CenterPoint Energy (NYSE: CNP) trades near $40/share, close to its 52 week high after a steady recovery in regulated earnings and margin improvement. The company continues to benefit from predictable rate base growth and stable regulated operations, which have supported its positive performance over the past year.

Recently, CenterPoint finalized regulatory approvals tied to grid modernization and storm hardening across several major territories. Management also highlighted improving customer growth and continued progress on system upgrades intended to strengthen long term reliability. These developments show that the company is executing well even as the broader utility sector manages slower demand and higher financing costs.

This article reviews where analysts expect the stock to trade by 2027 using consensus targets and TIKR’s Guided Valuation Model based on analysts average estimates.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Modest Upside

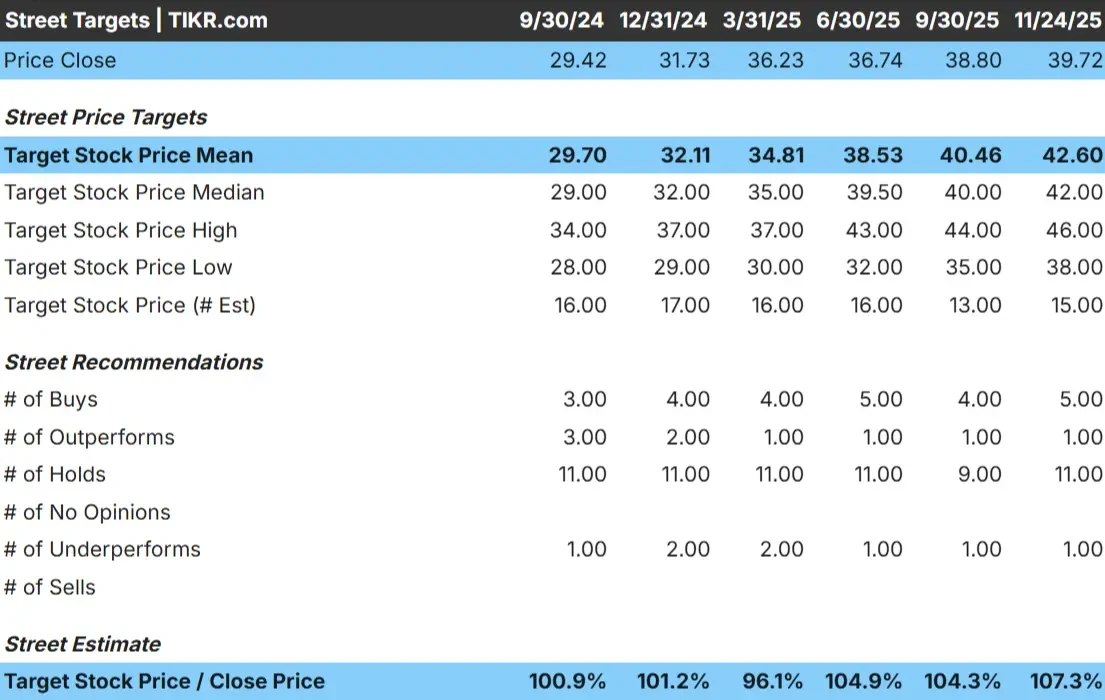

CNP trades around $40/share. The average analyst price target sits at $43/share, which implies roughly 8% upside. This places the stock in the modest upside category, where returns can improve if earnings exceed expectations.

Target range:

- High estimate: $46/share

- Low estimate: $38/share

- Median target: $42/share

- Ratings: 5 Buys, 1 Outperforms, 11 Holds, 1 Underperform

The narrow spread between high and low targets shows that analysts share a consistent view of the company’s outlook. For investors, this signals a stable utility that will likely follow its earnings path rather than experience a major valuation shift.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

CNP Growth Outlook and Valuation

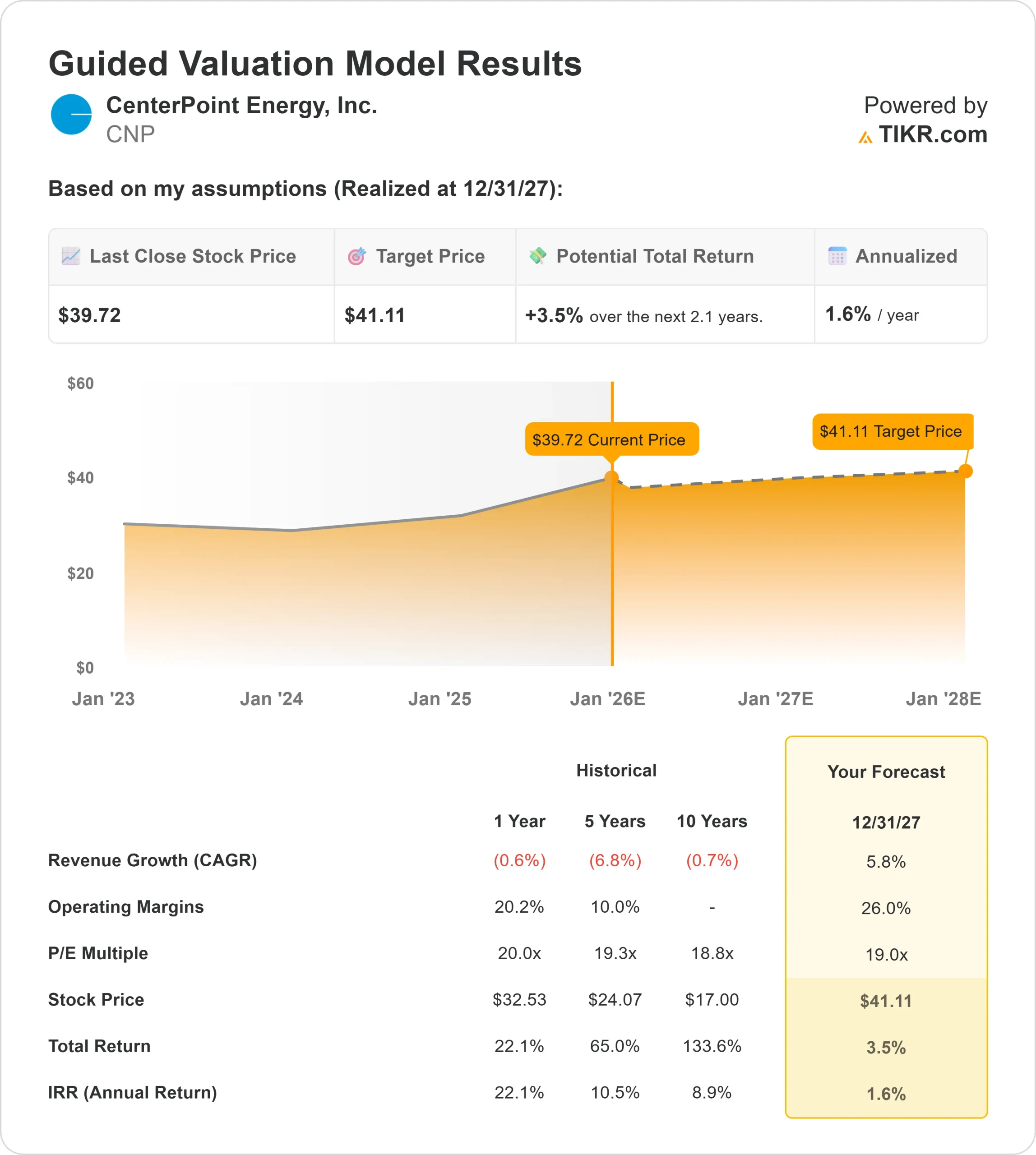

CenterPoint’s fundamentals appear stable based on the valuation model inputs:

- Revenue growth is projected at 5.8%

- Operating margins are expected to remain near 26%

- Shares are valued using a 19x forward P E

- Based on analysts average estimates, TIKR’s Guided Valuation Model using a 19x forward P E suggests about $41/share by 2027

- This implies roughly 3.5% total return, or about 1.6% annualized

These numbers indicate that CenterPoint can compound steadily, but not at a level that drives strong share price appreciation. The stock appears fairly valued for its growth profile, which means upside will depend on consistent execution and supportive regulatory outcomes.

For investors, CenterPoint screens as a stable utility rather than a high growth story. Most of the return potential is likely to come from predictable earnings and dividends rather than a significant move in the stock price.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

CenterPoint continues to benefit from long term infrastructure investment, ongoing system modernization and increasing focus on reliability improvements. Customer growth in key service regions has added support to its operating base, and management remains focused on execution quality across large capital programs.

These efforts help strengthen the company’s regulatory standing and provide clearer earnings visibility. For investors, these developments suggest that CenterPoint has a solid foundation for long term performance even if the pace of growth remains measured.

Bear Case: Growth Constraints and Rate Sensitivity

Even with these strengths, CenterPoint faces challenges that may limit its ability to outperform. Growth remains moderate, and the company operates in a sector that is highly sensitive to interest rate trends. Shifts in regulatory timing or cost recovery can also influence earnings, and utilities with slower expansion often struggle to command higher valuations.

For investors, the risk is that CenterPoint’s stability may cap upside potential unless earnings meaningfully improve or the regulatory environment becomes more favorable.

Outlook for 2027: What Could CNP Be Worth?

Based on analysts average estimates, TIKR’s Guided Valuation Model suggests CenterPoint could trade near $41/share by 2027, which represents about 3 to 4% upside from today. That translates to roughly 1.6% annualized returns.

This outlook already assumes steady execution and continued rate base expansion. To unlock stronger upside, CenterPoint would need faster earnings growth, a more supportive rate environment or improved cost efficiency. Without that, investors should expect stable but limited returns.

For investors, CenterPoint screens as a reliable long term utility holding. The company offers steady earnings, predictable cash flows and dependable income, but significant upside will depend on management outperforming current expectations.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>