Key Stats for Comfort Systems Stock

- Past-Week Performance: +2.3%

- 52-Week Range: $276.4 to $1,500

- Current Price: $1,430.4

What Happened?

Comfort Systems USA (FIX) crossed into territory no MEP contractor has ever occupied, posting a 25.5% gross margin in Q4 2025 — the first quarter in company history to breach 25% — while its $11.9 billion backlog sits nearly double where it stood a year ago, trading at $1,430.38.

On February 19, CEO Brian Lane attributed the quarter’s results to unprecedented demand, with Q4 revenue of $2.65 billion crushing the $2.34 billion consensus estimate as diluted EPS of $9.37 beat the $6.76 Wall Street forecast by 39%.

The engine behind the beat is a backlog that grew 99.3% year over year, driven by a $2.4 billion sequential surge in Q4 alone, with technology customers including data centers now representing 45% of revenue, up from 33% in 2024.

Meanwhile, the board raised its quarterly dividend to $0.70 per share on February 19, payable March 17 to shareholders of record March 6, marking two consecutive $0.10 increases that together represent nearly a 50% lift to the payout.

CFO William George stated on the Q4 2025 earnings call that “by the time we are booking backlog and especially by the time we’re booking revenue, we’re really working on things that came up 1 to 2.5 years ago,” anchoring the current $12 billion backlog to hyperscaler commitments made well before today’s CapEx surge.

With modular capacity expanding from 3 million to 4 million square feet by end of 2026 and same-store revenue growth guided at mid-to-high teens, Comfort Systems is structurally positioned as the dominant late-cycle beneficiary of a data center construction wave that, by its own math, won’t fully hit revenue until 2027 and 2028.

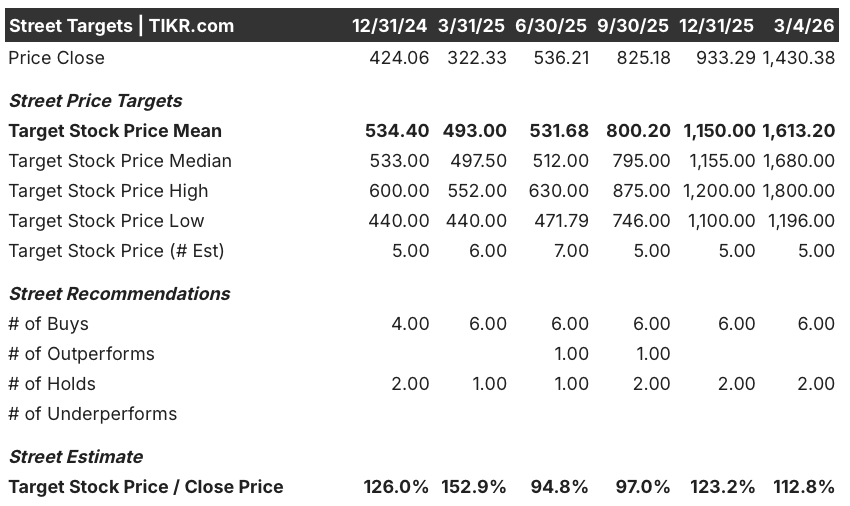

Wall Street’s Take on FIX Stock

The record $11.9 billion backlog, nearly double year-ago levels, forces analysts to reconsider FIX not as a cyclical contractor but as a structurally compounding infrastructure platform riding a multi-year data center construction supercycle.

Consensus estimates project FY 2026 revenue of $10.95 billion (+20.3% YoY) and EPS of $36.76 (+27.3%), with EBITDA margins expanding to 16.8% from an already historic 16.0% in 2025, confirming the growth direction is operationally intact.

Six analysts rate FIX a Buy and two rate it a Hold, with a mean price target of $1,613.20 implying 12.8% upside from the March 4 close of $1,430.38, as analysts await sustained margin delivery above 25% gross profit before upgrading.

The Street’s high target of $1,800 anchors to continued hyperscaler CapEx acceleration and modular capacity expansion to 4 million square feet, while the low target of $1,196 reflects risk from labor cost inflation and a potential slowdown in technology customer bookings.

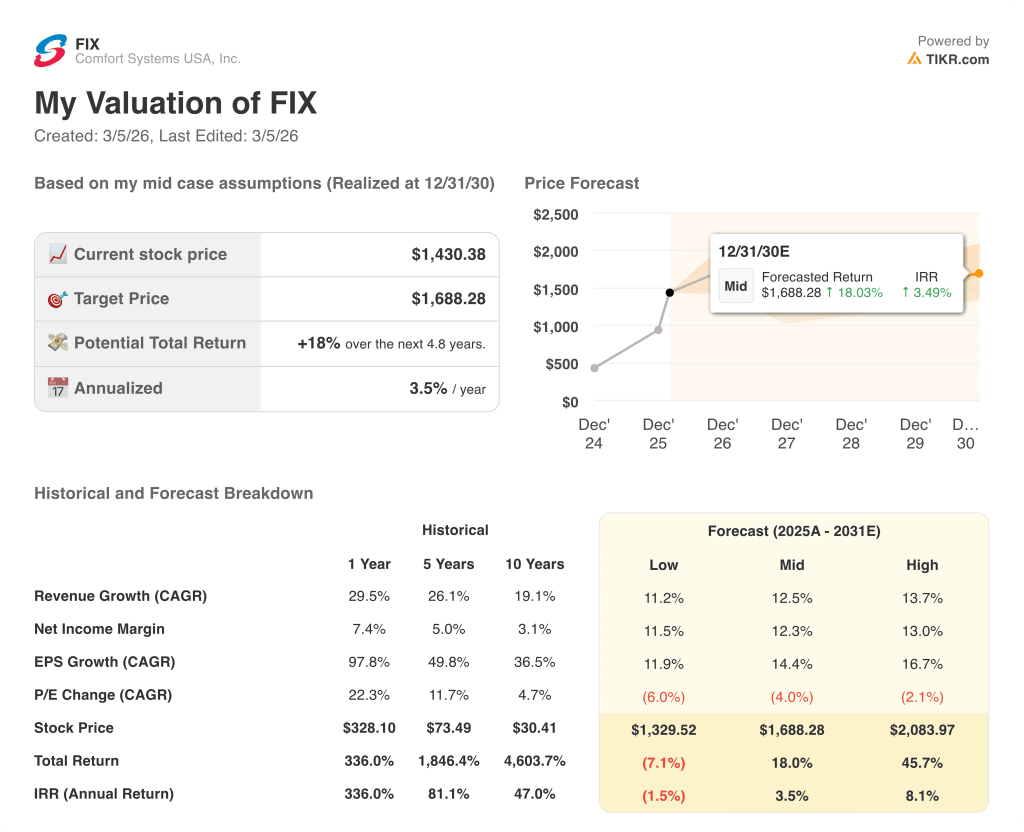

What Does the Valuation Model Say?

The TIKR mid-case valuation model prices FIX at $1,688.28 by December 2030, implying an 18% total return and an annualized IRR of just 3.5% from current levels.

The market is pricing FIX as if its backlog duration is a liability rather than a visibility asset, ignoring that booked revenue extends meaningfully into 2027 and 2028.

The 10-year EPS CAGR of 36.5% versus a current NTM P/E of 43x reveals the market is paying a growth premium well below what the decade-long compounding record historically justified.

Management’s two consecutive $0.10 dividend increases, totaling nearly a 50% payout lift, and $217.9 million in share repurchases during 2025 signal that leadership sees the current price as undervaluing durable cash generation.

A 2026 tax rate rising to approximately 23% from 20.9% in 2025 directly compresses net income margins, threatening the EPS trajectory if revenue growth decelerates even modestly from guided mid-to-high teens.

The March 17 dividend payment to shareholders of record March 6 represents the near-term confirmation date, with the next earnings call serving as the primary reset point for 2026 same-store growth execution.

FIX earns a conviction Hold at current levels: the backlog and margin story is real, but the 3.5% annualized IRR to fair value demands patience over urgency.

Should You Invest in Comfort Systems USA, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up FIX stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Comfort Systems USA, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze FIX stock on TIKR for Free →