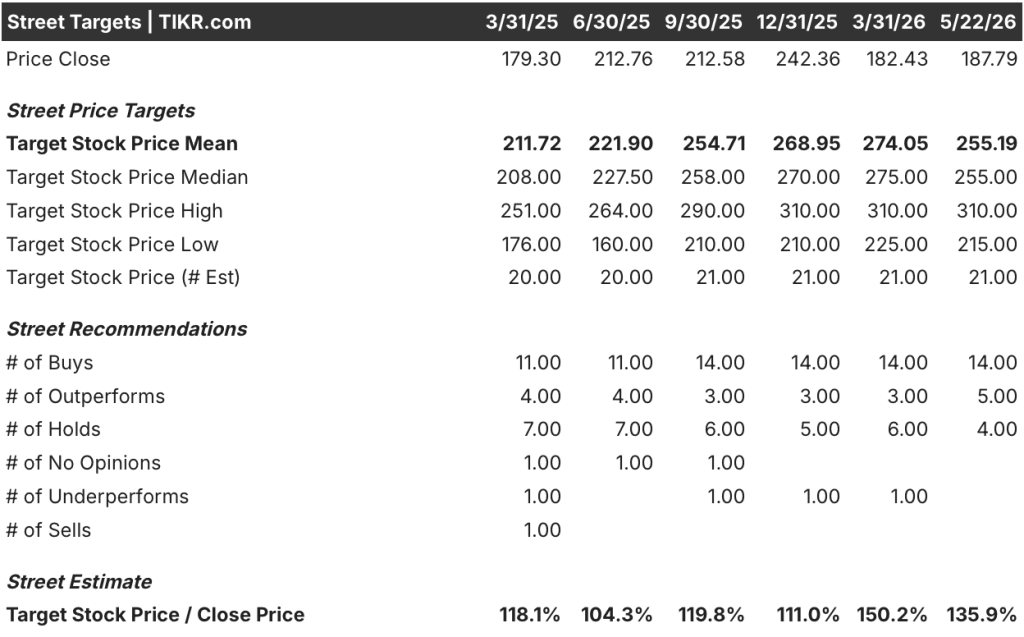

Key Stats for Capital One Stock

- 52-Week Range: $175 to $260

- Current Price: $188

- Street Mean Target: $255

- Street High Target: $310

- Analyst Consensus: 14 Buys / 5 Outperforms / 4 Holds

- TIKR Model Target (Dec. 2030): $315

Capital One Missed Q1 Estimates, But the Credit Story Investors Fear Is Actually Improving

Capital One Financial (COF), the sixth-largest U.S. bank by assets and one of the country’s largest credit card lenders, reported Q1 2026 adjusted EPS of $4.42 against a Wall Street estimate of $4.57, sending shares down roughly 3% in after-hours trading after its April 21 results.

The miss came from a provision for credit losses of $4.07 billion, ahead of the $3.77 billion analysts had expected.

But provisions and credit quality are two different things, and the actual credit results came in better than feared.

The domestic card charge-off rate for Q1 came in at 5.1%, an improvement of 109 basis points year over year, and the delinquency rate of 3.7% was down 55 basis points from the same quarter a year ago.

CEO Richard Fairbank was direct about the macro backdrop on the Q1 2026 earnings call: “The U.S. consumer remained healthy and the overall economy remained resilient through the first quarter.”

Revenue of $15.23 billion rose 52% year over year, driven primarily by the May 2025 acquisition of Discover Financial Services, which added billions in loans, deposits, and a proprietary global payments network to Capital One’s balance sheet.

Excluding Discover, legacy Capital One card revenue grew approximately 7% year over year, which reflects the pace of the underlying franchise before deal math is applied.

The Discover integration is progressing on schedule, with the full conversion of Capital One debit customers onto the Discover network completed in Q1, unlocking the first wave of the $2.5 billion in total synergies expected by mid-2027.

In April, Capital One also closed its $4.5 billion acquisition of Brex, the corporate card and expense platform, adding a fast-growing commercial fintech business to a credit card empire that now spans consumer, small business, and enterprise segments.

The NIM declined 39 basis points sequentially to 7.87%, but the CFO attributed the bulk of that to seasonal factors: two fewer days in the quarter accounted for 18 basis points alone, and elevated cash from strong deposit growth compressed yield further.

Net interest income still came in at $12.15 billion for the quarter, up 52% from $8 billion a year ago.

COF Stock Trades at a 12% Discount to Its Own Historical P/E While Synergies Are Just Getting Started

Wall Street’s view on Capital One stock has not meaningfully deteriorated despite the Q1 miss.

The analyst breakdown as of May 2026 stands at 14 Buys, 5 Outperforms, and 4 Holds, with no Sells and no Underperforms.

The Street mean target for Capital One stock is around $255, implying roughly 36% upside from the current price of around $188.

The highest target on the Street sits at around $310, representing a premium of around 65% to where COF stock trades today.

Truist Securities, which maintained a Buy after the Q1 miss, said the margin shortfall was temporary and that the consumer remained in good shape, though it noted that expense guidance remained open-ended heading into the back half of the year.

KBW, also keeping an Outperform rating, framed the situation directly: Capital One is carrying excess capital, increasing investment, and absorbing integration costs simultaneously, all of which are near-term headwinds that do not change the long-term earnings case.

Adjusted EPS for Q1 came in at $4.42, up 9% from $4.06 in the same quarter a year ago, which means the underlying business is growing earnings even as the company absorbs Discover integration expenses of $415 million in the quarter.

The metric that makes COF stock look most interesting right now is the NTM P/E multiple sitting at 9.13x against a historical mean of 10.40x, a 12% discount to its own average.

COF was trading near 12x forward earnings as recently as early 2026, just before the Q1 miss reset sentiment.

Capital One stock is undervalued relative to its own history: a company absorbing two transformational deals, showing actual credit improvement, and sitting on $76 billion in cash is not a 9x earnings story, and the Street’s distribution of 19 Buy-or-better ratings to 4 Holds says the same thing.

The catalyst to watch is the Discover back-book conversion, currently planned for late 2026 through Q1 2027, which is when the expense synergies begin to dominate the integration cost line.

Is Capital One Stock Undervalued in 2026? TIKR’s $315 Mid-Case Puts the Integration Discount in Numbers

TIKR’s mid-case model values Capital One stock at around $315 by December 2030, implying around 68% total return from the current price of around $188, or roughly 12% annualized over the next 4 and a half years.

If revenue grows at around 5% annually through 2035 and net income margins compress slightly to around 21%, the low case produces a stock price of around $323 and a 6% annualized return from here.

If revenue growth runs closer to 6% and margins hold near 21%, the mid-case reaches around $377 by December 2034, an 8% annualized IRR.

In the high case, with roughly 6% revenue growth and a less severe multiple compression path, the model reaches around $423 and a 10% IRR. The spread across scenarios is tight enough to make COF stock look like a durable compounder regardless of which path materializes, not a binary bet.

The single variable with the most weight is the timing and scale of Discover integration synergies, which management confirmed remain on track to deliver the full $2.5 billion by mid-2027.

Is Capital One stock a buy right now?

Capital One stock carries 14 Buy ratings and 5 Outperform ratings from the 23 analysts covering it, with no Sells and no Underperforms.

The Street mean target of around $255 implies roughly 36% upside from the current price of around $188.

The stock is trading at 9.13x NTM earnings, a 12% discount to its historical mean multiple of 10.40x, while Discover integration synergies are still in early stages.

The key variable to watch is the back-book conversion timeline, which is expected to close out in early 2027.

What is the price target for COF stock?

The Wall Street mean target for COF stock is around $255, with the highest analyst target at around $310. TIKR’s mid-case model shows a target of around $315 by December 2030, implying roughly 68% total return from today’s price.

The Street’s target range runs from a low of around $215 to a high of around $310 across 23 analysts.

Should You Invest in Capital One Financial Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Capital One Financial Corporation stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Capital One Financial Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze COF stock on TIKR for Free →