Rivian Automotive (NASDAQ: RIVN) has emerged as one of the most talked-about electric vehicle stocks in recent years. While shares have experienced sharp swings, including a significant drawdown from their 2021 post-IPO highs, investor interest remains strong as excitement builds around the company’s production ramp-up, delivery milestones, and long-term potential in the EV market.

In this article, we explore Wall Street analysts’ forecasts for Rivian through 2027, pulling from consensus estimates and company guidance to understand where the stock might be headed. These projections are based on third-party analyst data and do not represent TIKR’s own forecast.

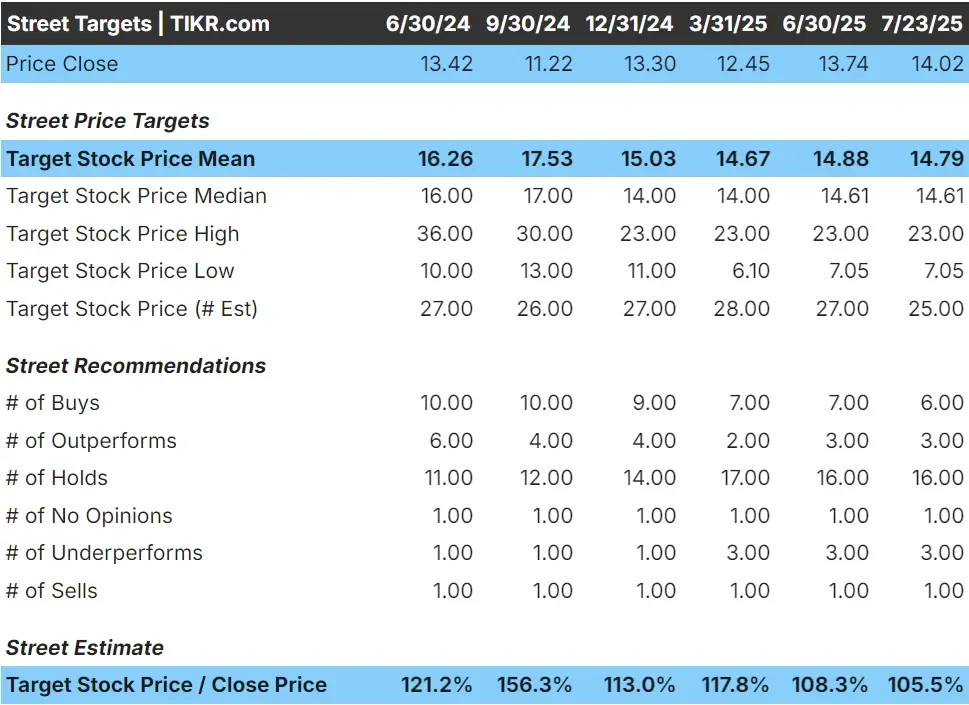

Analyst Price Targets: Optimism Has Cooled, but Long-Term Upside Remains

Wall Street analysts remain cautiously optimistic about Rivian’s future, but the range of price targets has narrowed over the last year. As of late July 2025, Rivian trades around $14, and the average analyst target sits at $14.79, suggesting a modest 6% upside over the next 18 months for the stock. That’s a far cry from late 2024, when the average price target implied more than 50% upside while the stock traded near its lows of around $11/share.

The high end of the forecast remains anchored at $23/share, while the lowest target is around $7/share. In short, analysts are still supportive of Rivian’s long-term potential, but recent price gains and execution risk appear to have tempered short-term enthusiasm.

Revenue and Growth Outlook

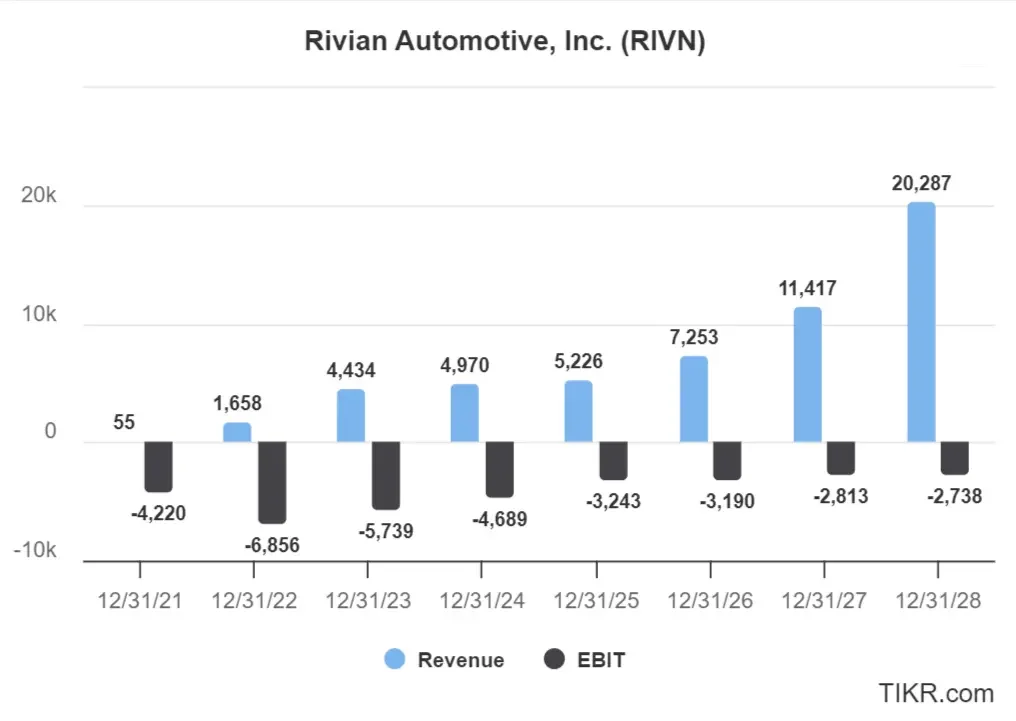

Rivian’s revenue is expected to scale meaningfully as the company ramps production and delivers more vehicles. After generating nearly $5 billion in revenue in 2024, analysts project steady gains in the coming years, with revenue climbing to $5.2 billion in 2025 and $7.3 billion in 2026. By 2027, Wall Street expects Rivian to generate over $11.4 billion in sales, more than doubling what the business is expected to see in 2025.

This growth implies revenue will grow at a compound annual growth rate (CAGR) of over 30% between 2024 and 2027. While impressive, the company is still projected to operate at a loss over this period, with EBIT expected to remain negative through at least 2028.

The ramp-up in revenue suggests confidence in Rivian’s ability to scale manufacturing and secure demand, but profitability remains a key hurdle to watch.

Valuation Multiples Still Stretched

While Rivian’s projected revenue growth is impressive, the company remains far from profitability. Analysts don’t expect Rivian to post positive EBIT through at least 2028, with projected operating losses of $3.2 billion in 2025 and $2.8 billion in 2027, even as revenue crosses $11 billion.

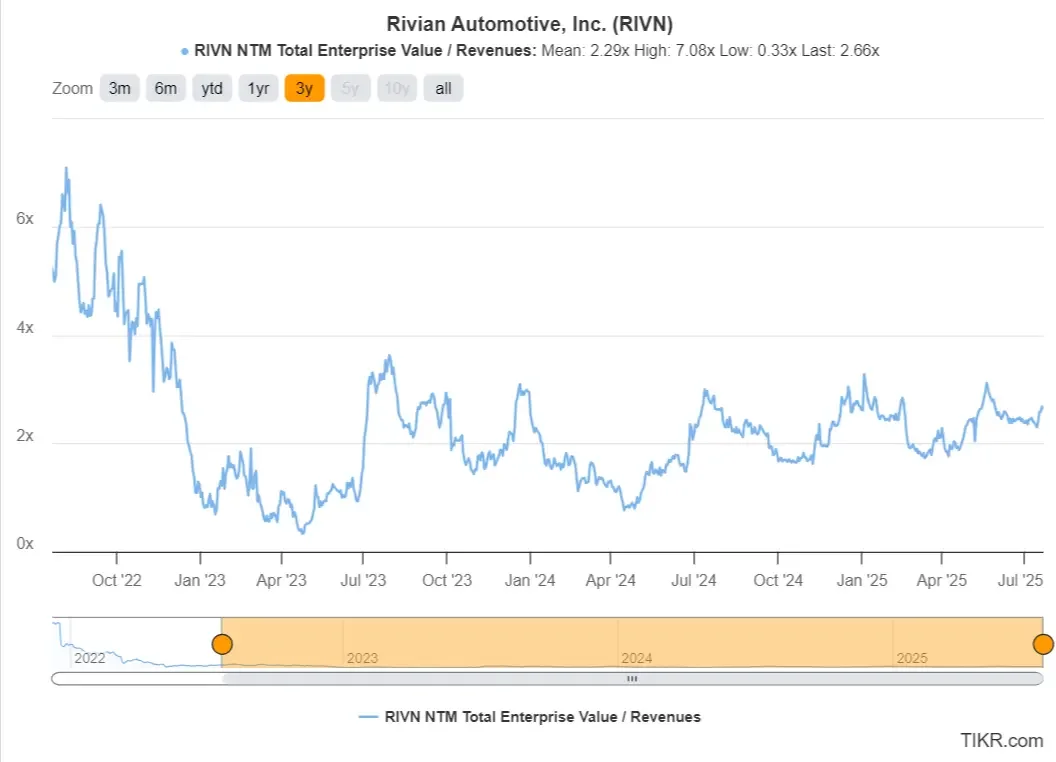

From a valuation standpoint, the stock still looks expensive relative to fundamentals. As of July 2025, Rivian trades at 2.66x forward revenue, slightly above its 3-year average of 2.29x despite the company continuing to burn cash and reporting multi-billion-dollar annual losses.

With no positive EBITDA on the near-term horizon, traditional valuation metrics like EV/EBITDA or Price/Normalized Earnings remain unhelpful. Investors are effectively pricing Rivian on future revenue potential, which leaves little margin for error if growth slows or margins fail to improve.

What’s Driving the Optimism?

The bull case for Rivian is built on its strong revenue growth, expanding vehicle lineup, and deep-pocketed partners. Deliveries are rising, the R1S is gaining traction in the SUV market, and Rivian continues to fulfill its delivery van contract with Amazon.

The upcoming R2 launch in 2026 has also fueled optimism. With a lower price point, it could help Rivian reach a broader market and drive volume growth.

Despite ongoing losses, the company ended Q1 2025 with over $7 billion in cash, giving it flexibility to keep investing in production and product development. Management remains focused on vertical integration and building a premium EV brand, which investors hope will lead to durable competitive advantages over time.

Bear Case: Losses, Competition, and Execution Risk

While Rivian’s growth story is compelling, the company is still losing billions of dollars each year. Analysts don’t expect it to generate positive operating income until after 2028, which means profitability isn’t coming anytime soon.

Also, the EV space is fiercely competitive. Tesla dominates the market, while legacy automakers like Ford, GM, and Hyundai are scaling their own EV offerings. Unlike legacy auto rivals, Rivian doesn’t have a profitable gas-powered business to fall back on if EV demand softens.

Execution risk is another concern. Delays, cost overruns, or supply chain hiccups could hurt margins or derail production targets. Rivian’s current valuation still assumes strong revenue growth and operational improvement, so any slip-ups could lead to a sharp market reaction.

Outlook for 2027: What Could Rivian Be Worth?

Rivian’s valuation in 2027 depends on two key factors: how much revenue it generates and whether it can get closer to profitability.

In a very bullish scenario, Rivian reaches analyst estimates of $11.4 billion in revenue and trades at a 2.5x EV/Revenue multiple. That would imply a market cap of roughly $28.5 billion. With 1.2 billion shares outstanding, the stock would trade around $24 per share.

In a more conservative (and likely) case, Rivian still hits $11.4 billion in revenue, but trades at a 1.5x multiple due to ongoing losses or industry headwinds. That would imply a market cap closer to $17 billion, or about $14 per share.

Keep in mind, Rivian is likely to still be unprofitable years from now and relies on debt and equity financing, which adds some risk to the business.

Bottom line: Even if Rivian grows rapidly, its long-term stock performance will depend on margin improvement, production execution, and sustained investor confidence.

Wall Street Analysts Are Bullish on These 5 Undervalued Compounders With Market-Beating Potential

TIKR just released a new free report on 5 compounders that appear undervalued, have beaten the market in the past, and could continue to outperform on a 1-5 year timeline based on analysts’ estimates.

Inside, you’ll get a breakdown of 5 high-quality businesses with:

- Strong revenue growth and durable competitive advantages

- Attractive valuations based on forward earnings and expected earnings growth

- Long-term upside potential backed by analyst forecasts and TIKR’s valuation models

These are the kinds of stocks that can deliver massive long-term returns, especially if you catch them while they’re still trading at a discount.

Whether you’re a long-term investor or just looking for great businesses trading below fair value, this report will help you zero in on high-upside opportunities.

Click here to sign up for TIKR and get our full report on 5 undervalued compounders completely free.