Key Takeaways:

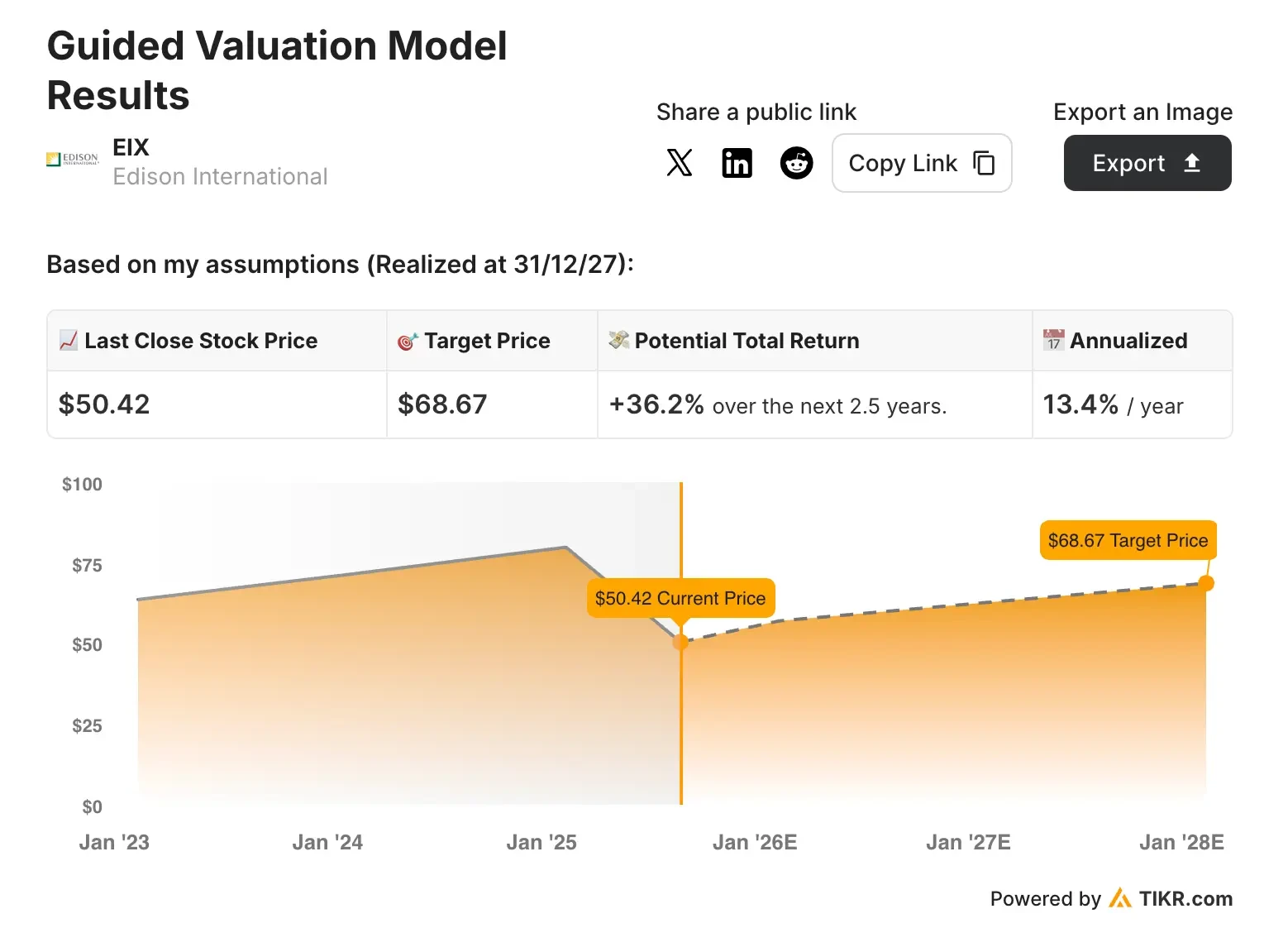

- Edison International stock could reasonably reach $69/share by the end of 2027, based on our valuation assumptions.

- That implies a 36% total return from today’s price of $51/share, with an annualized return of 13% over the next 2.5 years.

- Edison operates as a leading electric utility company serving Southern California through its subsidiary, Southern California Edison.

Edison International (EIX) is a public utility holding company that operates primarily through Southern California Edison, one of the largest electric utilities in the United States.

Edison serves approximately 15 million people across a 50,000-square-mile service territory in Southern California.

The utility giant benefits from a robust capital investment program focused on grid modernization, wildfire mitigation, and infrastructure resilience.

With ongoing regulatory proceedings supporting rate base growth and a constructive regulatory environment in California, Edison remains positioned as a steady utility growth story despite recent wildfire-related challenges.

With approximately $15 billion in annual revenue, record infrastructure investments, and multiple growth drivers advancing through regulatory approval, Edison maintains its position as a premier regulated utility investment opportunity.

Here’s why EIX stock could return 13% annually through 2027 and continue delivering steady performance through 2030.

Try TIKR’s Valuation Model today for FREE (It’s the easiest way to find undervalued stocks) >>>

What the Model Says for EIX Stock

We analyzed Edison’s upside using valuation assumptions based on the company’s regulated utility operations and expanding rate base investments.

Based on estimates of 4% annual revenue growth, 25% operating margins, and stable valuation multiples, the model projects EIX stock could rise from $50/share to $69/share.

That represents a total return of 36% and an annualized return of 13% over the next 2.5 years. This return forecast includes expected dividend payments:

Value Edison International for yourself in less than 60 seconds (It’s free!) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for EIX stock:

1. Revenue Growth: 4%

Edison delivered solid Q1 results with core earnings per share of $1.37 compared to $1.13 a year ago.

It reaffirmed confidence in meeting its 2025 EPS guidance and delivering core EPS growth of 5% to 7% through 2028.

We used a 4% forecast reflecting steady regulated utility growth driven by rate base expansion from infrastructure investments and wildfire mitigation programs.

2. Operating Margins: 25%

Edison demonstrates consistent profitability typical of regulated utilities with predictable cost recovery mechanisms.

Analysts’ consensus estimates project stable margins as Edison International executes its capital investment program with appropriate regulatory cost recovery.

3. Exit P/E Multiple: 9x

EIX stock trades at reasonable multiples for a regulated utility with steady growth prospects. We maintain current valuation levels given a regulated business model and constructive regulatory environment in California.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

TIKR’s valuation tool allows investors to test a wide range of outcomes based on how EIX stock performs through 2030 under different scenarios (these are estimates, not guaranteed returns). These valuations include expected dividend payments:

- Low Case: Regulatory challenges and wildfire liability concerns → 8% annual returns

- Mid Case: Steady execution of capital programs and rate recovery → 12% annual returns

- High Case: Accelerated infrastructure investments and favorable regulatory outcomes → 14% annual returns

Even in the conservative case, Edison stock offers attractive single-digit returns typical of utility investments, while the upside scenario could deliver solid performance if regulatory and operational catalysts materialize.

See analysts’ growth forecasts and price targets for any stock (It’s free!) >>>

TIKR Takeaway

Edison represents a compelling combination of regulated utility stability and growth opportunities through infrastructure modernization in one of the nation’s largest service territories.

With an estimated 36% upside by the end of 2027 and potential annual returns of 13%, Edison stands out as a steady utility play benefiting from ongoing rate base growth, essential infrastructure investments, and California’s supportive regulatory framework for grid hardening and wildfire mitigation.

EIX stock is best suited for investors seeking exposure to regulated utilities, companies with predictable cash flows and dividend potential, as well as infrastructure investment themes in growing markets like Southern California.

The combination of regulatory visibility, essential service provision, and substantial capital investment opportunities makes Edison an attractive consideration for income-oriented utility portfolios, positioning the stock for steady long-term performance.

Is EIX stock worth buying today? Use TIKR’s Valuation Model and analyst forecasts to see if it looks undervalued.

Value any stock with TIKR’s Valuation Model (It’s free!) >>>

Wall Street Analysts Are Bullish on These 5 Undervalued Compounders With Market-Beating Potential

TIKR just released a new free report on 5 compounders that appear undervalued, have beaten the market in the past, and could continue to outperform on a 1-5 year timeline based on analysts’ estimates.

Inside, you’ll get a breakdown of 5 high-quality businesses with:

- Strong revenue growth and durable competitive advantages

- Attractive valuations based on forward earnings and expected earnings growth

- Long-term upside potential backed by analyst forecasts and TIKR’s valuation models

These are the kinds of stocks that can deliver massive long-term returns, especially if you catch them while they’re still trading at a discount.

Whether you’re a long-term investor or just looking for great businesses trading below fair value, this report will help you zero in on high-upside opportunities.

Click here to sign up for TIKR and get our full report on 5 undervalued compounders completely free.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!