Canadian Tire Corporation (CTC), founded in 1922, is one of Canada’s largest retail and financial services companies with a broad portfolio of iconic brands including Canadian Tire Retail, SportChek, Mark’s, and PartSource. Its vertically integrated model combines retail operations, a financial services arm, and a majority interest in CT REIT, which manages over 370 properties nationwide. Together, these segments form a diversified ecosystem of consumer spending, loyalty, and credit engagement across nearly 1,700 locations.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

The company’s loyalty engine, Triangle Rewards, remains a cornerstone of its customer strategy with over 11.9 million active members and growing partnerships that deepen engagement. In Q3, Canadian Tire announced Tim Hortons as a new partner and confirmed upcoming integrations with RBC and WestJet in 2026. These alliances are expected to expand reach, enhance data insights, and strengthen recurring sales through Canada’s most recognized consumer brands.

At the corporate level, Canadian Tire is advancing its “True North” transformation, a multi-year strategy to streamline operations, enhance digital infrastructure, and refocus capital on growth. The restructuring, completed in late Q3, consolidates management functions and optimizes its store network, particularly SportChek and Atmosphere, to improve profitability and agility heading into 2026.

Quickly value any stock with TIKR’s powerful new Valuation Model (It’s free!) >>>

Financial Story

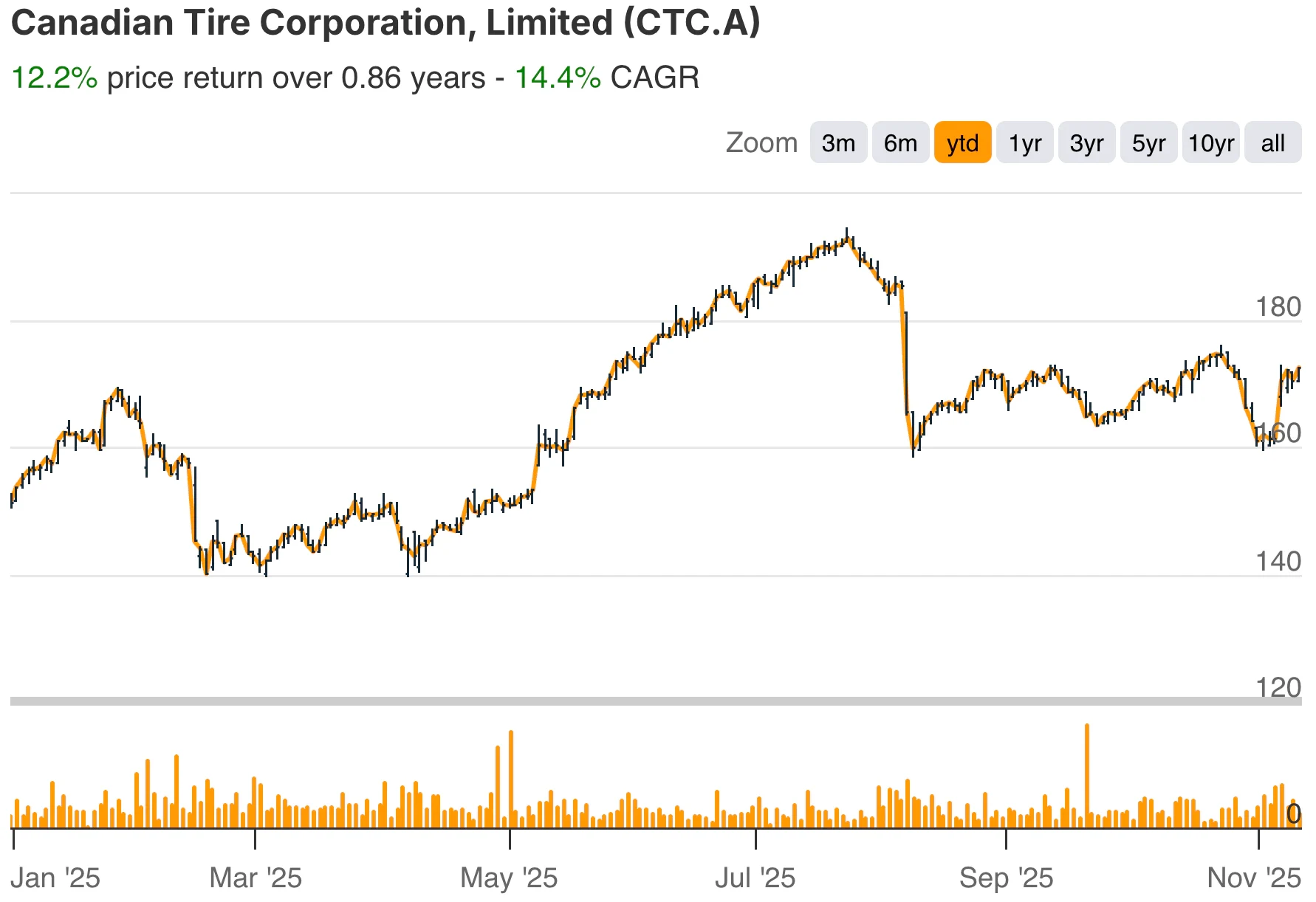

For the quarter ended September 27, 2025, Canadian Tire reported consolidated revenue of $4.11 billion, up 3% year over year, driven by broad-based growth across banners. Retail revenue rose 3.2%, or 5.9% excluding petroleum, reflecting higher sales in automotive, apparel, and discretionary categories. Normalized income before taxes held steady at $297.7 million, while normalized diluted EPS increased 6.5% to $3.78, showing improved operating leverage despite restructuring costs.

| Metric | Q3 2025 | YoY Change | Notes |

|---|---|---|---|

| Revenue | $4.11B | +3.0% | Growth across banners |

| Normalized EPS | $3.78 | +6.5% | Higher gross margins, transformation costs excluded |

| Reported EPS | $3.13 | -11.8% | Reflects restructuring charges |

| Retail Gross Margin | $1.21B | +7.7% | Excluding Petroleum |

| ROIC | 10.6% | +130 bps | Improved operating efficiency |

| Dividend | $7.20 annualized | +1.4% | 16th consecutive increase |

| Share Buyback | $400M target by 2026 | — | Board-approved program |

Gross margin expanded 112 basis points to 34.8%, supported by improved category mix and stronger inventory management. Retail gross margin rose 7.7% to $1.21 billion, led by higher-margin categories such as workwear and athletic footwear. Financial Services income before taxes declined to $84.4 million, as expected, due to higher write-offs, while CT REIT continued to deliver stable growth, with funds from operations up 3.1%.

Balance sheet discipline remains a priority. The company declared its 16th consecutive annual dividend increase to $7.20 per share and announced its intention to repurchase up to $400 million of Class A shares by the end of 2026. Net finance costs fell 13%, and Canadian Tire ended Q3 with a retail ROIC of 10.6%, up from 9.3% a year earlier.

Look up Canadian Tire’s full financial results & estimates (It’s free) >>>

Broader Market Context

Canadian Tire’s performance comes amid a cautious but resilient consumer landscape. The company continues to benefit from diversified retail exposure across essential and discretionary categories. Notably, discretionary sales outpaced essentials for the first time since 2021, a signal of improving household sentiment despite macroeconomic headwinds.

Canada’s retail sector remains shaped by inflation moderation and a shift toward loyalty-driven ecosystems. With its growing network of brand partners and robust data capabilities through Triangle Rewards, Canadian Tire is positioning itself as one of the few retailers capable of leveraging scale and customer analytics to sustain market share growth in a competitive, high-cost environment.

1. Retail Strength and Category Momentum

Retail sales remained stable at $4.54 billion, with comparable sales up 1.8% across banners. Canadian Tire Retail led with 1.2% growth, while SportChek and Mark’s posted 4.2% and 2.5% gains, respectively. Automotive achieved its 21st consecutive quarter of growth, underscoring the strength of core categories.

Gross margin rate excluding Petroleum rose to 35.8%, supported by improved product mix, inventory restocking, and pricing efficiency. The company’s strategic reinvestment in its store base, targeting 54 modernization projects this year, continues to enhance omni-channel performance and same-day delivery coverage across all banners.

2. True North Transformation and Operational Efficiency

Canadian Tire’s “True North” transformation is now entering its execution phase. The program’s Q3 restructuring costs of $29.7 million reflect the completion of corporate reorganization and SportChek portfolio optimization. The company expects its first full quarter of cost savings in Q4 2025, with additional benefits carrying into 2026.

Beyond structural savings, the strategy emphasizes digital integration, supply chain simplification, and an agile operating model. Early results show rising normalized profitability despite lower reported EPS, indicating that transformation costs are temporary while long-term cost leverage is improving.

Value stocks like Canadian Tire in less than 60 seconds with TIKR (It’s free) >>>

3. Capital Allocation and Shareholder Value

Capital discipline remains a cornerstone of Canadian Tire’s strategy. Management reaffirmed 2025 operating capital expenditures between $525–$575 million and guided 2026 spending between $500–$550 million, maintaining flexibility for retail enhancements and digital infrastructure.

The company also continues to prioritize shareholder returns through dividends and buybacks. With $362 million in share repurchases completed year-to-date and a 1.4% dividend increase, Canadian Tire continues to balance reinvestment with capital returns. These measures signal management’s confidence in sustainable cash generation through 2026.

The TIKR Takeaway

Canadian Tire’s Q3 2025 performance highlights a company balancing near-term restructuring with steady retail execution. The normalization of earnings, margin expansion, and rising ROIC indicate underlying health in its core operations. Despite headwinds in Financial Services, the retail segment’s momentum, particularly at SportChek and Mark’s, demonstrates the benefits of product mix and depth of customer loyalty.

The forward path will hinge on the execution of the True North transformation and the successful integration of new loyalty partners in 2026. With cost savings expected in Q4 and enhanced customer engagement through partnerships with Tim Hortons, RBC, and WestJet, Canadian Tire appears well-positioned to sustain growth through a more efficient, connected retail ecosystem.

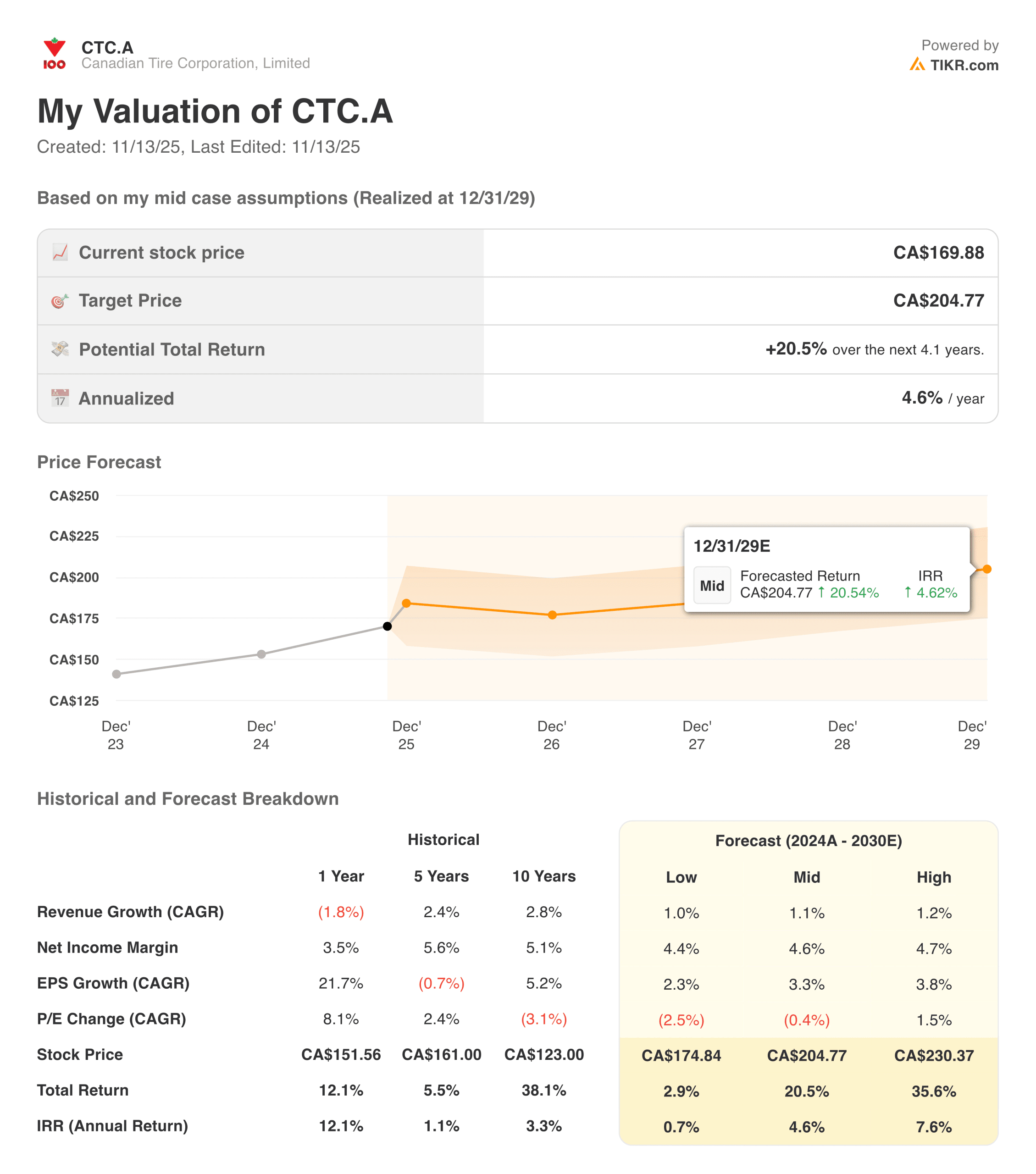

Should You Buy, Sell, or Hold Canadian Tire Stock in 2025?

Canadian Tire offers improving normalized earnings and a credible transformation plan, but short-term restructuring costs and mixed financial services results warrant caution. The long-term case remains solid, anchored by retail efficiency, strong brand equity, and consistent dividend growth, making the stock a stable hold for income-focused investors with moderate growth expectations.

How Much Upside Does Canadian Tire Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

Find out what your favorite stocks are really worth (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!