Key Takeaways:

- The 2-Minute Valuation Model values Bank of America stock at $56 per share in 2 years.

- That’s a potential 24% upside from today’s price of $45 per share.

- BAC stock is projected to grow EPS by over 49% over the next 3 years

- Get accurate financial data on over 100,000 global stocks for free on TIKR >>>

Bank of America (BAC) delivered another solid quarter in Q1 with $7.4 billion in net income and strong fundamentals across its diversified banking platform.

Despite recent market volatility and concerns about economic uncertainty, the nation’s second-largest bank continues to demonstrate the benefits of its growth strategy and disciplined risk management.

With BAC stock now trading at around $45 per share, Bank of America presents a compelling opportunity for investors seeking exposure to a well-capitalized financial institution positioned to benefit from potential interest rate changes and economic recovery.

Let’s examine why BAC stock could be attractive today using our 2-Minute Valuation Model.

Find the best stocks to buy today with TIKR. (It’s free) >>>

What is the 2-Minute Valuation Model?

Three core factors drive a stock’s long-term value:

- Revenue Growth: How big the business becomes.

- Margins: How much the business earns in profit.

- Multiple: How much investors are willing to pay for a business’s earnings.

Our 2-Minute Valuation Model uses a simple formula to value stocks:

Expected Normalized EPS * Forward P/E ratio = Expected Share Price

Revenue growth and margins drive a company’s long-term normalized earnings-per-share (EPS), and investors can use a stock’s long-term average P/E multiple to get an idea of how the market values a company.

Why Bank of America Stock Looks Undervalued

Forecast

Based on analyst estimates, Bank of America is expected to achieve solid earnings-per-share growth over the next three years.

EPS is projected to grow from $3.21 in 2024 to $4.79 by 2027, representing a 49% increase in total.

This earnings growth for BAC stock is likely to be driven by:

- Net Interest Income Recovery: Fixed-rate asset repricing and deposit cost normalization should drive NII growth to $15.5-$15.7 billion by Q4.

- Fee Income Growth: Wealth management and investment banking fees continue expanding with organic client growth.

- Operating Leverage: Revenue growing faster than expenses, with 2025 expense growth expected at 2-3%.

- Credit Quality: Maintaining excellent asset quality with charge-offs remaining stable around current levels.

For our valuation, we estimate that BAC will reach $ 4.50 in EPS by 2027.

Check out Bank of America’s full analyst estimates (It’s free) >>>

Is BAC Stock Undervalued Right Now?

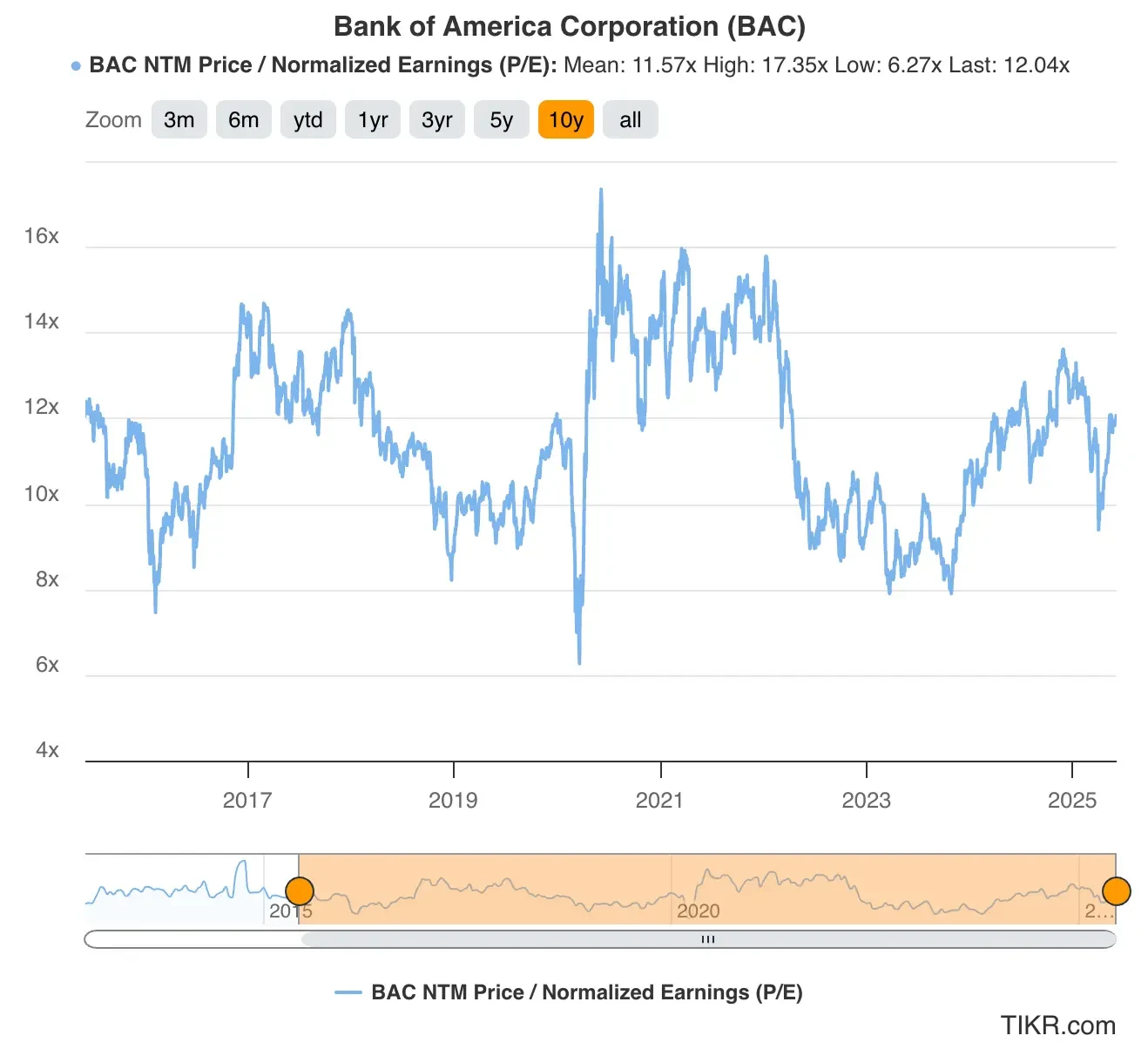

Bank of America stock trades at around 12x forward earnings, which is below its 5-year historical average P/E of 11.6x, as shown in the valuation chart.

Given the bank’s improved risk profile, diversified revenue streams, and strong capital position, a forward P/E multiple of 12x appears reasonable for our conservative valuation.

Fair Value of Bank of America Stock

Using our 2-Minute Valuation Model and applying a conservative approach:

- Conservative 2027 EPS estimate: $4.50

- Conservative forward P/E multiple: 12x

- Expected dividends over the next 2 years: $2

Expected Normalized EPS ($4.50) * Forward P/E ratio (12x) + Expected Dividends ($2) = Expected Share Price ($56)

The 2-year expected BAC stock price we would get from this valuation is $56 per share.

With Bank of America stock currently trading at around $56 per share, this implies a potential upside of 24% over the next two years or a 12% annualized return.

BAC stock is well-positioned to deliver outsized gains to shareholders, given that the broader markets’ average annual returns have been around 10%.

Remember, this is just a valuation exercise, and we don’t know for sure what the stock’s price will be in the future.

Value stocks quicker with TIKR (It’s free, no card required) >>>

What is BAC Stock’s Average Analyst Price Target?

Analysts think that Bank of America stock has a small amount of upside, with an average price target of around $49 per share for BAC stock. This indicates that they see about 10% upside today for the bank stock based on its current share price:

Risks to Consider

Despite the bullish outlook, investors should be aware of several risks that could impact Bank of America’s growth trajectory:

- Interest Rate Sensitivity: The bank remains sensitive to interest rate changes, with NII potentially declining if rates fall faster than expected.

- Credit Cycle: While credit quality is currently excellent, economic uncertainty could lead to higher charge-offs.

- Regulatory Changes: New banking regulations or capital requirements could impact profitability.

- Economic Slowdown: A recession could pressure loan growth and increase credit losses across the portfolio.

TIKR Takeaway

Bank of America presents a compelling value proposition at current levels. The stock’s potential upside is driven by strong projected earnings growth, improving operating leverage, and a reasonable valuation multiple relative to its improved risk profile.

While macroeconomic uncertainty persists, Bank of America’s diversified business model, strong capital position, and disciplined risk management provide a solid foundation for long-term growth.

The bank’s demonstrated ability to grow organically while maintaining excellent credit quality makes it an attractive option for investors seeking exposure to the financial sector.

Investors should be prepared for some volatility, but BAC’s consistent execution and strategic positioning make it a compelling choice for those seeking both income and capital appreciation.

Is BAC stock a buy over the next 24 months? Use TIKR to check the stock’s analyst price targets and growth forecasts to see if it is undervalued today.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!