Workday Inc. (NASDAQ: WDAY) has struggled over the past year, with the stock down about 14%. Shares trade near $231/share, well below the 12 month high of $294. Slower enterprise spending and a softer hiring environment have weighed on sentiment, creating a more cautious tone around cloud software valuations.

Recently, Workday delivered results that showed resilience despite the softer backdrop. Subscription revenue growth remained steady, margins continued to expand, and the company introduced new AI driven features that automate key HR and finance processes. Workday also secured several large enterprise wins, suggesting demand remains healthy even as customers become more selective with software budgets.

This article explores where Wall Street analysts think Workday could trade by 2028. We use consensus targets and TIKR’s Guided Valuation Model to outline the stock’s potential path. These figures reflect analyst expectations and are not TIKR’s own forecasts.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Modest Upside

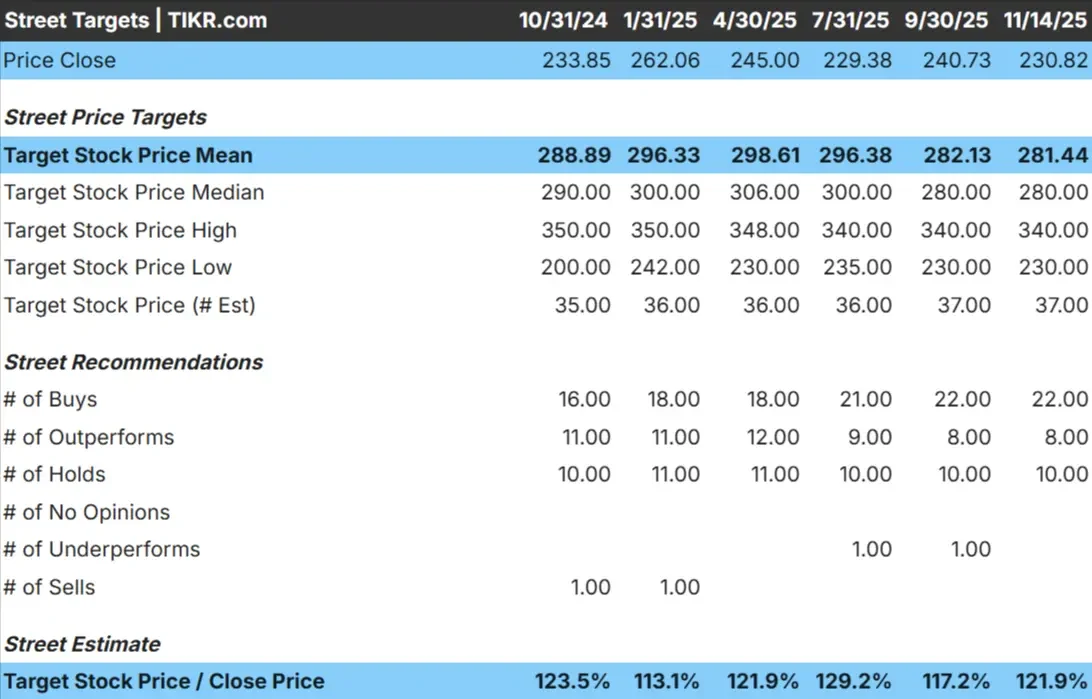

Workday trades near $231/share today. The average analyst price target is about $281/share, which suggests roughly 22% upside from current levels. The range is fairly stable, showing consistent expectations across the Street.

Here is the latest breakdown:

- High estimate: ~$340/share

- Low estimate: ~$230/share

- Median target: ~$280/share

- Ratings: 22 Buys, 8 Outperforms, 10 Holds

For investors, this points to modest but steady upside. Analysts are generally constructive on Workday’s long term trajectory, supported by recurring revenue and expanding adoption. However, the upside is not explosive, reflecting a balanced view of both growth potential and the current macro environment.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

Workday: Growth Outlook and Valuation

Workday’s financial outlook appears solid based on the model inputs:

- Revenue growth is projected at 12.6% annually through 2028

- Operating margins are expected to reach 31.9%

- Shares trade around 24.2x forward earnings

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model suggests Workday could reach about $331/share by 2028

- That implies roughly 43% total upside, or about 18% annualized returns

For investors, the model points to a reliable compounder. Workday does not need dramatic acceleration to deliver attractive returns. Predictable subscription revenue, strong customer retention, and continued operating leverage provide a stable foundation for multi-year growth.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Workday benefits from long term demand for cloud-based HR, payroll, and financial management systems. Companies continue shifting away from legacy software, and Workday remains one of the most trusted platforms for large enterprises. High renewal rates and steady module expansion further support its growth engine.

Management is also investing heavily in AI that enhances automation and improves decision making for HR and finance teams. These capabilities deepen customer reliance on the platform. For investors, these trends point to a business with deep customer integration and a long runway for continued expansion.

Bear Case: Valuation and Execution Risks

Despite the positives, Workday faces several risks that could limit returns. Its valuation assumes the company can maintain double digit revenue growth. If enterprise budgets tighten further, subscription growth may slow, which could pressure margins and the stock’s multiple.

Competition is another factor. Oracle, SAP, and emerging AI native tools continue to push aggressively into HR and finance. While Workday maintains a strong position, the market is becoming more crowded. For investors, the risk is not a collapse in fundamentals, but a moderation in growth that keeps returns closer to the middle of the range.

Outlook for 2028: What Could Workday Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model suggests Workday could trade near $331/share by 2028. That represents about 43% upside from current levels, or roughly 18% annualized returns.

While the outlook is encouraging, it already assumes Workday can sustain mid teens growth and continue expanding margins. Stronger upside would likely require accelerated adoption in financial management, deeper AI integration, or broader cross selling momentum across the platform.

For investors, Workday stands out as a long term compounder with a clear path to steady gains. It is not positioned for explosive growth, but its recurring revenue model and expanding capabilities give it the opportunity to deliver consistent and durable returns over the next several years.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>