Dover Corporation (NYSE: DOV) trades near $187/share after a steady recovery from recent lows. The stock has been range bound for much of the year as softer industrial demand and mixed revenue trends kept sentiment cautious. Despite these headwinds, Dover continues to maintain strong profitability and solid returns on capital, which has helped support its valuation.

Recently, Dover completed the separation of its Belvac business and advanced restructuring efforts across multiple segments to simplify operations and improve efficiency. Management also highlighted improving order activity in parts of the portfolio, suggesting early signs of stabilization heading into 2026. These developments show that Dover is positioning itself for cleaner growth after a challenging stretch for industrial companies.

This article explores where Wall Street analysts believe Dover could trade by 2027. We reviewed consensus targets and the assumptions behind the valuation model to outline the stock’s potential path. These figures reflect current analyst expectations and are not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Modest Upside

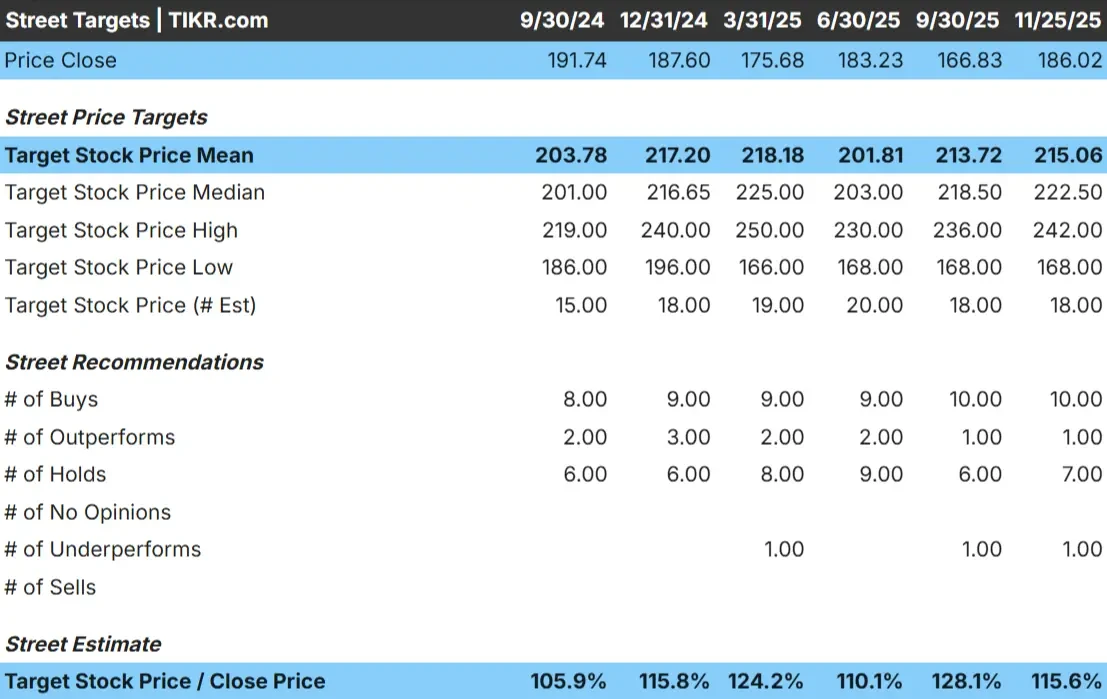

Dover trades near $187/share today, and the Street’s average target of $215/share suggests about 15% upside. This places Dover in the modest upside category, where the stock could outperform if margins improve or demand strengthens faster than expected.

- High estimate: $242/share

- Low estimate: $168/share

- Median target: $223/share

- Ratings: 10 Buys, 1 Outperform, 7 Holds, 1 Sell

For investors, the takeaway is straightforward. Most analysts expect a controlled and steady move higher, with targets clustered between $200 and $225. This tight range indicates broad agreement on Dover’s earnings power and reinforces the idea that the stock is viewed as a stable operator rather than a high volatility opportunity.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

Dover Growth Outlook and Valuation

The company’s fundamentals appear stable and supported by improving profitability.

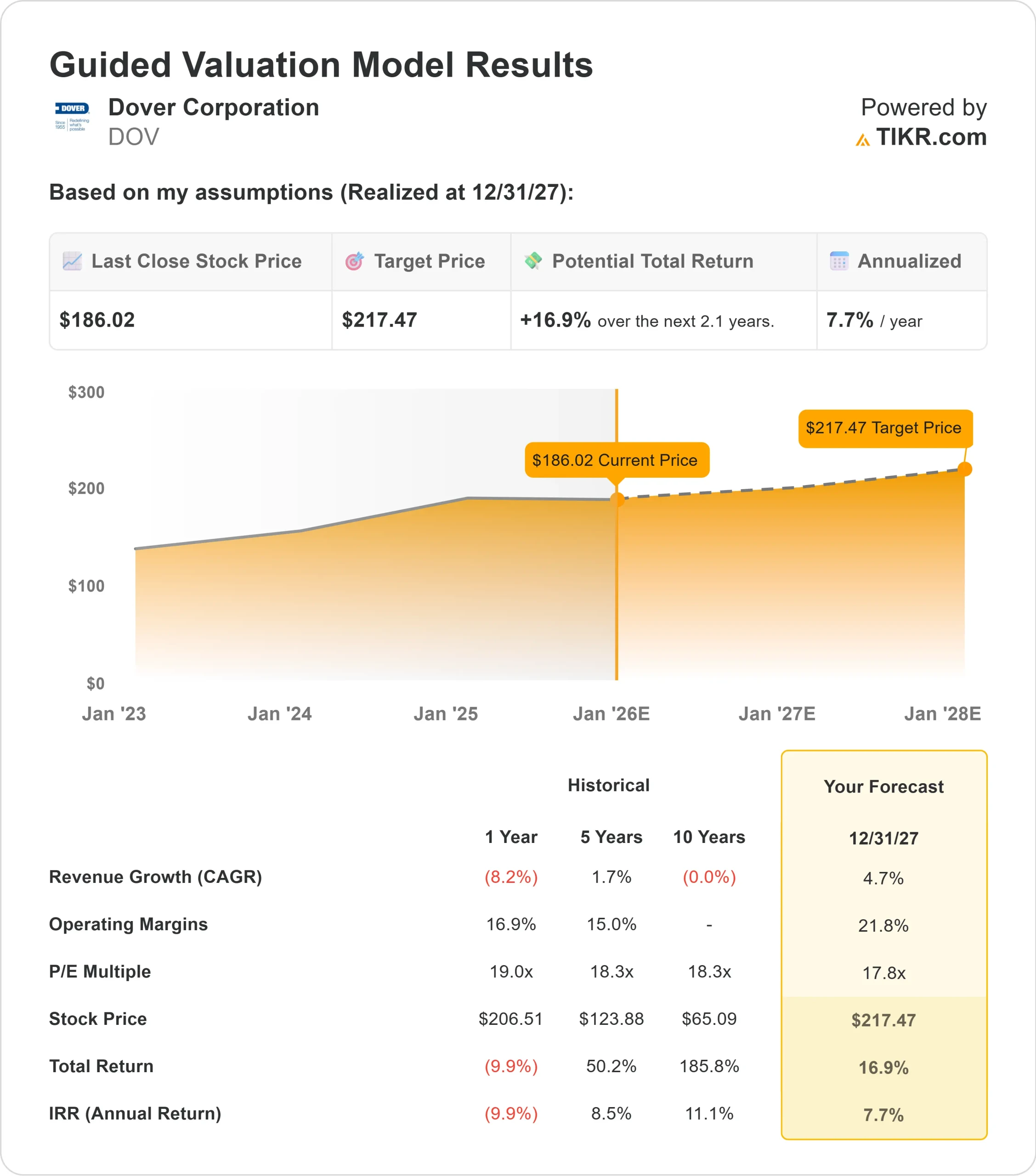

- Revenue is projected to grow 4.7% through 2027

- Operating margins are expected to reach 21.8%

- Shares are valued using a 17.8x forward P E assumption

- Based on analysts average estimates, TIKR’s Guided Valuation Model suggests $217/share by 12/31/27

- That implies about 17% total return, or roughly 8% annualized

These numbers point to steady but controlled compounding. Dover’s outlook depends more on margin expansion and disciplined execution than on rapid revenue acceleration. For investors, the setup suggests a predictable return path supported by stable profitability and low leverage, as long as end market demand remains consistent.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Dover’s operational discipline and consistent execution continue to support investor confidence. The company’s portfolio includes essential industrial businesses that tend to hold up across different parts of the cycle, which helps maintain stability even when demand softens. Management’s focus on strategic restructuring, cost efficiency, and portfolio refinement has also added to the constructive sentiment.

These steps signal that Dover is strengthening its foundation while preparing for more favorable conditions. For investors, this mix of disciplined management and gradual improvement in certain end markets supports a reasonable case for continued earnings momentum.

Bear Case: Slower Growth and Limited Rerating Potential

The biggest challenge for Dover is its modest growth outlook. While the company remains profitable and well managed, its revenue trajectory is expected to improve slowly. Without stronger demand across key segments, earnings could progress at a measured pace.

Valuation could also limit upside. Dover already trades near a typical forward multiple for the business, which makes a major rerating less likely unless fundamentals surprise to the upside. Investors who prioritize faster top line growth may gravitate toward industrial peers with more pronounced secular tailwinds.

Outlook for 2027: What Could Dover Be Worth?

Based on analysts average estimates, TIKR’s Guided Valuation Model suggests Dover could trade near $217/share by the end of 2027. That represents about 17% total return, or roughly 8% annualized, from current levels near $187/share.

This outlook reflects a balanced and realistic path forward. Stronger upside would require faster revenue growth, improved demand across the portfolio, or sharper than expected margin expansion. Without those catalysts, returns are likely to remain steady and earnings driven.

For investors, Dover looks like a dependable long term industrial holding with disciplined operations, stable profitability, and a clear valuation framework. While not a high growth story, it offers predictable performance for those seeking measured and consistent compounding.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>