Carrier Global Corporation (NYSE: CARR) has struggled over the past year. The stock trades near $54/share after falling about 31% as softer HVAC demand and declining margins weighed on results. Higher interest rates and slower construction activity have also put pressure on performance, keeping the stock near the lower end of its recent range.

Recently, Carrier made several notable moves that have gained investor attention. The company continued expanding its heat pump offerings and advanced its building automation capabilities, both of which support long term efficiency and sustainability goals. Management also emphasized cost discipline and operational improvement, signaling an effort to strengthen margins after a challenging stretch. These developments suggest the company is taking active steps to support future growth even in a softer environment.

This article explores where Wall Street analysts believe Carrier could trade by 2027. The figures below are based on consensus estimates and TIKR valuation data, reflecting analyst expectations rather than TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Meaningful Upside

Carrier trades around $54/share today, and the average analyst price target of $73/share points to about 35% upside. This qualifies as meaningful upside based on current expectations.

- High estimate: $90/share

- Low estimate: $60/share

- Median target: $73/share

- Ratings: 11 Buys, 2 Outperforms, 11 Holds

For investors, the wide range between high and low estimates shows that sentiment is still cautious but not overly bearish. Analysts expect earnings to stabilize and gradually improve, but the pace of recovery remains uncertain. If margins strengthen and demand normalizes, the stock has room to climb meaningfully from current levels.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

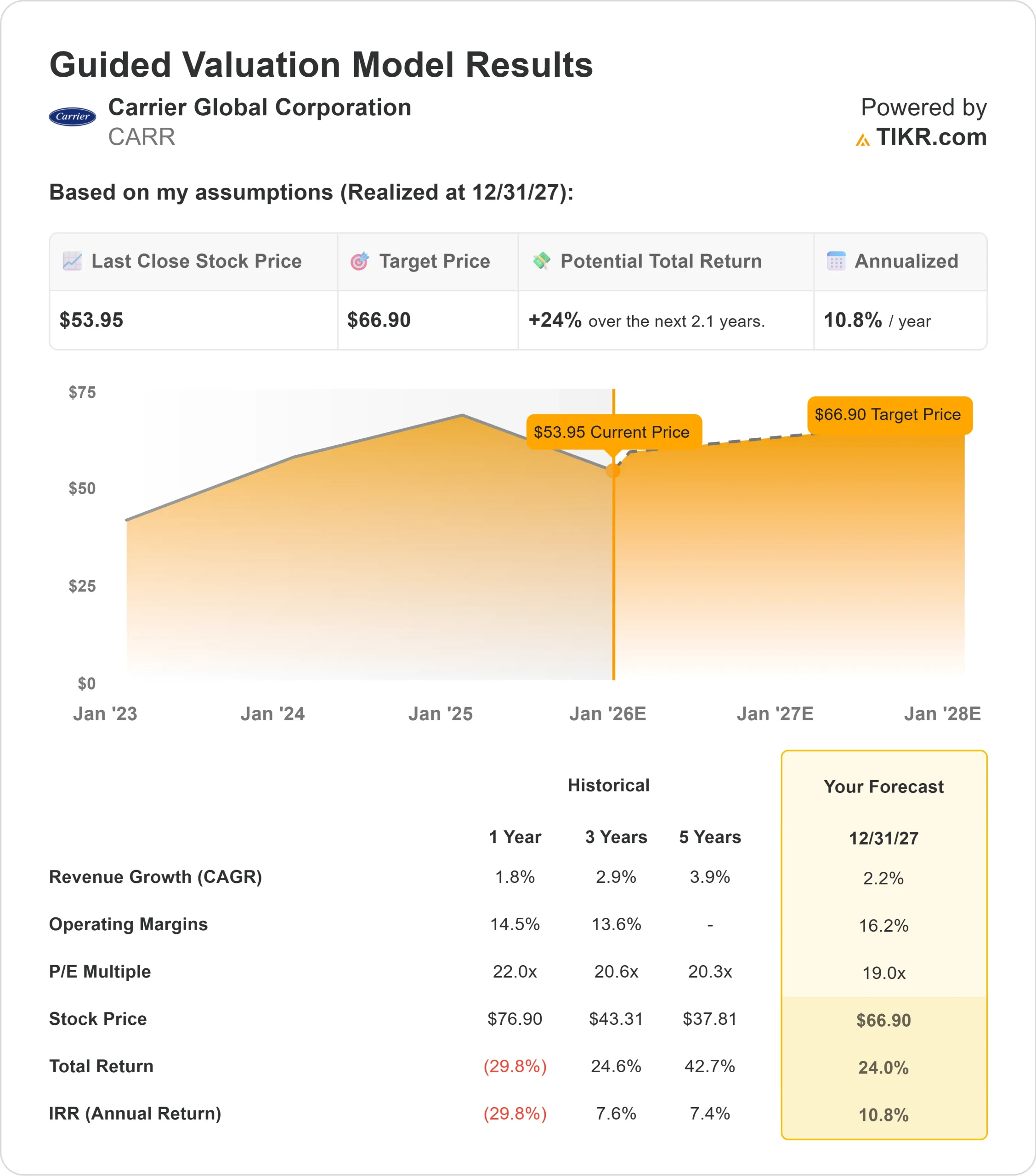

Carrier Growth Outlook and Valuation

Carrier’s fundamentals appear steady, supported by essential HVAC demand, efficiency driven regulations and increased adoption of modern building solutions. Growth is expected to remain moderate, but the company operates in markets with long duration demand and consistent replacement cycles.

- Revenue growth forecast: 2.2%

- Operating margin forecast: 16.2%

- Forward P E used: 19x

- Based on analysts average estimates, TIKR’s Guided Valuation Model using a 19x forward P E suggests about $67/share by 2027

- That implies about 24% upside, or roughly 11% annualized returns

These numbers indicate that Carrier can compound steadily, although not at a rapid pace. For investors, the appeal lies in dependable earnings, predictable demand and a valuation framework that supports measured long term returns rather than aggressive expansion.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Carrier benefits from long running demand across heating, cooling and building automation. Efficiency standards continue to tighten, creating steady replacement needs for modern HVAC systems and upgraded building solutions. The company’s expanding heat pump line and connected technologies also support better product mix and improved operating leverage over time.

Management has focused on strengthening the business through operational efficiency, better product positioning and more disciplined spending. For investors, these efforts suggest a clearer path toward stabilizing margins and rebuilding earnings as the broader environment improves.

Bear Case: Slower Growth and Margin Pressure

Carrier still faces meaningful challenges. Demand has softened, pricing has been pressured and margins have come under strain. Competition within HVAC and building technologies remains intense, and elevated interest rates continue to weigh on new construction and retrofit spending.

For investors, the main risk is that the recovery progresses more slowly than analysts expect. If margins do not rebound or if construction markets stay soft, the stock may fall short of valuation targets. The bear case centers on slower improvement in fundamentals combined with competitive pressures.

Outlook for 2027: What Could Carrier Be Worth?

Based on analysts average estimates, TIKR’s Guided Valuation Model suggests Carrier could trade near $67/share by 2027. This represents about 24% upside from current levels or roughly 11% annualized returns. The forecast points to a steady recovery rather than a sharp rebound.

While this outcome would reflect a meaningful improvement, it already assumes consistent execution and stable demand across Carrier’s core markets. To deliver stronger upside, the company would need faster margin expansion or a clearer rebound in commercial and residential spending. Without that, investors should expect measured returns that align with Carrier’s stable profile.

For investors, Carrier appears to be a reliable long term operator with durable demand and predictable fundamentals. The potential for significant upside will depend on how well management exceeds today’s cautious expectations.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>