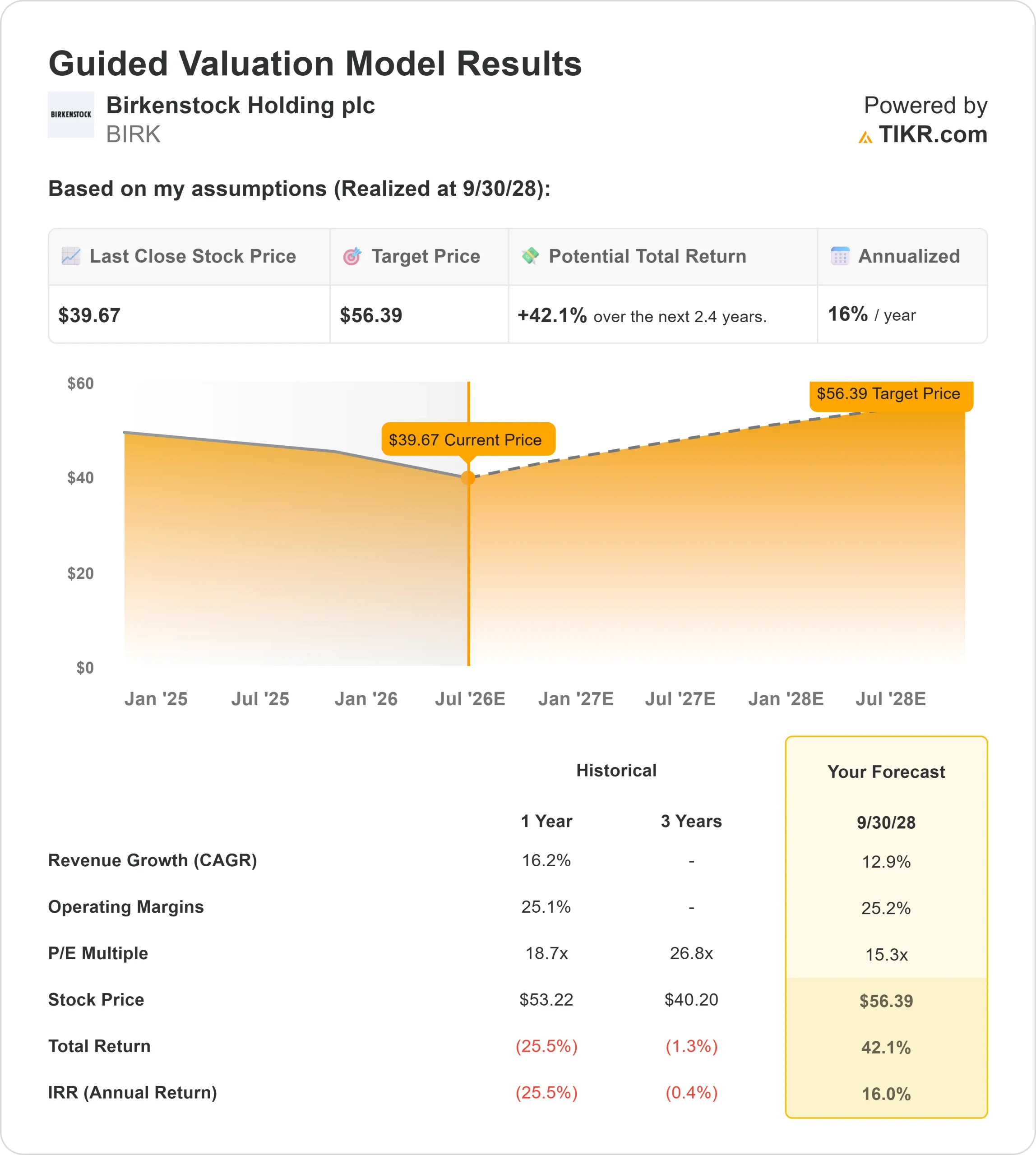

Key Stats for BIRK Stock

- Past-Week Performance: 33%

- 52-Week Range: $31 to $57

- Valuation Model Target Price: around $56

- Implied Upside: 42%

Analyze your favorite stocks like Birkenstock Holding with TIKR (It’s free) >>>

What Happened?

Birkenstock Holding plc stock rose about 33% this week, recently trading near $42 per share as investors reassessed the stock after a sharp post-earnings selloff. The market had been worried that tariffs, currency pressure, softer EMEA demand, and weaker margins were starting to pressure the premium footwear company’s growth story, especially as investors compared Birkenstock’s full-price brand strength with footwear peers such as Crocs, Deckers’ HOKA brand, Nike, and Adidas.

The stock moved higher because Birkenstock’s $250 million accelerated share repurchase directly addressed the market’s biggest question this week: whether the selloff had gone too far.

The company entered the agreement with Goldman Sachs and expects to receive about 6 million shares initially, representing about 80% of the shares covered by the agreement, based on the $33 closing price on May 20. That timing mattered because the stock had just fallen after Q2 margin pressure and an unchanged 2026 outlook, so the buyback gave investors a clear signal that management saw value in the shares.

The recent Q2 earnings call showed Birkenstock delivered revenue of €618 million, up 8% reported and 14% in constant currency, while adjusted EBITDA margin held at 32.1% despite FX and tariff pressure.

CEO Oliver Reichert said “demand for Birkenstock remains strong,” supported by 14% constant-currency growth in the Americas, 30% growth in APAC, over 60% growth in owned retail, double-digit same-store sales growth, and closed-toe penetration rising 300 basis points. Management also reiterated fiscal 2026 guidance for 13% to 15% constant-currency revenue growth, adjusted EBITDA of at least €700 million, and an adjusted EBITDA margin of 30% to 30.5%.

Analyst and institutional updates added more context to the rebound. Deutsche Bank lowered its target to $41 from $48, Piper Sandler cut its target to $50 from $55, Morgan Stanley lowered its target to $41 from $47, and BTIG reduced its target to $60 from $65, showing Wall Street remained cautious on near-term margins even as the stock bounced.

Recent institutional filings were mixed but still showed interest in the stock, as Summerhill Capital opened a new 95,436-share position worth about $4 million, Swedbank raised its stake by 25% to 1.5 million shares, and Goldman Sachs increased its position to about 1.1 million shares, while Kornitzer Capital and Renaissance Capital trimmed exposure after the margin reset.

Value Birkenstock Holding instantly (Free with TIKR) >>>

Is BIRK Undervalued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth: around 13%

- Operating Margins: around 25%

- Exit P/E Multiple: 15x

Birkenstock appears undervalued based on the valuation model, but this is not a simple cheap-stock setup because the market is still deciding whether the company deserves a premium brand multiple or a more standard footwear multiple.

The revenue growth assumption depends on Birkenstock continuing to expand globally through new stores, strong wholesale demand, rising APAC sales, and broader adoption of closed-toe products beyond its classic sandals and clogs.

That matters because Birkenstock is no longer just a warm-weather sandal story. Closed-toe products such as clogs and shoes help the company sell across more seasons, while APAC growth and owned retail expansion give the brand more control over pricing, customer experience, and margins.

See analysts’ growth forecasts and price targets for Birkenstock Holding (It’s free) >>>

Margins remain the biggest swing factor because Birkenstock still benefits from full-price selling and disciplined distribution, but tariffs, currency pressure, German manufacturing costs, and channel mix can limit earnings growth if sales momentum slows.

Compared with Crocs, Deckers’ HOKA brand, Nike, and Adidas, Birkenstock’s edge is not constant product turnover. Its edge is heritage, scarcity, comfort-driven demand, and strong full-price selling, which makes durable pricing power the key proof point for whether the stock can hold a premium multiple.

At current levels, Birkenstock looks undervalued, with the stock’s next move likely driven by full-price demand, APAC growth, store expansion, closed-toe adoption, tariff mitigation, and proof that management can keep margins near premium-footwear levels while scaling the business.

How Much Upside Does BIRK Stock Have From Here?

Investors can estimate Birkenstock Holding’s potential share price, or what any stock could be worth, in under a minute using TIKR’s New Valuation Model tool.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

Value Birkenstock Holding in under 60 seconds with TIKR (It’s free) >>>