Key Stats for Automatic Data Processing Stock

- Past-Week Performance: -3.6%

- 52-Week Range: $198.6 to $329.9

- Current Price: $205.5

What Happened?

Automatic Data Processing (ADP), the world’s largest human capital management company processing payroll for over 42 million employees globally, delivered a record client satisfaction quarter while raising its full-year adjusted EPS growth outlook to 9%–10%, even as shares trade near their 52-week low of $198.59.

ADP’s Q2 FY2026 earnings, reported January 28, produced adjusted EPS of $2.62 against the IBES estimate of $2.57, with 6% revenue growth and 80 basis points of adjusted EBIT margin expansion beating internal expectations across all three metrics.

Underneath the headline beat, ADP’s enterprise HCM platform Lyric, which handles payroll, HR, and workforce management for large organizations and competes directly against Workday, posted new business bookings above expectations for the second consecutive quarter, with more than 70% of wins coming from companies that had never used ADP before.

Maria Black, President and CEO, stated on the Q2 FY2026 earnings call that “Lyric’s new business bookings once again exceeded our expectations in the second quarter, and its new business pipeline continued to expand at a rapid pace,” directly underpinning the board’s decision to authorize a new $6 billion share repurchase program, replacing the prior $5 billion authorization.

ADP’s combination of a $6 billion buyback, a 10% dividend increase, the April 29 Q3 earnings release as the next catalyst, and accelerating enterprise wins through Lyric positions the company to compound shareholder returns even as pays-per-control growth remains near flat and the stock sits 38% below its 52-week high.

Wall Street’s Take on ADP Stock

The raised FY2026 EPS growth guidance to 9%–10%, driven by Lyric enterprise wins and $6 billion in authorized buybacks, shifts the forward earnings trajectory at a moment when ADP’s valuation has disconnected sharply from its business momentum.

As TIKR estimates, ADP will grow normalized EPS from $10.01 in FY25 to $10.97 in FY26 and $11.97 in FY27, with the Lyric platform’s accelerating new logo wins and WorkForce Suite integration supporting that 9.6% growth assumption.

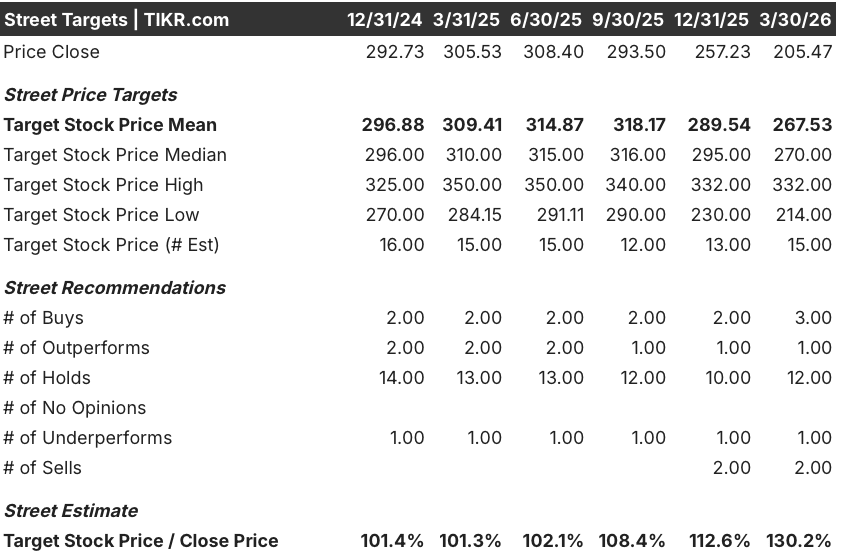

Wall Street’s current stance leans cautious but is directionally bullish on price: 15 analysts cover ADP, with 3 buys, 1 outperform, 12 holds, and 3 sells, while the mean target of $267.53 implies 30.2% upside from $205.47, anchored to the EPS raise and buyback program.

The $214 bear target assumes PEO worksite employee growth stalls further and pays-per-control stays flat, while the $332 bull case prices in Lyric reaching critical enterprise mass and EBITDA margins expanding beyond the 29.2% TIKR projects for FY26.

What Does the Valuation Model Say?

Still, as TIKR estimates, ADP’s mid-case price target of $298.22 rests on 5.2% revenue CAGR through FY30 and net income margins expanding from 19.9% in FY25 to 20.9%, justified by the structural shift in enterprise HCM spend toward Lyric and the WorkForce Suite.

At roughly 18.7x forward normalized EPS of $10.97, ADP trades at a meaningful discount to the multiple its 10-year EPS CAGR of 13.2% historically commanded, with FY26 FCF margin already expanding to 23.9% from 23.2% in FY25: undervalued.

Also, Lyric’s 70%-plus new logo win rate and the $6 billion buyback authorization provide the two real-world anchors the TIKR mid-case $298.22 target requires, with EPS compounding at 9.2% annually making the 45.1% total return over 4.2 years structurally credible.

Management’s disclosure that the Q2 client satisfaction result was the single best in ADP history, paired with only a 10–30 basis point retention decline, confirms the moat is intact rather than eroding.

Moreover, A sustained deceleration in pays-per-control growth, currently near flat, would directly compress the revenue base supporting the 6% FY26 ES revenue growth assumption and undermine the margin expansion path.

The April 29 Q3 earnings release is the next confirmation point: watch pays-per-control for any improvement above flat and Lyric bookings for continued above-expectation delivery against the 9%–10% EPS growth guide.

Should You Invest in Automatic Data Processing, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up ADP stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Automatic Data Processing, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze ADP stock on TIKR for Free →