Key Takeaways:

- The 2-Minute Valuation Model values Yum China stock at $59 per share in 2 years.

- That’s a potential 34% upside from today’s price of $44 per share.

- Despite economic headwinds, Yum China is projected to grow EPS by 41% over the next 3 years.

- YUMC stock trades near its lowest P/E multiple in years, offering a compelling valuation today.

- Get accurate financial data on over 100,000 global stocks for free on TIKR >>>

Yum China Holdings (YUMC) operates China’s largest restaurant company, with iconic brands including KFC, Pizza Hut, and Taco Bell, as well as local favorites like Little Sheep and Huang Ji Huang.

With over 14,000 stores across approximately 2,000 cities and towns in China, Yum China has built an unparalleled presence in the world’s second-largest economy.

With YUMC stock now trading at $44 per share, the company presents an intriguing value opportunity after several years of challenging operating conditions.

Despite ongoing headwinds in the Chinese consumer market, analyst projections show steady earnings recovery ahead, while the stock trades at historically attractive valuations.

Let’s see why.

Find the best stocks to buy today with TIKR. (It’s free) >>>

What is the 2-Minute Valuation Model?

Three core factors drive a stock’s long-term value:

- Revenue Growth: How big the business becomes.

- Margins: How much the business earns in profit.

- Multiple: How much investors are willing to pay for a business’s earnings.

Our 2-Minute Valuation Model uses a simple formula to value stocks:

Expected Normalized EPS * Forward P/E ratio = Expected Share Price

Revenue growth and margins drive a company’s long-term normalized earnings-per-share (EPS), and investors can use a stock’s long-term average P/E multiple to get an idea of how the market values a company.

Why YUMC Stock Looks Undervalued

Forecast

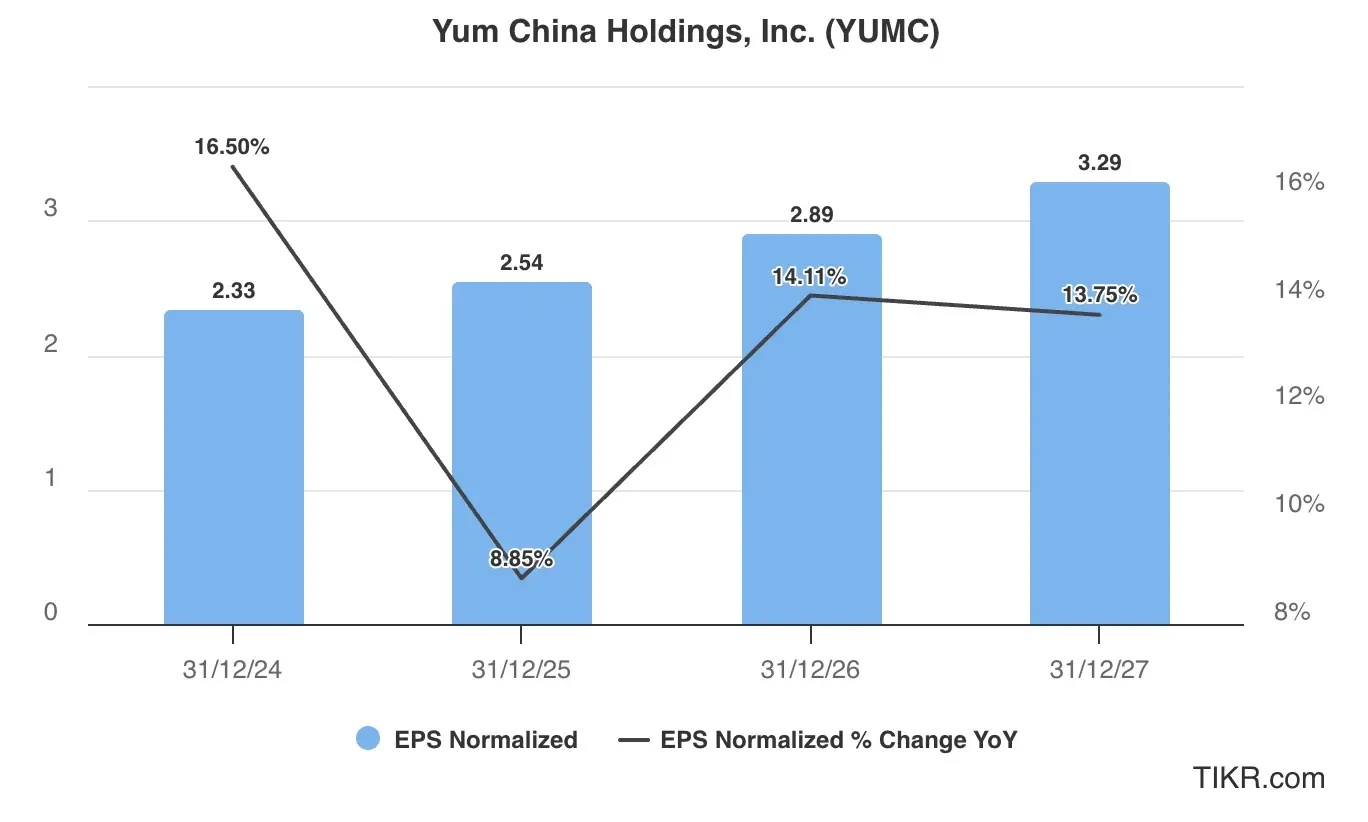

Based on analyst estimates in the EPS chart below, Yum China is expected to achieve consistent earnings-per-share growth over the next two years.

EPS is projected to grow from $2.33 in 2024 to $3.29 by 2027. This represents a 41% total increase in EPS from 2024 to 2027, reflecting Yum China’s gradual recovery from the challenges that have pressured the business in recent years.

This earnings growth for Yum China stock is likely to be driven by:

- Same-store sales recovery: As Chinese consumer confidence gradually improves, foot traffic and spending per visit are expected to normalize from recent depressed levels.

- Digital delivery growth: Yum China’s leading position in food delivery, with partnerships across all major platforms, positions it to capture the growing demand for convenience dining.

- Store expansion in lower-tier cities: The company continues opening locations in smaller cities where it faces less competition and enjoys higher profit margins.

- Operational efficiency improvements: Cost optimization initiatives and technology investments are helping to improve margins even with modest sales growth.

- Premium menu innovation: Introducing higher-priced menu items and limited-time offers helps drive average ticket size and profitability.

For our valuation, we’ll estimate that $YUMC will reach $3 in EPS in 2027.

Check out Yum China’s full analyst estimates (It’s free) >>>

Is Yum China Stock Undervalued Right Now?

Yum China stock trades at around 16x forward earnings, below its 3-year historical average P/E of 24x, as shown in the valuation chart.

This represents one of the lowest valuations in Yum China’s recent trading history, suggesting the market may be overly pessimistic about the company’s recovery prospects.

For our valuation, we’ll use a conservative forward P/E multiple of 19x. This is below the historical average, but still acknowledges the company’s improved growth profile.

Fair Value of Yum China Stock

Using our 2-Minute Valuation Model and applying a conservative approach:

- Conservative 2027 EPS estimate: $3

- Conservative forward P/E multiple: 19x

- Expected dividends over the next 2 years: $2

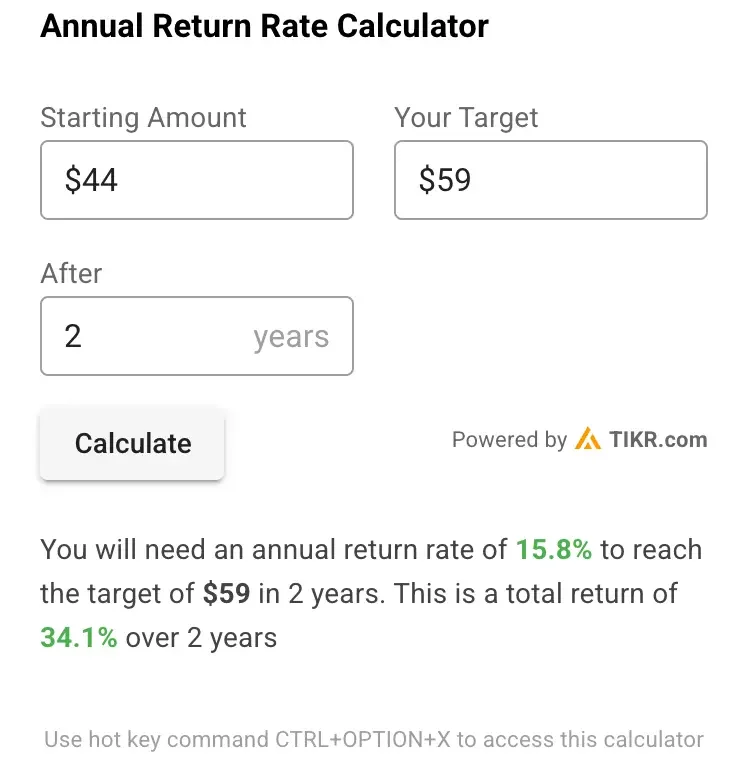

Expected Normalized EPS ($3) * Forward P/E ratio (19x) + Expected Dividends ($2) = Expected Share Price ($59)

The 2-year expected YUMC stock price we would get from this valuation is $59 per share.

With Yum China stock currently trading at around $44 per share, this implies a potential upside of 34% over the next two years or a 16% annualized return.

YUMC stock is well-positioned to deliver outsized gains to shareholders, given that average annual returns for the broader markets have been around 10%.

Remember, this is just a valuation exercise, and we don’t know for sure what the stock’s price will be in the future.

Value stocks quicker with TIKR (It’s free, no card required) >>>

What is Analysts’ Target Price for Yum China Stock?

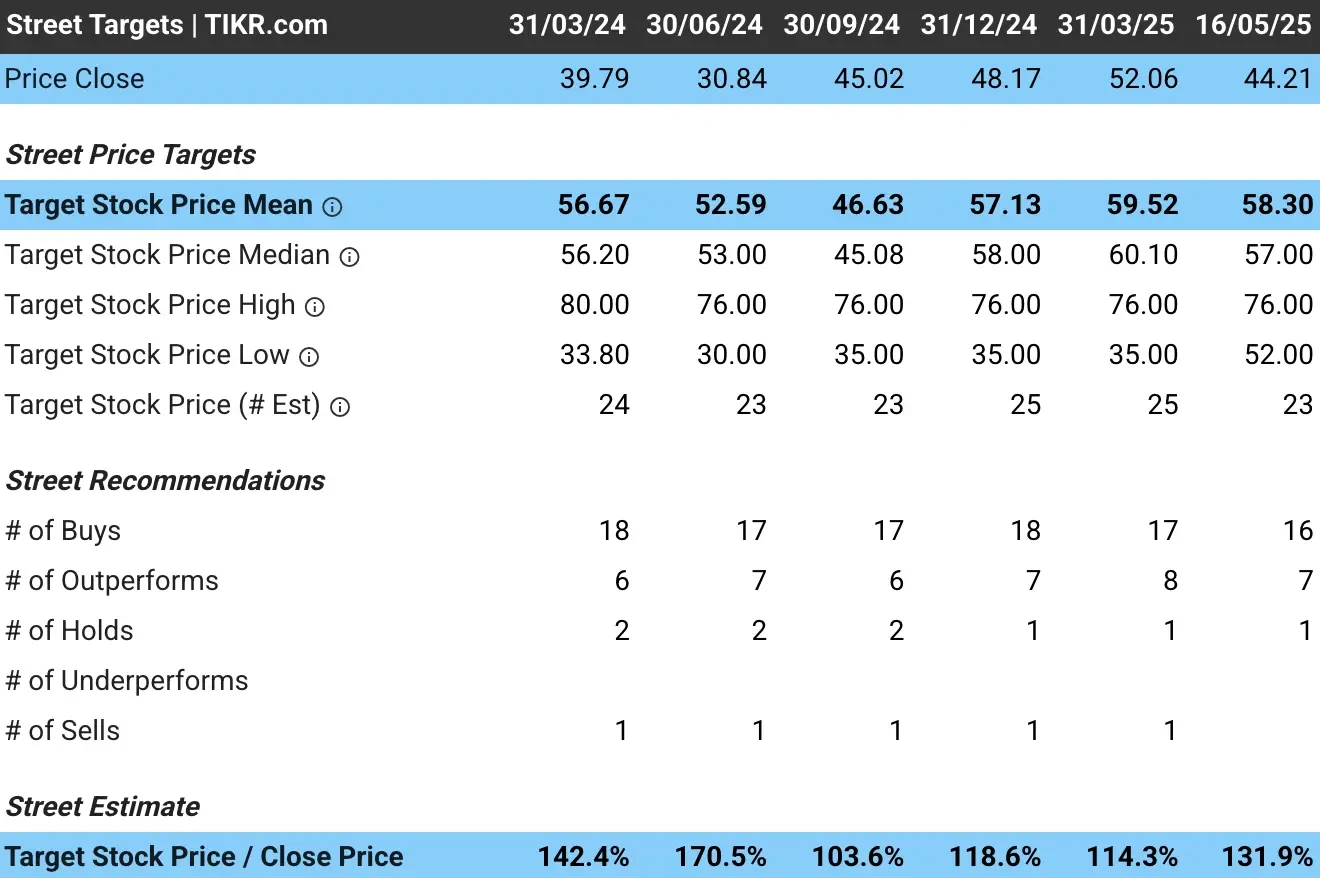

Analysts think that YUMC stock could have strong upside today.

Analysts have an average price target of around $58 per share for Yum China stock, indicating they see about 32% upside today for YUMC based on its current share price:

Risks to Consider

Despite the bullish outlook, investors should be aware of several risks that could impact Yum China’s growth trajectory:

- Chinese economic uncertainty: Slower-than-expected economic recovery in China could delay the anticipated improvement in consumer spending.

- Competitive pressure: Intense competition from local restaurants and other international chains could pressure margins and market share.

- Regulatory environment: Changes in food safety regulations, labor laws, or foreign investment policies could impact operations.

- Consumer behavior shifts: Permanent changes in dining habits or preferences could affect traditional restaurant formats.

- Currency risk: Fluctuations in the Chinese yuan could impact reported earnings for U.S. investors.

TIKR Takeaway

Yum China presents a compelling value proposition at its current depressed valuation. While it faces ongoing challenges in the Chinese market, its dominant market position, extensive store network, and strong digital capabilities position YUMC stock well for the eventual recovery.

Yum China’s strong balance sheet and cash generation provide downside protection while the company navigates current headwinds.

The projected 34% return over two years is driven by earnings recovery and potential valuation normalization as investor sentiment improves. For value-oriented investors willing to take a contrarian position on China’s consumer market, Yum China offers an attractive risk-reward opportunity.

While timing the exact bottom of the Chinese consumer cycle is difficult, the combination of low valuations, steady earnings projections, and strong analyst support suggests that patient investors could be well-rewarded.

Is YUMC stock a buy for contrarian value investors? Use TIKR to check the stock’s analyst price targets and growth forecasts to see if it is undervalued today.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!