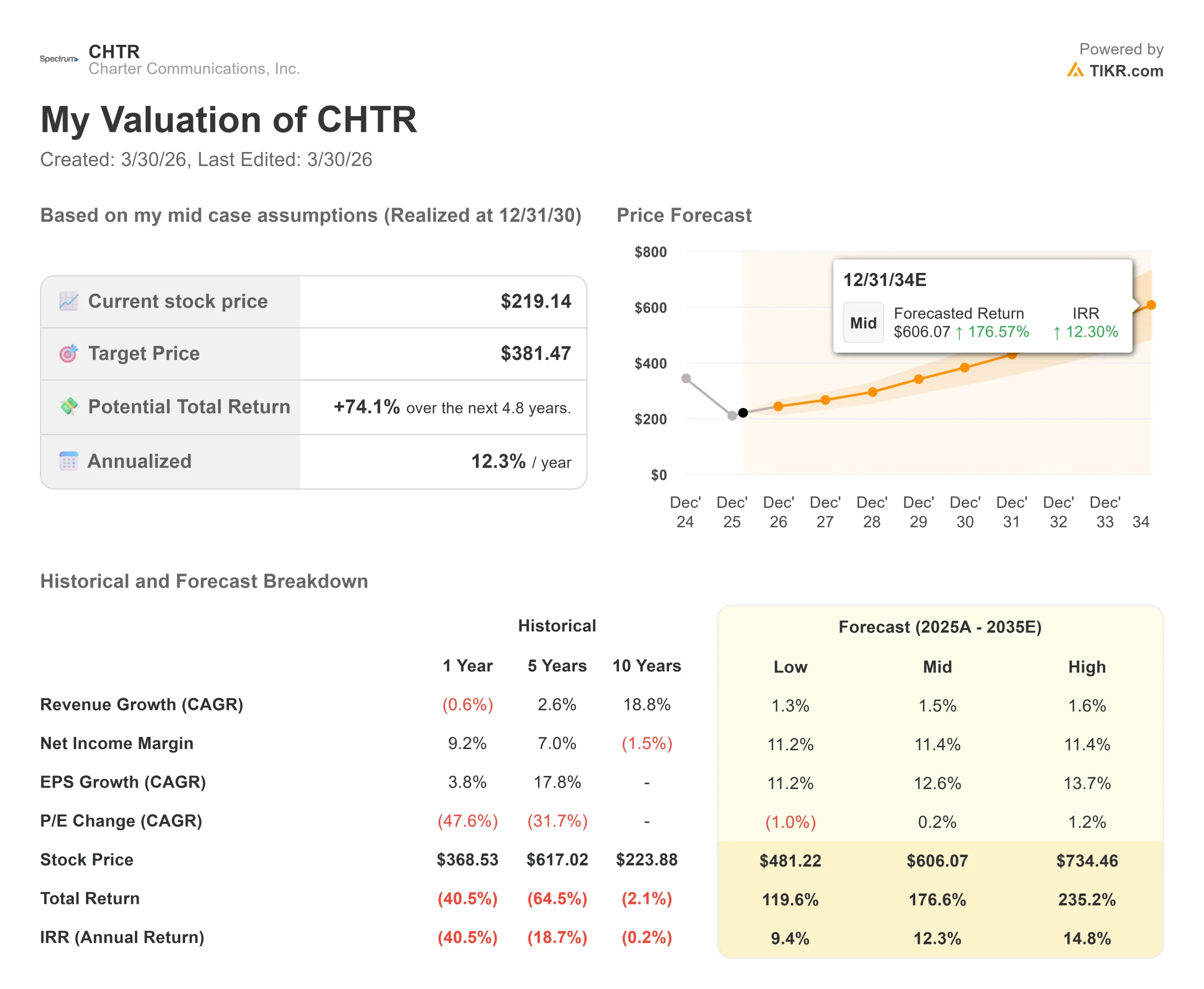

Key Stats for Charter Communications Stock

- Current Price: $219.14

- Target Price (Mid): $381.47

- Street Target: $276.80

- Potential Total Return: +74.1%

- Annualized IRR: 12.30% / year

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Charter Communications (CHTR) stock is down roughly 50% from its 52-week high of $437.06, and the market is split on what it means. Bulls argue the stock is priced for a permanent decline, but the underlying network and free cash flow trajectory do not support it.

Bears point to four straight quarters of broadband subscriber losses and a competitive market that keeps getting harder.

The unresolved question is whether Charter can actually get broadband back to growth, or whether fiber and fixed wireless have claimed that ground permanently.

On February 27, 2026, the FCC approved Charter’s $34.5 billion acquisition of Cox Enterprises, clearing the last major federal hurdle.

California’s Public Utilities Commission remains the only outstanding state approval, with Charter pushing for a final decision no later than July 16 to support a mid-year close.

When Q4 2025 results landed on January 30, the stock rose 7.33% in pre-market trading as broadband losses narrowed more than expected and the company posted a rare gain in video subscribers.

Speaking at the NSR/BCG Global Connectivity Leaders Conference in New York on March 26, CFO Jessica Fischer was direct: “Our number one priority is getting broadband back to growth.” She acknowledged a competitive market but laid out the specific tools Charter is deploying to push back.

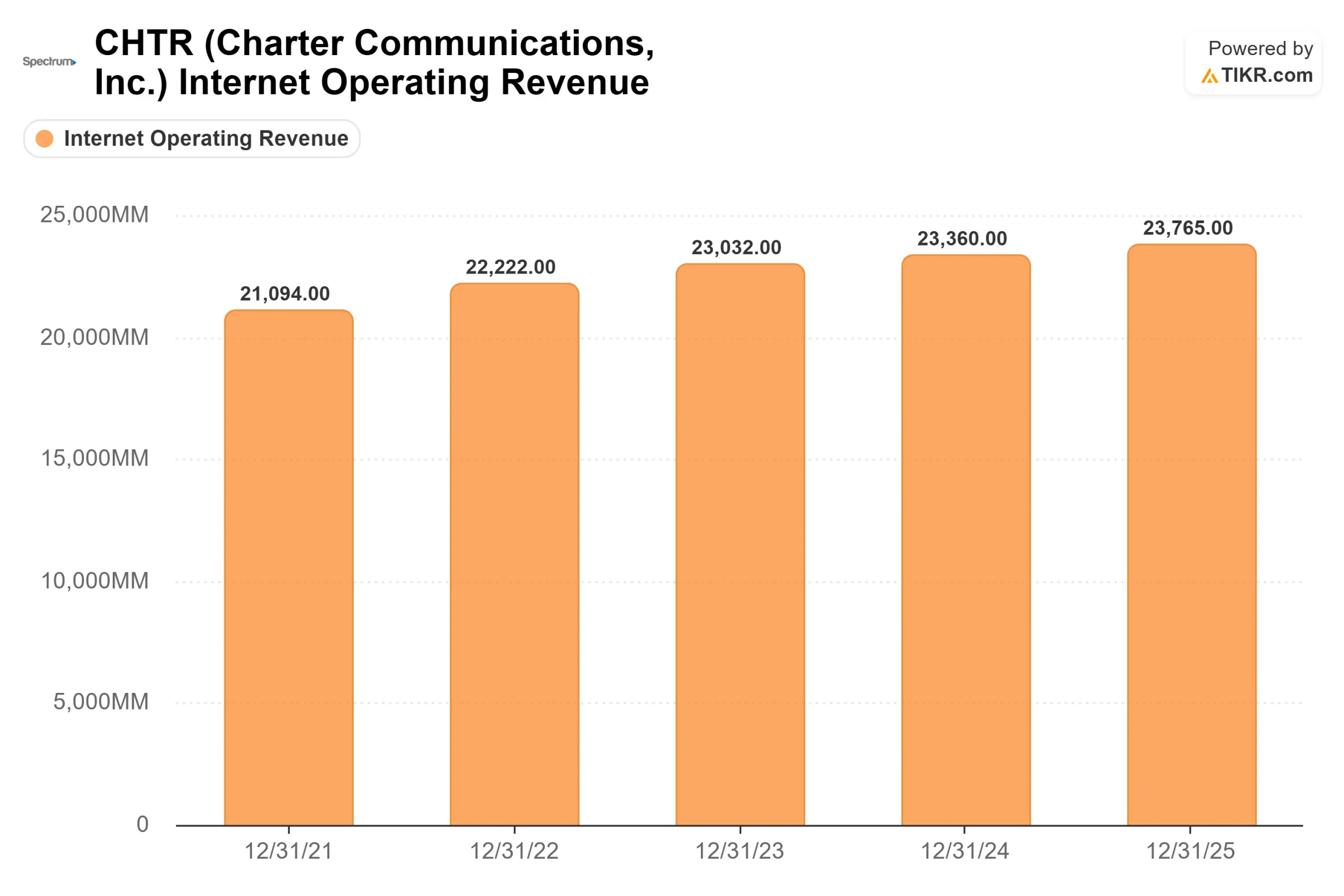

Charter lost 119,000 internet customers in Q4 2025, an improvement from 177,000 lost in Q4 2024. Full-year 2025 revenue of $54.8 billion declined 0.6% year over year, and Q4 adjusted EBITDA of $5.7 billion fell 1.2% year over year.

The numbers are still negative. But the rate of deterioration is slowing, which is the inflection point on which the investment case depends.

See historical and forward estimates for Charter Communications stock (It’s free!) >>>

Is Charter Communications Undervalued Today?

The valuation case rests on cost structure and free cash flow inflection, not revenue growth.

That CapEx story is what Fischer spent the most time on at the March 26 conference.

Charter has run above its long-run spending rate for four years because of two specific programs: a rural expansion initiative and a network evolution project upgrading its cable infrastructure to DOCSIS 4.0, the standard enabling multi-gigabit speeds over existing lines.

The expansion initiative finishes this year.

The network evolution project is substantially complete by the end of 2027. “Just pulling that capital out of the plan is enough to get us back to that run rate below $8 billion,” Fischer said, referring to CapEx guidance for 2028 and beyond.

That directly converts to free cash flow.

On competition, Fischer said the pressure from fixed wireless “is not significantly different from where it’s been previously,” and on Starlink: “There’s not a discernible impact from Starlink on trends right now.”

She acknowledged fiber competitors continue to gain ground in mature markets, but argued Charter retains a higher market share in those markets because of its converged product, its scale, and its video offering.

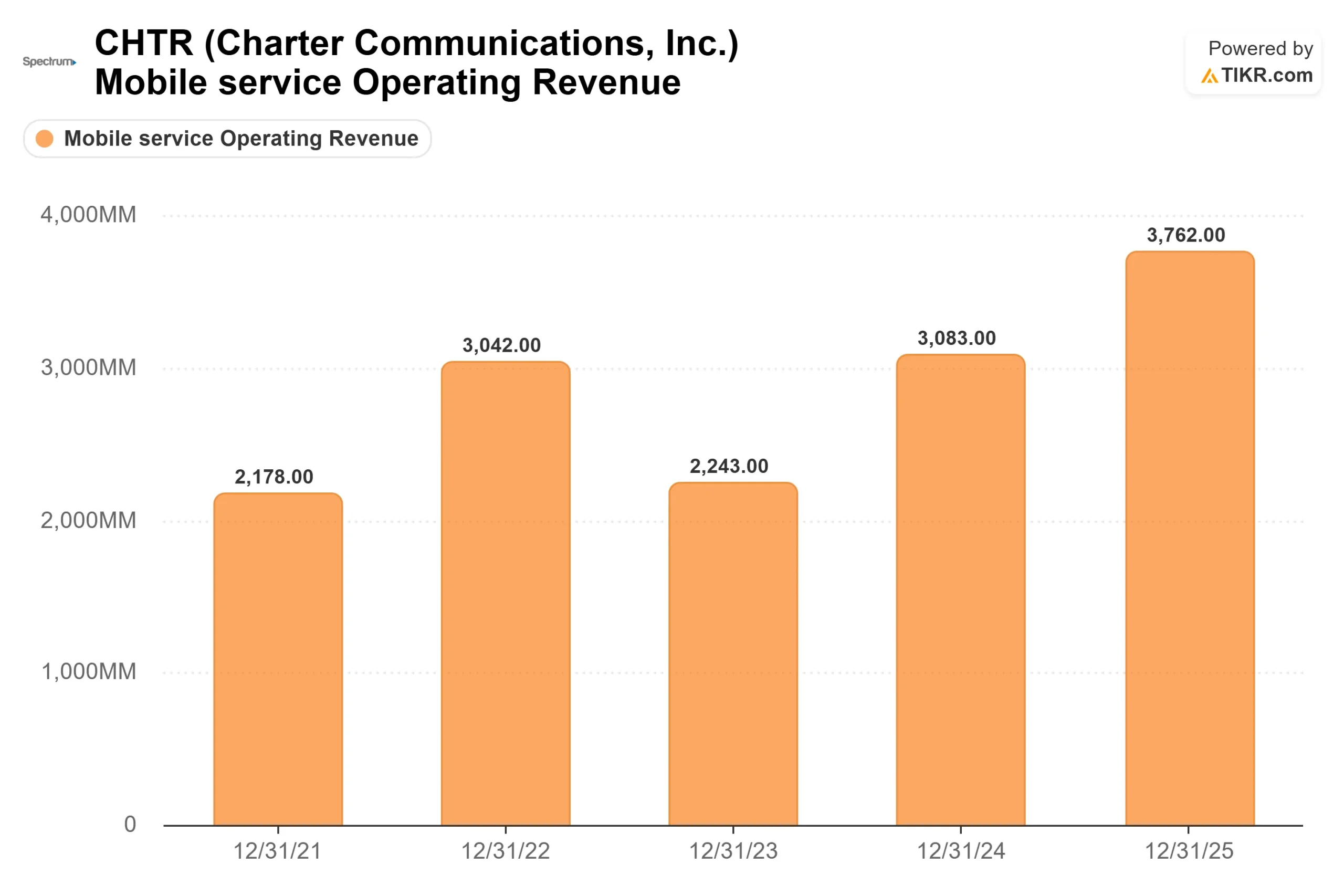

Mobile lines grew by 428,000 in Q4 2025, and residential connectivity revenue rose 2.3% year over year despite the broadband customer losses.

Fischer confirmed that Charter’s WiFi and CBRS network now delivers 88% of the data to mobile phones on its network, operating largely on owned infrastructure rather than pure carrier resale.

Mobile service margin, excluding subscriber acquisition costs, reached 34% in Q3 2025, and Fischer said she “fully expects” meaningful growth in that margin for several more years as scale builds.

The Cox deal, at $34.5 billion, would create the largest cable and broadband provider in the country with approximately 38 million subscribers, surpassing Comcast.

Fischer’s pitch on Cox was specific: its mobile and video penetration are both very low, meaning Charter can apply its Spectrum pricing and packaging to a new customer base immediately.

She also flagged Cox’s B2B assets, including its Segra commercial fiber platform and RapidScale managed IT business, as capabilities that Charter can extend across its existing 41-state footprint.

The primary risk is California. The CPUC has indicated it could hold hearings in April, with a statutory deadline running to the end of January 2027.

A delay past mid-2026 pushes back synergy realization and slows the free cash flow inflection the model depends on.

See how Charter Communications performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $219.14

- Target Price (Mid): $381.47

- Potential Total Return: +74.1%

- Annualized IRR: 12.30% / year

See analysts’ growth forecasts and price targets for Charter Communications stock (It’s free!) >>>

The TIKR mid-case targets $381.47 by December 31, 2030, implying a 74.1% total return at a 12.30% annualized IRR. The mid-case revenue CAGR of 1.5% is conservative, which is the honest construction: the model does not require a broadband subscriber recovery to generate strong returns.

Two revenue drivers support that path. First, mobile service revenue is growing fast and increasingly offsets broadband compression. Second, broadband ARPU is being driven higher through three levers Fischer named at the March 26 conference: upselling customers to gigabit and 2-gigabit tiers as network evolution expands, attaching value-added services like Invincible WiFi (Charter’s product combining WiFi 7 with 5G backup), and driving multi-product bundling that improves both retention and revenue per household.

The margin driver is CapEx normalization. When network evolution finishes in 2027, and CapEx returns below $8 billion, free cash flow expands and flows directly to EPS, which the model projects at a 12.6% CAGR through the forecast period. That is how a low-revenue-growth cable company generates a 74% total return.

The key downside: if California delays the Cox close into 2027, the FCF inflection is slower. If broadband losses fail to stabilize, ARPU growth faces additional compression. In that scenario, the low-case IRR drops to 9.40% per year.

Conclusion: Watch the Q1 2026 earnings report on April 24. The metric that matters is residential broadband net additions. If Charter’s Life Unlimited packaging, Invincible WiFi attach rates, and gigabit upsell are showing up in narrowing losses, the case becomes easier to hold. Fischer’s March 26 remarks suggest management believes they have the tools. Q1 delivers the first data point.

At $219.14, Charter is priced as if EBITDA declines indefinitely, on a network that is more than 99% fiber to the node, with a fast-growing mobile business, a transformative acquisition pending, and a CapEx cycle two years from normalization. The TIKR mid-case says that the combination is worth $381.47 by December 31, 2030.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Charter Communications?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Charter Communications, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Charter Communications alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Charter Communications on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!