first full year after close and approximately $0.7 in year five.

Also, beyond the near-term skepticism, the market is beginning to re-rate Danaher from a pure-play life sciences compounder into a diversified medtech platform, with the Masimo deal broadening its Diagnostics segment by pairing invasive Radiometer blood analyzers with Masimo’s non-invasive pulse oximeters and brain function monitoring devices.

President and CEO Rainer Blair stated on the Q4 earnings call that “the combination of our differentiated portfolio, the power of the Danaher Business System and the strength of our balance sheet positions Danaher for long-term value creation as we move into 2026 and beyond,” contextualizing remarks delivered just weeks before the company’s largest acquisition since its $5.7 billion Abcam deal in 2023.

Adding further institutional conviction, Third Point raised its Danaher stake nearly 12x, from 50,000 to 600,000 shares as of December 31, while Bernstein analyst Christian Moore separately expressed confidence that the Masimo acquisition would prove to be a strong long-term move for Danaher.

Looking three to five years out, Danaher’s entry into patient monitoring signals a deliberate build toward a full-spectrum diagnostics and care-delivery ecosystem, and if Masimo’s projected revenue growth of up to 10% materializes alongside a normalizing bioprocessing cycle, Danaher’s trading multiple of 19x forward EBITDA could prove deeply conservative relative to where the business is ultimately headed.

Wall Street’s Take on DHR Stock

The $9.9 billion Masimo acquisition reshapes Danaher’s Diagnostics segment and gives the company a recurring-revenue anchor in patient monitoring precisely as its bioprocessing recovery gains traction, shifting the forward earnings story from stabilization to genuine multi-front acceleration.

Underpinning that acceleration, Danaher’s revenue grew 2.9% in 2025 and analysts project 4.4% growth in 2026, while normalized EPS climbs from $7.8 to an estimated $8.4, a 7.8% jump that reflects both operational leverage and the $0.2 first-year EPS contribution Masimo is expected to deliver.

Wall Street stands firmly behind the name with 18 buys, 4 outperforms, and just 3 holds against zero sells, converging on a mean price target of $264.9 that implies 26.4% upside from the current $209.5, with analysts holding conviction through the deal-driven pullback rather than fading their targets.

The spread between the $220.0 low target and $310.0 high target reflects a genuine fork in the road, where the bear scenario prices in deal integration risk and multiple compression while the bull case demands successful Masimo execution plus a full bioprocessing equipment recovery materializing faster than the current flat guidance implies.

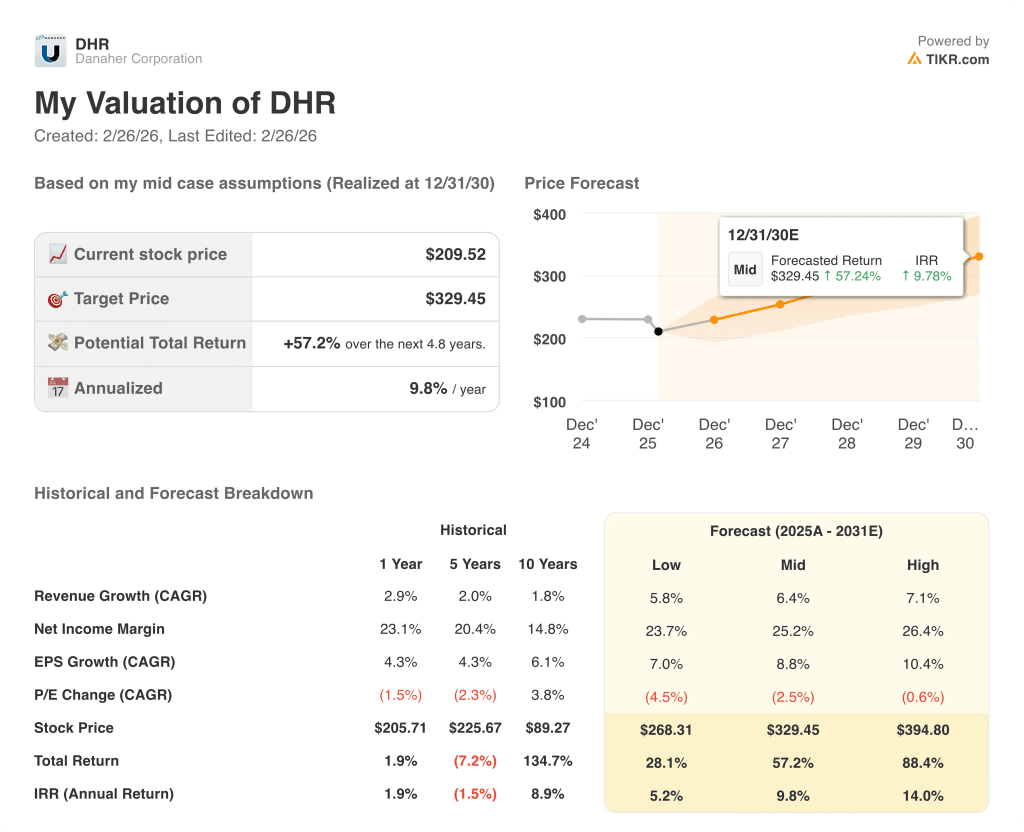

What Does the Valuation Model Say?

Given Danaher’s post-acquisition repositioning and its bioprocessing high single-digit growth outlook, a mid-case valuation model prices DHR at $329.5, implying a 57.2% total return over 4.8 years at a 9.8% annualized IRR, a return profile that looks credible if integration synergies and the biologics supercycle both deliver as expected.

The most consequential near-term risk sits in Danaher’s Life Sciences segment, where operating profit already collapsed 57.0% in 2025 to $520 million, and any further deterioration in academic funding, biotech spending, or China demand could neutralize the bioprocessing gains and compress the margin expansion baked into the $8.4 EPS estimate.

At $209.5, Danaher trades at a discount to its mean analyst target and well below the mid-case model value, making it look undervalued for patient investors, provided management executes the Masimo integration cleanly and the bioprocessing equipment recovery confirmed by three consecutive quarters of sequential order growth finally translates into full-year revenue in 2026.

Should You Invest in Danaher Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up DHR stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Danaher Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze DHR stock on TIKR for Free →