Nasdaq Inc. (NASDAQ: NDAQ) has been stable in recent years. Revenue growth has moderated, but margins remain strong and the company continues to benefit from rising demand across data, indices, and market technology. The stock trades near $87/share, moving mostly sideways as investors wait for clearer signs of acceleration in its software and analytics businesses.

Recently, Nasdaq reported continued momentum in its anti-financial-crime platform and expanded partnerships with global exchanges, reinforcing its push into higher-margin, recurring revenue businesses. The company has also seen steady market activity despite volatility across asset classes, showing the durability of its core trading and data operations. These developments suggest Nasdaq is executing well even in a more cautious environment.

This article explores where Wall Street analysts think Nasdaq could trade by 2027. We have reviewed consensus targets and valuation models to outline the stock’s potential path. These figures reflect analyst expectations and are not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Modest Upside

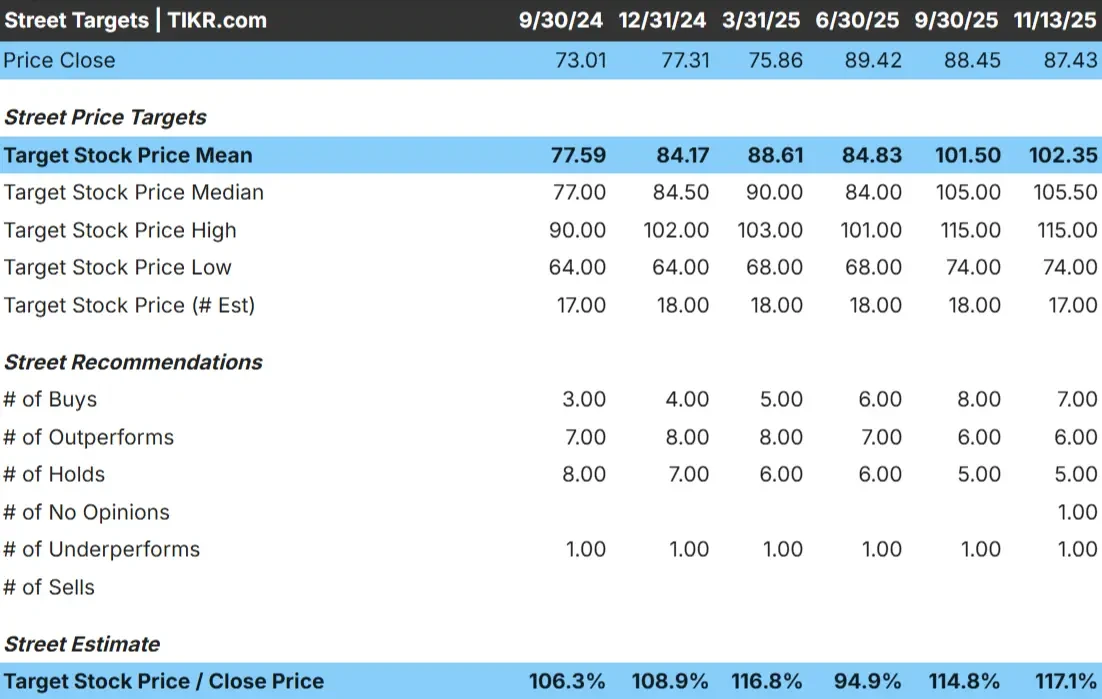

Nasdaq trades at about $87/share today. The average analyst price target is $102/share, which points to roughly 17% upside. The range is relatively tight and reflects steady sentiment:

- High estimate: ~$115/share

- Low estimate: ~$74/share

- Median target: ~$106/share

- Ratings: 7 Buys, 6 Outperforms, 5 Holds, 1 Underperform

Analysts see room for gains, but not a major re-rating. For investors, this suggests Nasdaq could outperform gradually if its data, index, and regulatory technology businesses continue expanding at a stable pace. The tight spread in targets shows analysts broadly agree on the company’s direction.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

Nasdaq: Growth Outlook and Valuation

Nasdaq’s fundamentals remain healthy and consistent, supported by strong margins and predictable recurring revenue:

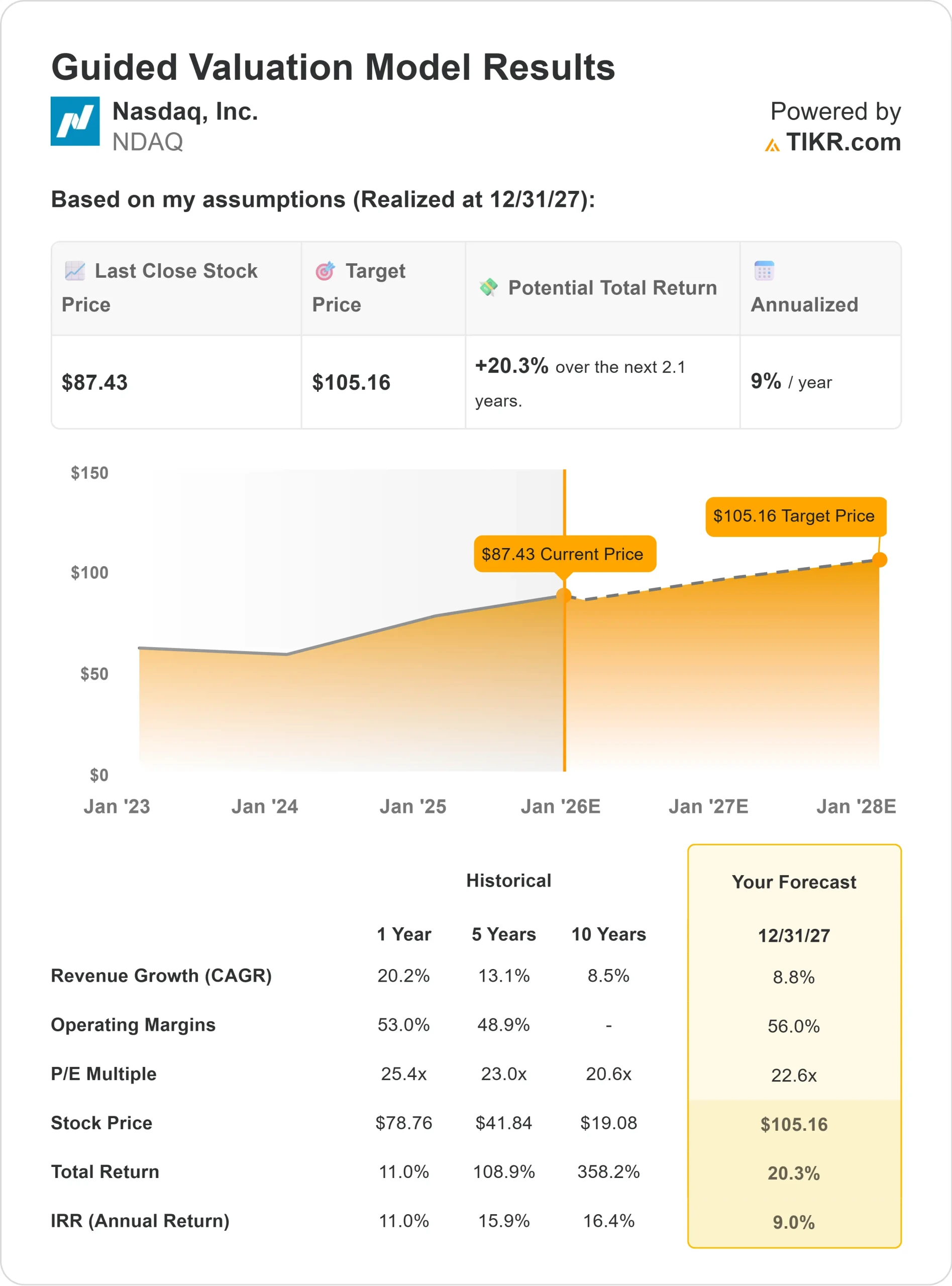

- Revenue is projected to grow about 9% annually through 2027

- Operating margins are expected to stay near 56%

- Shares trade at roughly 24x forward earnings

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 22.6x forward P/E suggests ~$105/share by 2027

- That implies roughly 20% total returns, or about 9% annualized

These figures point to a business built for steady compounding rather than rapid acceleration. The valuation looks fair for a company with strong cash flow, high retention, and a growing mix of recurring revenue.

For investors, Nasdaq offers a stable long-term setup. The upside may be modest, but the consistency of the model makes it appealing for those seeking reliable performance.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Nasdaq has steadily expanded its higher-margin segments, especially data licensing, index services, and anti-financial-crime technology. These businesses generate recurring revenue, support strong retention, and reduce dependence on trading volumes. As these segments grow, Nasdaq becomes more stable and less cyclical.

Management is also investing in cloud technology, workflow automation, and global exchange infrastructure. These efforts strengthen Nasdaq’s competitive position and support long-term growth. For investors, these strengths point to a company that can compound reliably through efficiency and rising demand for its technology platforms.

Bear Case: Slower Growth and Competitive Pressures

Despite its strengths, Nasdaq still faces challenges. Revenue growth has slowed compared to previous years, and the exchange business remains sensitive to shifts in trading volumes and overall market activity.

Competition is also rising across data, analytics, and regulatory technology. Larger competitors and new entrants continue expanding into these areas. For investors, the concern is that Nasdaq’s strong fundamentals may already be reflected in the stock price. If growth underperforms or margins tighten, upside could be limited from current levels.

Outlook for 2027: What Could Nasdaq Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model suggests Nasdaq could trade near $105/share by 2027. That represents roughly 20% upside, or about 9% annualized returns.

This outlook reflects steady progress rather than aggressive acceleration. To deliver stronger upside, Nasdaq would need faster adoption of its technology platforms, continued strength in index and data services, or a more supportive trading environment. Without that, returns are likely to remain moderate but consistent.

For investors, Nasdaq looks like a high-quality and stable compounder. The potential for higher returns depends on the company outperforming today’s expectations and unlocking more meaningful growth in its technology and analytics businesses.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>