Trane Technologies plc (NYSE: TT) trades near $419/share after a steady year. Demand for HVAC upgrades and energy efficient systems has supported stable earnings, and the company continues to outperform most industrial peers on margins and returns. Despite a mixed macro backdrop, Trane has kept growth intact across both residential and commercial markets.

Recently, the company rolled out new climate control and decarbonization solutions aimed at large enterprise customers, helping strengthen booking momentum heading into 2026. Trane also reported solid performance in its Commercial HVAC segment, supported by resilient pricing and ongoing demand for building efficiency upgrades. These developments show that Trane is still executing effectively as sustainability spending remains a priority across many industries.

This article explores where Wall Street analysts expect TT to trade by 2027. We have pulled together consensus targets and valuation models to outline the stock’s potential path. These figures reflect current analyst expectations and not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Modest Upside

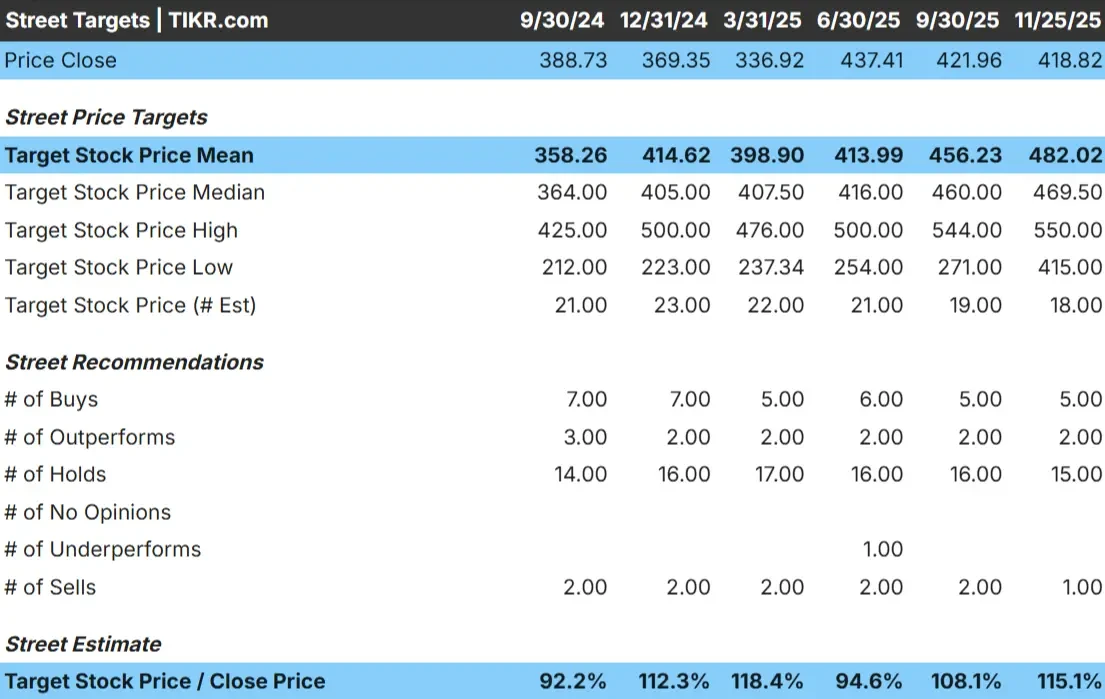

TT trades around $419/share, and the Street’s average target of $482/share points to about 15% upside. This places expectations in the modest range, suggesting analysts see the potential for gains but not a major breakout.

Street targets:

- High estimate: $550/share

- Low estimate: $415/share

- Median target: $470/share

- Ratings: 5 Buys, 2 Outperforms, 15 Holds, 1 Sell

Overall, analysts expect TT to continue grinding higher as long as earnings remain consistent. The tight spread around the consensus target indicates moderate conviction. For investors, this means TT is more likely to follow its dependable compounding path rather than deliver sharp moves driven by sentiment.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

TT Growth Outlook and Valuation

The company’s fundamentals appear steady and well supported by long term demand across its HVAC and building technology markets.

- Revenue is projected to grow about 7.5% through 2027

- Operating margins are expected to remain near 19.3%

- Shares trade at roughly 27x forward earnings

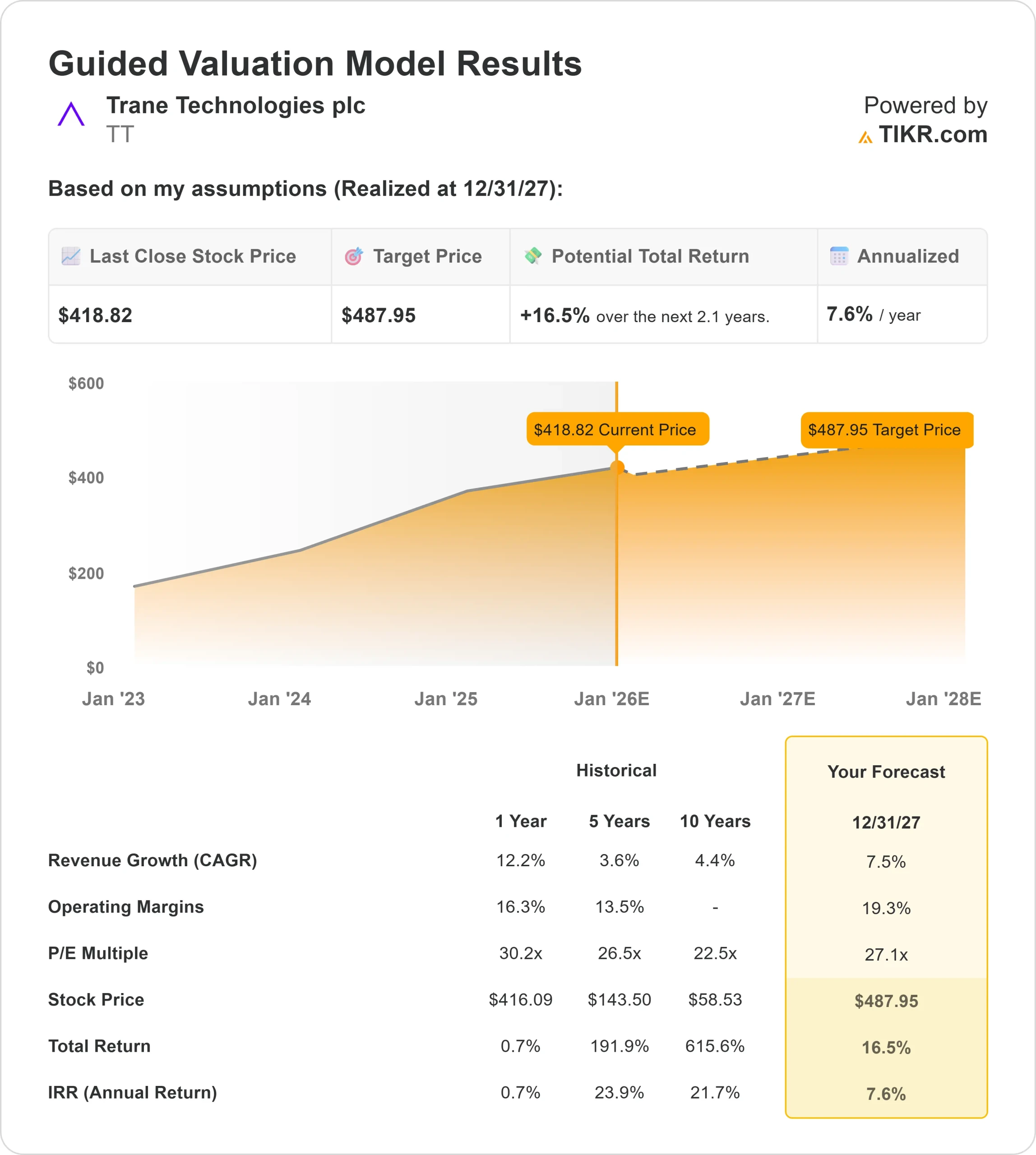

- Based on analysts average estimates, TIKR’s Guided Valuation Model using a 27x forward P E suggests about $488/share by 2027

- That implies roughly 16.5% upside, or about 7.6% annualized returns

These numbers point to reliable compounding rather than rapid acceleration. Trane continues to benefit from strong pricing, efficient operations and disciplined capital allocation. The company also maintains low leverage, which helps support stability across different market cycles.

For investors, TT looks like a dependable industrial compounder. Most of the expected returns are tied to steady earnings growth, not major valuation expansion. Investors seeking consistency and long term visibility may find the stock appealing within the broader industrial sector.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Trane is positioned at the center of long term themes such as energy efficiency, electrification and building modernization. Companies and institutions are investing in reducing emissions and improving climate control performance, which directly supports demand for Trane’s solutions. Strength in Commercial HVAC highlights the company’s ability to benefit from these trends.

Management’s continued expansion into decarbonization and advanced building technologies also strengthens customer relationships and enhances the company’s market position. For investors, these efforts suggest Trane has the tools to maintain stable earnings growth even when broader industrial spending becomes uneven.

Bear Case: Valuation and Slower Trends

Despite its strengths, TT trades at a premium valuation relative to its growth rate. Shares sit near 27x forward earnings, which limits the potential for a meaningful rerate higher. If revenue growth slows or pricing becomes more competitive, the stock may struggle to justify this premium.

Competition across HVAC markets continues to intensify as peers expand their own energy efficiency and sustainability offerings. Any loss of pricing power, margin pressure or a slowdown in construction activity could weigh on results. For investors, the risk is that stability alone may not be enough to drive stronger returns if earnings come in softer than expected.

Outlook for 2027: What Could TT Be Worth?

Based on analysts average estimates, TIKR’s Guided Valuation Model suggests TT could trade near $488/share by 2027. That represents about 16% upside, or roughly 8% annualized returns.

This would reflect solid long term performance from a high quality industrial, but it already assumes steady execution and firm demand across Trane’s HVAC markets. To deliver meaningfully stronger gains, TT would need faster revenue growth, improved operating leverage or a stronger construction cycle. Without that, investors should expect dependable but measured compounding.

For investors, TT stands out as a consistent long term operator with strong fundamentals and disciplined execution. The potential upside is reasonable, but future returns will depend on how well management sustains growth in a competitive and evolving industry.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>