Key Takeaways:

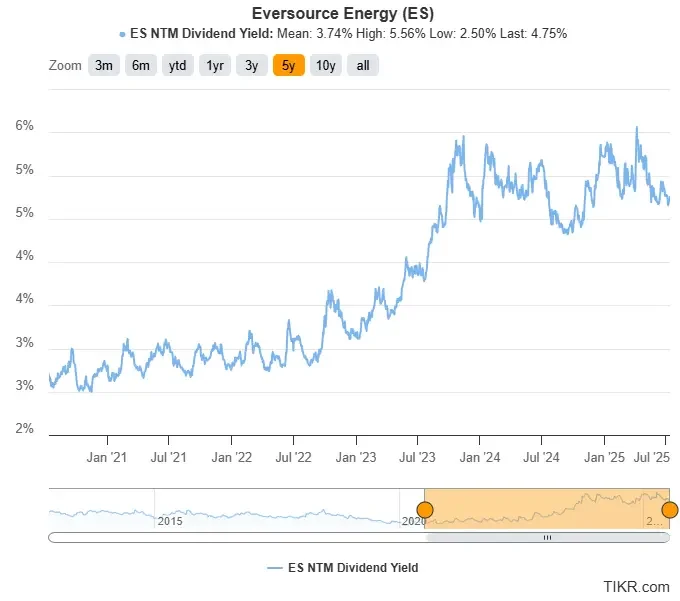

- Eversource Energy (ES) pays a 4.75% dividend yield, well above its 5-year average of 3.74%.

- The stock trades around $65/share, and based on analyst estimates, it could be worth $79/share by the end of 2027, implying 8.4% annual returns.

- With 25 years of dividend growth and a stable utility model, ES offers dependable income with modest upside potential.

Eversource Energy (ES) is a regulated utility serving millions of customers across New England. At first glance, it might seem like just another slow-moving utility stock. But with shares still down over 30% from their 2022 highs and the dividend yield approaching 5%, there’s more to the story.

The company has begun pivoting back to its core utility operations, planning to sell off non-core renewable assets to strengthen its balance sheet and focus on regulated earnings. Analysts expect this shift to gradually improve profitability and restore earnings growth over the next few years.

For income-focused investors, that sets up an interesting opportunity: a steady, investment-grade utility offering a near-5% yield with potential for modest upside as fundamentals recover. If the turnaround plays out, ES could offer a rare mix of stability, yield, and long-term value.

Analysts Think the Stock is Undervalued Today

Eversource shares currently trade around $65/share, and based on analysts’ consensus estimates, the stock could be worth $79/share by the end of 2027.

That implies a 22% total return over the next 2.5 years, or about 8.4% annually with dividends included.

The recent drop in stock price has mostly come from one-time challenges like offshore wind project write-offs and elevated interest expenses. But as the company completes its restructuring and refocuses on regulated utility growth, analysts expect earnings and dividends to grow consistently.

Value any stock in less than 60 seconds with TIKR (It’s free) >>>

A 4.75% Dividend Yield That Stands Out

Eversource’s dividend yield is now 4.75%, which is well above its 5-year average of 3.74%.

The elevated yield is the result of a sharp drop in the company’s stock price, which is now down more than 25% from its 2022 peak.

Eversource’s regulated operations across New England continue to generate consistent cash flows, and the company plans to refocus on its core utility business by selling off non-core renewable assets.

Given the company’s investment-grade balance sheet, consistent cash flows, and long history of dividend increases, the 4.75% yield looks well-supported. While a sharp rebound in the stock may take time, investors today are being paid generously to wait.

For long-term income investors, this could be an opportunity to lock in an above-average yield from a utility that’s streamlining its strategy and maintaining dividend growth through the transition.

Find high-quality dividend stocks that look even better than Eversource today. (It’s free) >>>

Dividend Looks Safe With Room for Consistent Growth

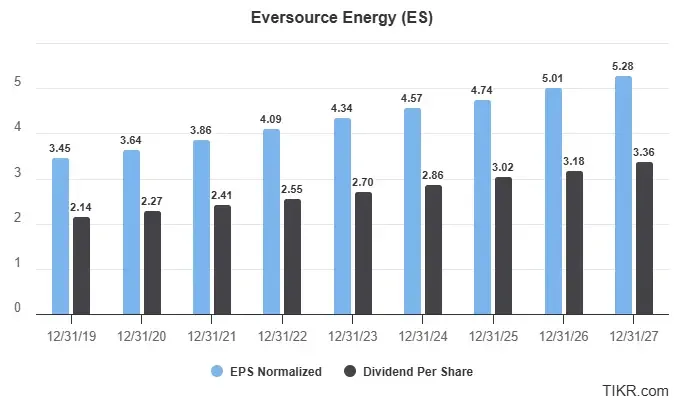

Eversource is expected to pay about $3.02 per share in dividends this year, while analysts project $4.74 in EPS for 2025, putting the forward payout ratio near 64%.

In January 2025, Eversource announced the $2.4 billion sale of its Aquarion Water business. This move was designed to reduce debt and sharpen the company’s focus on its core regulated electric and gas operations across New England.

Analysts expect normalized EPS to grow at a steady 5% to 6% annually over the next few years, with dividend growth projected to track slightly behind, at around 5% per year.

EPS growth is expected to be driven by regulated rate base expansion, ongoing infrastructure investments in electric and gas systems, and lower interest expense following the Aquarion sale.

See Eversource’s full growth forecast and analyst estimates. (It’s free) >>>

Wall Street Analysts Are Bullish on These 5 Undervalued Compounders With Market-Beating Potential

TIKR just released a new free report on 5 compounders that appear undervalued, have beaten the market in the past, and could continue to outperform on a 1-5 year timeline based on analysts’ estimates.

Inside, you’ll get a breakdown of 5 high-quality businesses with:

- Strong revenue growth and durable competitive advantages

- Attractive valuations based on forward earnings and expected earnings growth

- Long-term upside potential backed by analyst forecasts and TIKR’s valuation models

These are the kinds of stocks that can deliver massive long-term returns, especially if you catch them while they’re still trading at a discount.

Whether you’re a long-term investor or just looking for great businesses trading below fair value, this report will help you zero in on high-upside opportunities.

Click here to sign up for TIKR and get our full report on 5 undervalued compounders completely free.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!