PG&E Corporation (NYSE: PCG) has had a turbulent stretch in recent years. The stock trades near $16/share as investors continue to watch regulatory developments, wildfire liabilities, and the company’s elevated leverage. Even with these pressures, PG&E has delivered more stable operating results and maintained healthy margins, which has helped sentiment gradually improve.

Recently, PG&E secured approval for a major phase of its Undergrounding Initiative, a long term plan to reduce wildfire risk by placing power lines below ground in high risk areas. Management also reaffirmed progress on its multi year grid modernization strategy, highlighting improvements in system reliability and infrastructure upgrades. These developments show that PG&E is taking meaningful steps to strengthen its operations and reduce long term risk.

This article explores where Wall Street analysts believe PG&E could trade by 2027. We pulled together consensus targets and TIKR’s Guided Valuation Model inputs to outline the stock’s potential path. These figures reflect current analyst expectations and are not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Meaningful Upside

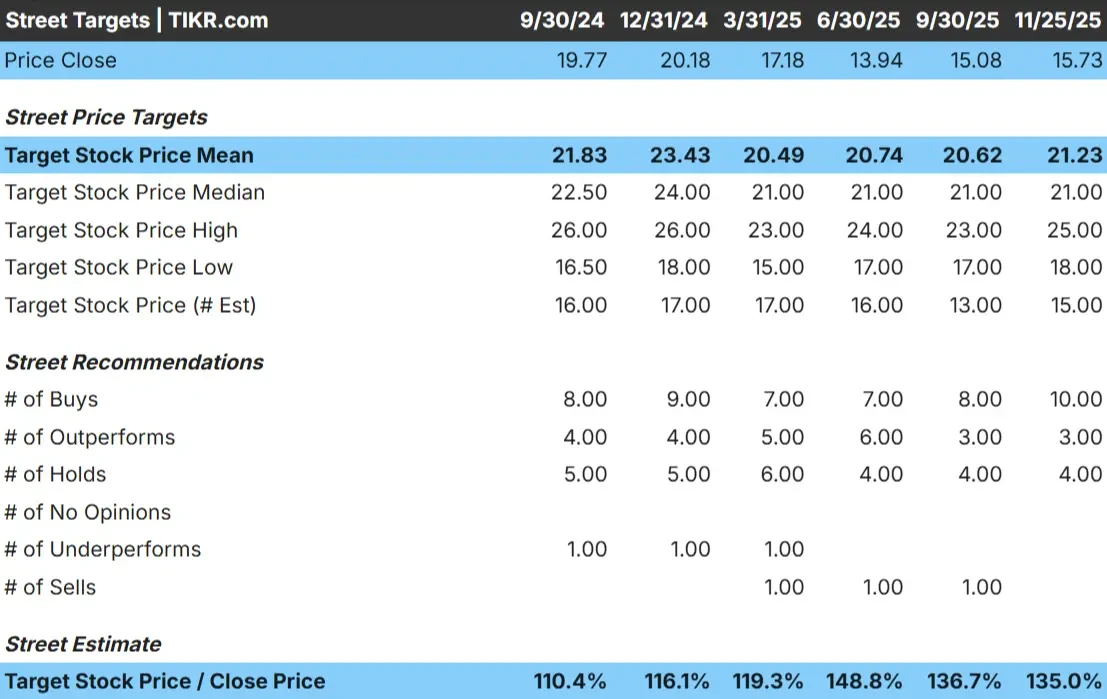

PG&E trades near $16/share today. The average analyst price target is $21/share, which points to roughly 35% upside. Forecasts show a range of views:

- High estimate: $25/share

- Low estimate: $18/share

- Median target: $21/share

- Ratings: 10 Buys, 3 Outperforms, 4 Holds

Because the upside exceeds 30%, analysts see meaningful return potential if PG&E continues executing steadily. For investors, this reflects cautious optimism. The stock can rerate higher, but only if the company maintains consistent margins, delivers reliable operations, and avoids regulatory setbacks.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

PG&E: Growth Outlook and Valuation

The company’s fundamentals point to steady but moderate growth based on the model inputs:

- Revenue growth forecast: 4%

- Operating margin forecast: 25%

- Forward P E used: 10x

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 10x forward P E suggests $19/share by 2027

- That implies 18 to 19% upside, or about 8% annualized returns

These numbers suggest PG&E can compound steadily, although not at a rapid pace. Most of the expected return comes from consistent earnings rather than a major valuation shift, which is typical for a regulated utility.

For investors, PG&E screens as a stable long term operator where predictability drives the majority of returns. The balance sheet and regulatory backdrop still limit how far the stock can rerate, but reliable execution can support solid compounding over time.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Operational consistency has improved. PG&E continues to harden its grid, upgrade infrastructure, and invest in wildfire mitigation. These efforts help reduce risk and create a clearer path to stable earnings. System reliability improvements also support a more dependable operating environment.

For investors, this progress signals that PG&E is addressing long standing challenges with greater discipline. The gradual strengthening of operations makes it easier for the company to meet expectations and maintain steadier financial performance.

Bear Case: Leverage and Regulatory Pressure

Despite the improvements, PG&E’s challenges remain significant. The company still carries high leverage, and its financial flexibility is more limited than many peers. This makes it more sensitive to higher costs, external shocks, or changes in the regulatory environment.

Regulatory scrutiny also remains intense. Any delays, cost recovery issues, or missteps in PG&E’s long term infrastructure plans could pressure earnings or sentiment. For investors, the risk is that PG&E must execute cleanly to avoid setbacks that could weigh on valuation.

Outlook for 2027: What Could PG&E Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 10x forward P E suggests PG&E could reach about $19/share by 2027, representing an 18 to 19% gain, or roughly 8% annualized returns.

This outlook assumes stable execution and continued progress on risk reduction. To unlock stronger upside, PG&E would need cleaner regulatory visibility, better cost efficiency, and deeper improvements across its service areas. Without that, returns are likely to remain steady but moderate, reflecting the company’s regulated profile and leverage constraints.

For investors, PG&E looks like a dependable long term utility with room for consistent compounding, although outsized gains depend on management continuing to strengthen operations and reduce risk across the system.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>