Key Takeaways:

- Arista Networks is executing a comprehensive AI networking transformation through enhanced back-end infrastructure, scale-out deployments, and strategic customer expansion across cloud titans and enterprise markets.

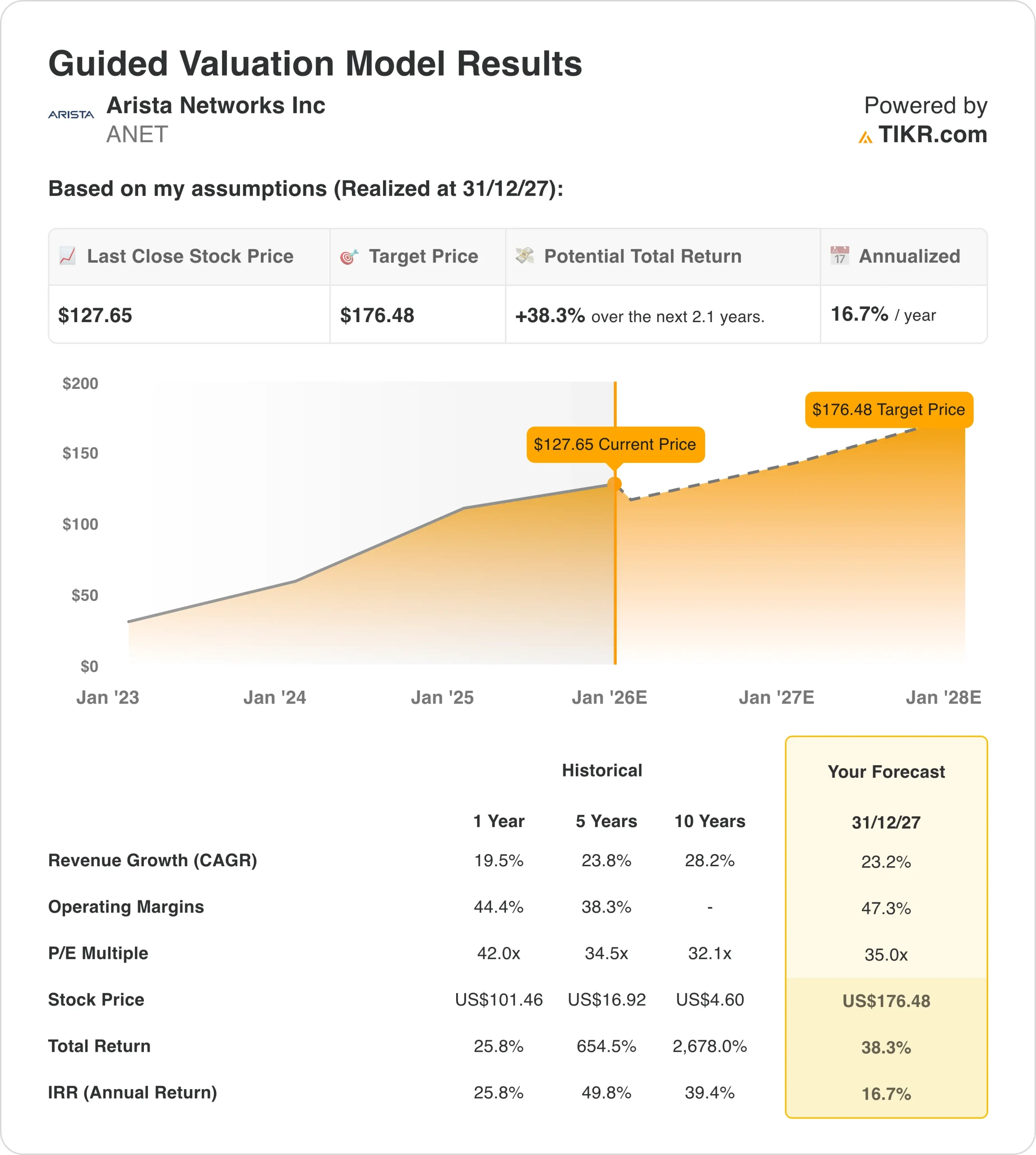

- ANET stock could reasonably reach $176/share by December 2027, based on our valuation assumptions.

- This implies a total return of 38% from today’s price of $128/share, with an annualized return of 17% over the next 2.1 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Arista Networks (ANET) is establishing new benchmarks in the AI networking segment through strategic technology evolution, addressing scale-out fabrics, blue-box solutions, and Ethernet-based architectures across the cloud titan, enterprise, and neocloud markets.

Arista Networks serves data center customers globally through its EOS operating system philosophy, which spans 10,000+ enterprise customers, emerging AI networking offerings, and distributed fabric capabilities, all delivered with industry-leading reliability and performance.

Core offerings include cloud titan networking solutions, campus enterprise systems, AI back-end infrastructure, and optimized switching platforms featuring 800-gigabit and 1.6-terabit capabilities, distributed scheduled fabric architecture, and comprehensive network automation.

The networking leader delivered third-quarter 2025 revenue of $2.31 billion, a 28% year-over-year increase. Its product deferred revenue grew by $625 million sequentially, indicating continued momentum despite some supply chain constraints affecting shipment timing.

Arista Networks demonstrates strong execution across strategic initiatives under the leadership of CEO Jayshree Ullal and the senior management team, including newly promoted CTO Ken Duda and President/COO Todd Nightingale.

The company grew its AI-related revenue to approximately $1.5 billion in 2025 while achieving 65.2% gross margins and maintaining an operating margin of 48.6%.

ANET completed major AI fabric deployments with three of four 100,000+ GPU customers going into production by year-end 2025.

ANET stock went public in 2014 and has delivered returns of over 2,600% to shareholders since the IPO.

Here’s why Arista Networks stock could provide strong returns through 2027 as it capitalizes on AI networking trends while scaling its Ethernet solutions across diverse cloud and enterprise deployments.

See analysts’ full growth forecasts and estimates for Arista Networks stock (It’s free) >>>

What the Model Says for ANET Stock

We analyzed the upside potential for Arista Networks stock using valuation assumptions based on its AI networking dominance and market expansion opportunities across back-end infrastructure and enterprise growth strategies.

Analysts recognize an opportunity ahead for Arista Networks stock given its proven execution track record, brand strength, and systematic approach to building competitive advantages while maintaining exceptional profitability in the expanding AI networking market.

Arista’s diversified growth strategy provides multiple vectors. At the same time, the Ethernet scale-up initiative validates that comprehensive network solutions can drive revenue growth and customer returns in the evolving AI infrastructure landscape.

Based on estimates of 23% annual revenue growth, 47% operating margins, and a normalized P/E valuation multiple of 35x, the model projects Arista Networks stock could rise from $128/share to $176/share.

That would be a 38% total return, or a 17% annualized return over the next 2.1 years.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for ANET stock:

1. Revenue Growth: 23%

Arista Networks delivered a strong third quarter 2025 performance, with 28% revenue growth driven by momentum across all business segments, including AI networking, enterprise campus, and cloud titan deployments.

The company’s product deferred revenue totaled $4.7 billion, representing the majority of the balance for the first time.

This growth reflects the company’s shift toward larger AI data center build-outs with 18-24 month acceptance clauses, compared to the traditional 6-12 month cycles in cloud deployments.

Growth drivers include expanding demand for AI infrastructure, with the company targeting $2.75 billion in AI-related revenue for 2026, up from $1.5 billion in 2025. Management also expects campus revenue to grow from $750-800 million in 2025 to $1.25 billion in 2026.

The company is experiencing strong momentum with 15-20 vanguard customers deploying AI infrastructure beyond the top four cloud titans. These include neoclouds, sovereign wealth funds, and AI-as-a-service providers putting their first deployments into production during calendar year 2025.

Arista surpassed $2.3 billion in quarterly revenue and raised its full-year 2025 guidance to approximately $8.87 billion, representing 26-27% annual growth. For 2026, management committed to 20% growth, resulting in total revenue of $10.65 billion.

We used a 23% forecast, reflecting Arista’s ability to capture AI networking demand through scale-out, scale-up, and scale-across deployments while expanding enterprise campus penetration. This balances the company’s strong near-term momentum against longer acceptance cycles and potential supply chain variability.

2. Operating margins: 47%

In the third quarter of 2025, Arista Networks achieved operating margins of 48.6%, up from previous quarters, demonstrating strong operational leverage across its capital-efficient business model.

It reported gross margins of 65.2%, driven by a favorable customer mix and benefits from improved inventory management. Management targets 62-64% gross margins for 2026, accounting for cloud titan volume and product mix dynamics.

Operating expenses came in at 16.6% of revenue, with R&D at 10.9%, sales and marketing at 4.7%, and G&A at 1.0%. The efficient expense structure reflects Arista’s focus on engineering excellence and direct customer engagement.

The company is investing strategically in next-generation capabilities, including:

- 800-gigabit and 1.6-terabit switching platforms for AI back-end networks

- Distributed scheduled fabric (DSF) and non-scheduled fabric architectures offering customer choice

- AVA (Autonomous Virtual Assist) using AI for network design, operation, and troubleshooting

- Etherlink portfolio supporting scale-out, scale-up, and scale-across use cases

We forecast 47% operating margins, reflecting management’s proven ability to maintain industry-leading profitability while investing in R&D and scaling the business.

This accounts for the company’s 43-45% operating margin guidance for 2026 while recognizing potential upside from a favorable mix and operating leverage.

3. Exit P/E Multiple: 35x

Arista Networks stock currently trades at a next-twelve-months P/E multiple of approximately 40x, reflecting its premium positioning, technology leadership, and proven ability to generate consistent growth through economic and technology cycles.

Historical P/E multiples show premium valuations: 42x over the past year, 35x over the last five years, and an average of 32x over the last decade, demonstrating sustained investor confidence in the company’s competitive advantages.

We maintain a 35x exit multiple given Arista’s execution capabilities, secular tailwinds in AI infrastructure spending, and a systematic approach to building sustainable competitive advantages through engineering excellence and customer partnerships.

The company’s 19 consecutive record quarters demonstrate operational consistency, while partnerships with major cloud titans (Microsoft, Meta, Oracle) and AI labs (OpenAI, Anthropic) validate Arista’s strategic positioning in the evolving infrastructure landscape.

Management’s disciplined capital allocation includes strategic share repurchases and strong free cash flow generation of $1.3 billion in Q3 . The company maintains a strong balance sheet with $10.1 billion in cash and investments, supporting both organic investment and shareholder returns.

The AI networking opportunity represents significant long-term growth potential. Management increased its total addressable market estimate to $105 billion from $70 billion just one year earlier, with scale-up representing a net-new TAM category not yet included in those figures.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

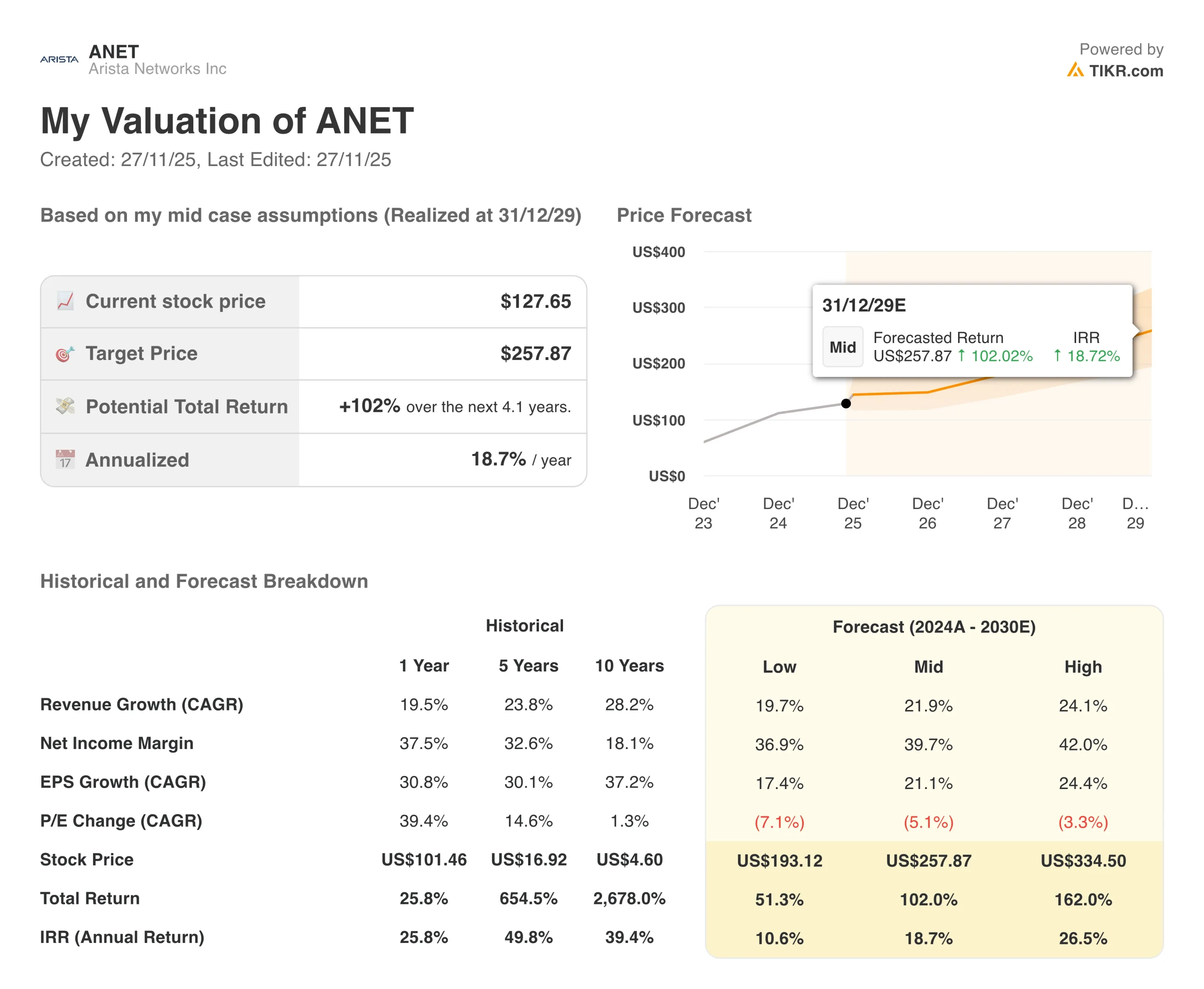

Different scenarios for ANET stock through 2030 show varied outcomes based on AI deployment execution and competitive dynamics (these are estimates, not guaranteed returns):

- Low Case: Supply constraints persist and white box competition intensifies → 11% annual returns

- Mid Case: Successful Ethernet scale-up transition and steady enterprise campus expansion → 19% annual returns

- High Case: Strong AI infrastructure acceleration and expanded scale-up market share → 27% annual returns

Even in the conservative case, Arista Networks stock offers double-digit returns, supported by its technology positioning and proven ability to maintain customer partnerships and engineering excellence, while competitors struggle with proprietary lock-in limitations and lower software quality.

The upside scenario for ANET stock could deliver exceptional performance if the company successfully captures scale-up networking opportunities during the multi-year AI infrastructure build-out while maintaining dominant share in scale-out deployments and achieving targeted campus growth across enterprise customers.

See what analysts think about ANET stock right now (Free with TIKR) >>>

How Much Upside Does ANET Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!