MSCI Inc. (NYSE: MSCI) has been under pressure over the past year as markets adjusted to higher rates, slower ETF flows, and softer risk sentiment. The stock trades near $573/share, hovering below recent highs. Even so, MSCI remains one of the most durable index and data franchises in the world, supported by deep client relationships and high recurring revenue.

Recently, MSCI highlighted continued growth in its climate and ESG platforms, with more asset managers integrating these datasets into their investment workflows. The company also expanded several major index licensing agreements, signaling steady demand for its benchmarks even in a mixed macro environment. These moves show that MSCI continues to strengthen its competitive positioning.

This article explores where Wall Street analysts think MSCI could trade by 2027. We pulled together consensus price targets and valuation models to outline the stock’s potential path. These figures reflect current analyst expectations and are not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Modest Upside

MSCI trades near $570/share today. The average analyst price target is $655/share, which points to roughly 14% upside. The range is steady and reflects constructive but cautious sentiment:

- High estimate: about $710/share

- Low estimate: about $535/share

- Median target: about $670/share

- Ratings: 9 Buys, 5 Outperforms, 3 Holds, 1 Underperform

Since the implied upside is in the low teens, analysts view the opportunity as modest. For investors, this suggests the stock is likely to outperform through steady earnings compounding rather than big multiple expansion. The tight spread also shows analysts have a stable and aligned view of MSCI’s long-term fundamentals.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

MSCI: Growth Outlook and Valuation

MSCI’s long-term outlook continues to reflect a premium, high-margin business with strong competitive advantages:

- Revenue growth historically near 13%, with forecasts around 9% through 2027

- Operating margins consistently above 50%

- Shares trade around 31x forward earnings

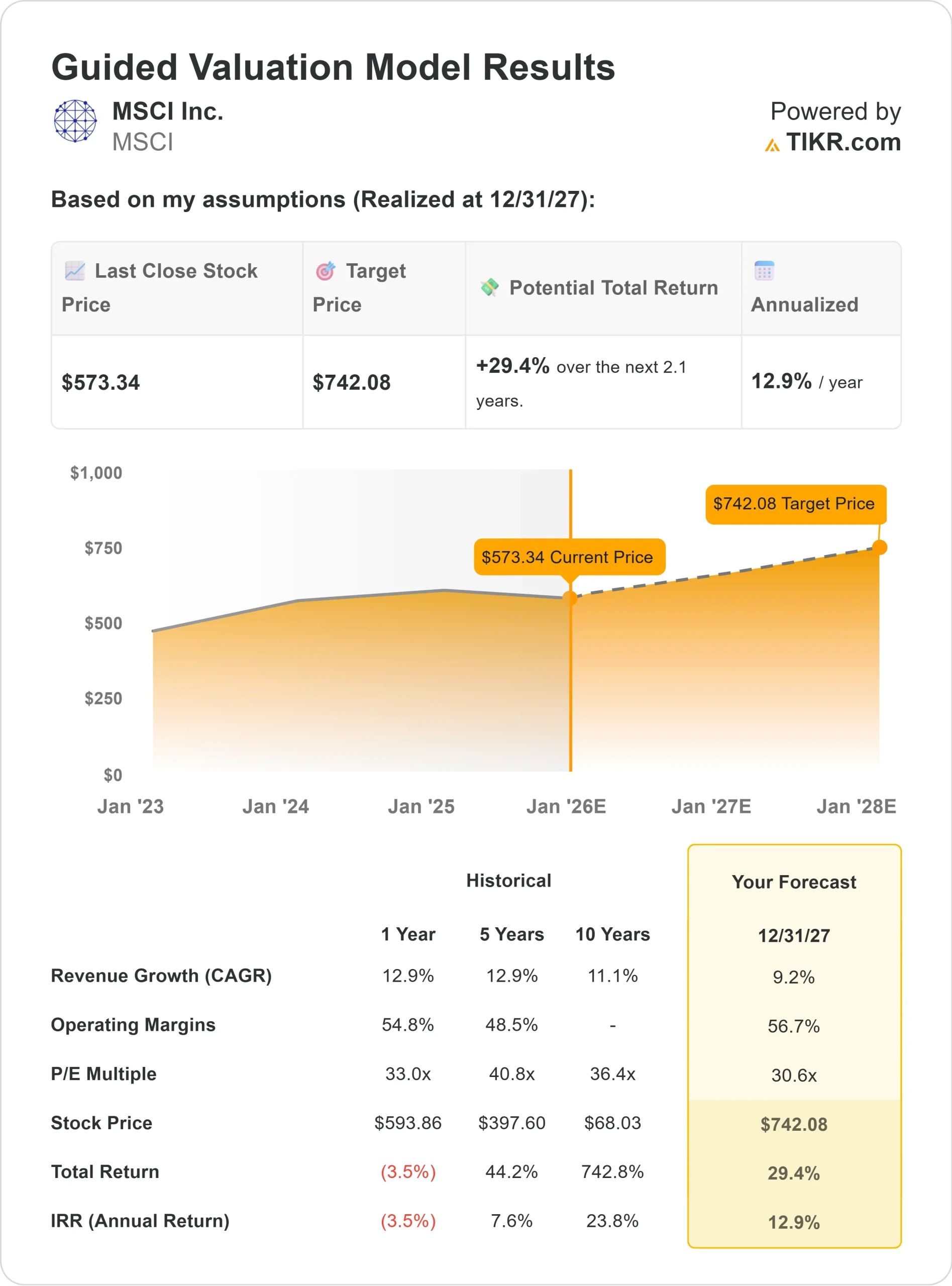

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 30.6x forward P/E points to about $742/share by 2027

- That represents roughly 29% upside, or about 13% annualized returns

These figures highlight a company that compounds through consistency. MSCI does not need rapid top-line acceleration to deliver meaningful results. Its recurring revenue, strong pricing power, and high client renewal rates allow earnings to grow even in slower market environments.

For investors, MSCI remains a steady compounder with a clear long-term earnings trajectory. The valuation is elevated, but the business supports that premium through reliable margins and durable demand for its index and data platforms.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

MSCI continues to benefit from global demand for indexing, ESG solutions, and analytics platforms. Asset managers depend on MSCI benchmarks to build ETFs and structured products, which helps maintain a stable and recurring revenue base. The company’s climate and ESG offerings are also gaining traction as institutions integrate more advanced data tools into their decision-making.

Management’s recent expansion of major index licensing agreements reinforces MSCI’s influence across the investment ecosystem. For investors, these developments suggest MSCI has the scale and brand strength to keep compounding earnings even when markets turn volatile.

Bear Case: Valuation and Market Sensitivity

Despite its strengths, MSCI trades at a premium valuation. With shares priced for stability and high margins, any slowdown in global equities or ETF flows could temporarily soften index-linked revenue. Client behavior still responds to broader market conditions, even if MSCI’s business model is not highly cyclical.

ESG and climate data growth may also fluctuate as regulations shift or institutions adjust spending priorities. While long-term demand remains intact, near-term adoption can vary. For investors, the core risk is not MSCI’s business quality but whether the current premium multiple already reflects a slower global backdrop.

Outlook for 2027: What Could MSCI Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 30.6x forward P/E suggests MSCI could trade near $742/share by 2027. That represents about 29% upside, or close to 13% annualized returns.

This outlook assumes steady growth supported by recurring revenue and consistent margins. It does not rely on aggressive market forecasts, which underscores the resilience of MSCI’s business model. To see stronger upside, the company would likely need faster expansion in ESG, climate analytics, or index adoption.

For investors, MSCI stands out as a reliable long-term compounder. The path to upside is driven by predictable earnings growth, strong client loyalty, and the global shift toward rules-based investing. While the valuation leaves less room for error, the underlying business remains one of the strongest in financial services.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>